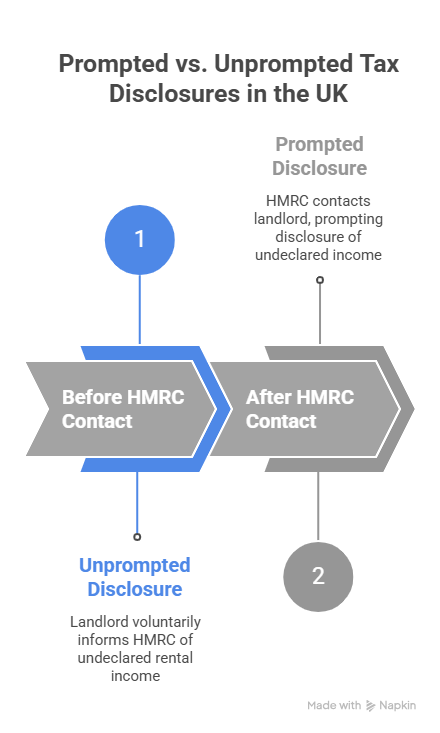

If you are a landlord with undeclared rental income, you are likely standing at a digital crossroads. On one path, you come forward voluntarily to settle your debts. On the other, you wait until a brown envelope from HMRC arrives on your doorstep. In the world of UK tax compliance, these two paths are known as Prompted vs Unprompted disclosures.

Understanding the difference between these two categories isn’t just academic—it is a financial imperative. The “Let Property Campaign” (LPC) is designed to be a bridge back to compliance, but the toll you pay to cross that bridge depends entirely on who starts the conversation.

In this deep-dive guide, we will break down the mechanics of the Let Property Campaign, compare the penalty structures of prompted vs. unprompted disclosures, and explain why the timing of your disclosure is the single most significant factor in protecting your assets.

Featured Snippet: What is the difference between Prompted vs Unprompted disclosures?

The primary difference lies in timing and cost. An unprompted disclosure occurs when a landlord voluntarily notifies HMRC of unpaid tax before any inquiry is opened. A prompted disclosure happens after HMRC contacts the landlord (often via a “nudge letter”). Unprompted disclosures carry significantly lower penalties, often starting at 0% for “reasonable care” errors.

The Anatomy of the Let Property Campaign

The Let Property Campaign is a specific disclosure opportunity for individual landlords letting out residential property. It is not available to limited companies or those letting out commercial premises.

HMRC’s goal with this campaign is efficiency. It is cheaper for the government if you do the math and hand over the tax than it is for them to assign an inspector to hunt you down. To incentivize this, they created a sliding scale of leniency.

Why Does HMRC Distinguish Between the Two?

HMRC rewards “honesty before discovery.” If you realize you’ve made a mistake and move to fix it, you are seen as a low-risk taxpayer who made an error. If you only move to fix it because you were caught, you are viewed as a high-risk taxpayer who was potentially trying to evade their obligations.

Defining the Unprompted Disclosure

An unprompted disclosure is a proactive strike. It means you have contacted HMRC to tell them you have unpaid tax before they have sent you a letter, opened an inquiry, or even hinted that they are looking at your affairs.

The Financial Benefits of Being Proactive

The most compelling reason to stay in the “unprompted” category is the penalty floor. For errors made despite taking “reasonable care,” the penalty can be as low as 0%. Even for “careless” behavior, the unprompted penalty can remain at 0% if you provide full assistance to HMRC.

The Psychological Peace of Mind

When you lead the disclosure, you control the narrative. You aren’t responding to accusations; you are presenting a professional, calculated summary of your affairs. This often leads to a much smoother settlement process and a faster conclusion.

Defining the Prompted Disclosure

A prompted disclosure is a reactive move. This usually begins when you receive a “nudge letter” or a formal notice of inquiry.

The “Nudge Letter” Trap

HMRC sends out thousands of these letters to landlords in London, Windsor, Oxford, and Reading. The letter essentially says, “We have information that you have rental income; check your records and let us know.” The moment that letter is generated and sent, your window for an unprompted disclosure has effectively slammed shut.

The Cost of Hesitation

In a prompted scenario, the “penalty floor” rises. HMRC assumes that you wouldn’t have come forward if they hadn’t nudged you. Therefore, the minimum fine for “careless” behavior jumps from 0% to 15%. If the behavior is deemed “deliberate,” the prompted penalties can be eye-watering, often reaching 35% to 70% of the tax due.

Detailed Comparison: Prompted vs. Unprompted

To help you visualize the stakes, consider this comparison of the two disclosure types across different behavioral categories.

Behavioral Categorization: The Secret Ingredient

HMRC doesn’t just look at when you disclosed; they look at why you didn’t pay in the first place. This behavior dictates which row of the penalty table you fall into.

- Reasonable Care: You kept records and tried to follow the rules, but perhaps you misunderstood a complex deduction or a change in law.

- Careless: You didn’t keep good records, or you “forgot” about the income for several years without checking your obligations.

- Deliberate: You knew you owed tax, but you decided not to pay it.

- Deliberate & Concealed: You knew you owed tax and took active steps to hide it (e.g., using offshore accounts or false names).

