LPC disclosure provides residential landlords a clear path to bring their tax affairs up to date. HMRC introduced the Let Property Campaign in 2013. It gives property owners an opportunity to report previously undeclared rental income.

You can use this facility if you received an official nudge letter. You can also use it if you choose to come forward voluntarily. Declaring your income before HMRC finds the error keeps interest charges lower and limits financial penalties.

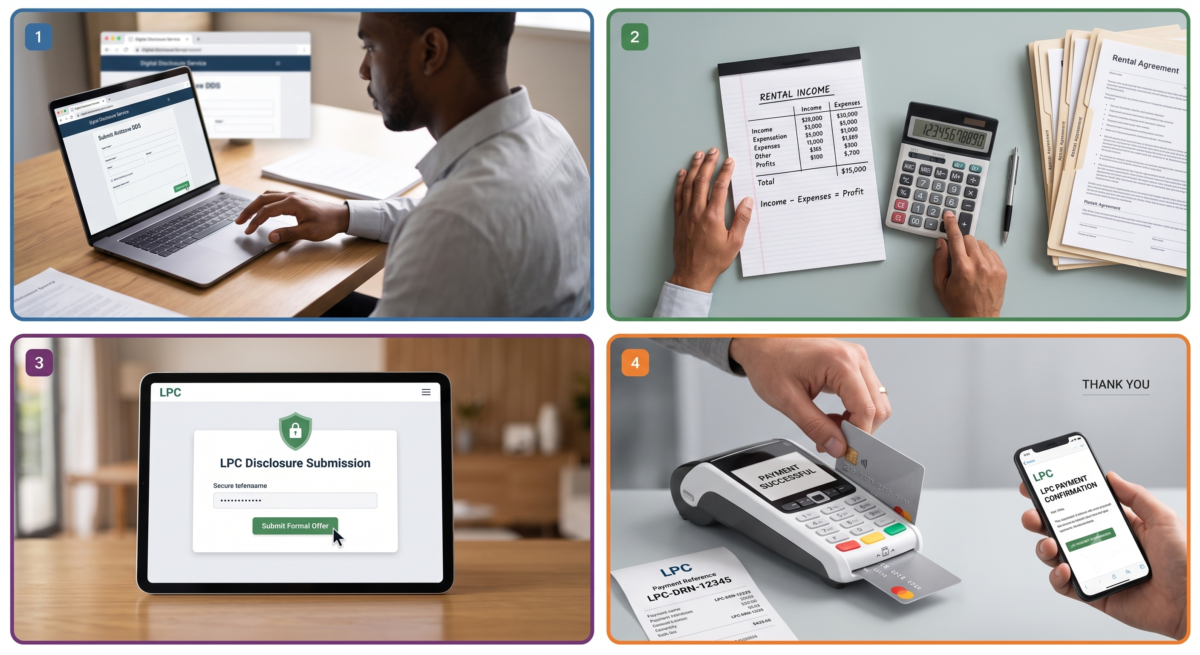

| Step | Action | Key Tasks | Outputs & Deadlines |

| 1 | Notify HMRC | Submit the Digital Disclosure Service (DDS) form | Receive Disclosure Reference Number (DRN) & PRN |

| 2 | Calculate Tax & Penalties | Determine net rental profit (income minus expenses); calculate tax, interest, and applicable penalties | Complete within the 90-day window |

| 3 | Submit Formal Disclosure | Submit formal offer to HMRC