The Multiplier Effect: If you are “Deliberate” and “Prompted,” you are looking at the highest possible financial punishment available under the Let Property Campaign.

The Disclosure Timeline: From Start to Finish

Regardless of whether your disclosure is prompted or unprompted, the technical process follows a similar 4-step framework.

1. Notification

You notify HMRC that you intend to make a disclosure under the campaign. For unprompted cases, this is done via the Digital Disclosure Service (DDS). For prompted cases, you usually reply to the specific officer or department that contacted you.

2. Calculation (The 90-Day Clock)

Once notified, you have 90 days to prepare your figures. This includes:

- Total rental income for all relevant years.

- Deductible expenses (maintenance, agent fees, insurance).

- Mortgage interest relief (restricted to basic rate tax credit).

- Calculation of tax, interest, and your proposed penalty percentage.

3. Submission

You submit your final disclosure. At this stage, you must pay the amount in full or have a payment plan ready to propose.

4. Acceptance

HMRC reviews your submission. If they agree with your behavior categorization and your figures, they will issue an acceptance letter. The case is then closed.

Strategy: How to Move from “Prompted” back to “Leniency”

If you have already received a nudge letter, you might feel like you’ve already lost. While you can’t technically revert to “unprompted” status, you can still significantly reduce your penalties within the “prompted” range through Quality of Disclosure.

HMRC reduces fines based on:

- Telling: Being 100% transparent about the errors.

- Helping: Responding to their queries within days, not weeks.

- Giving Access: Providing all bank statements and records without being forced to via a formal notice.

By maximizing these three factors, a landlord in Slough or Reading who has been prompted can often pull their penalty down toward the minimum floor of that category.

Case Study: The Proactive vs. The Reactive Landlord

Landlord X (Windsor): Owns a flat and hasn’t declared income for 6 years. They read about the Let Property Campaign and hire an expert to file an unprompted disclosure.

- Outcome: Behavior is judged “Careless.” Penalty is negotiated to 0% because they provided full assistance and came forward voluntarily.

Landlord Y (Oxford): Owns an identical flat with the same 6-year history. They wait. HMRC sends a nudge letter. Landlord Y eventually discloses.

- Outcome: Behavior is also “Careless.” Because it was prompted, the minimum penalty is 15%.

On a tax bill of £20,000, Landlord Y pays £3,000 more than Landlord X for the exact same mistake—simply because of the timing.

Serving Landlords in the South East and Beyond

Tax compliance isn’t just about numbers; it’s about local context. We provide specialized Let Property Campaign support across key regions:

- London: Dealing with high-volume rental income and the complexities of the Non-Resident Landlord Scheme (NRLS).

- Windsor & Reading: Supporting landlords with high-value portfolios where “deliberate” accusations from HMRC can lead to massive financial losses.

- Oxford & Slough: Helping academic and professional landlords fix historical errors before they trigger a full HMRC investigation.

Prompted vs Unprompted

Overview: Quick Differences

- Unprompted: Voluntary, happens before HMRC contact. Lowest penalties (0% minimum).

- Prompted: Happens after HMRC contact (Nudge letters). Higher penalty floors (15% minimum for careless).

- Common Goal: Both use the Let Property Campaign to settle back tax and interest.

- Actionable Advice: If you haven’t been contacted yet, disclose immediately to lock in “Unprompted” status.

FAQ: People Also Ask

1. What exactly triggers a “prompted” status?

HMRC considers a disclosure prompted if it is made at a time when they have reason to believe that tax has been underpaid. This is almost always triggered by the issuance of a “nudge letter” or a notice of an intended tax return inquiry.

2. Can I still use the Let Property Campaign if I got a letter?

Yes. Even if you are prompted, the Let Property Campaign is usually the most efficient way to settle. It is still better than a full, intrusive tax investigation which could look into your lifestyle, business, and other income sources.

3. Does a phone call from HMRC count as a “prompt”?

Generally, yes. If HMRC contacts you specifically about your property income, any disclosure made after that point is likely to be treated as prompted.

4. How far back does an unprompted disclosure go?

The “look-back” period depends on behavior, not the prompt status. If you were careless, it’s 6 years. If it was a reasonable excuse, it’s 4. If it was deliberate, it can be up to 20 years.

5. What if I genuinely didn’t know I had to declare it?

This is often categorized as “Careless.” While “Ignorance of the law is no excuse” is a legal maxim, an unprompted disclosure for a careless mistake often results in a 0% penalty if you help HMRC resolve the matter quickly.

6. Is the interest higher for prompted disclosures?

No, the statutory interest rate is the same. However, because prompted disclosures often take longer to resolve (due to HMRC’s involvement), more interest may accrue over time.

Why Timing is Everything

The difference between a Prompted vs Unprompted Let Property Campaign disclosure is the difference between being a “partner” in the process and being a “target.”

HMRC’s “Connect” system is running 24/7, matching Land Registry data with your tax returns. If there is a gap, a nudge letter is inevitable. By moving now—on your own terms—you drastically reduce your penalties, limit the number of years HMRC investigates, and save yourself the immense stress of a forced inquiry.

Are you ready to clear your record and protect your property investment? Learn More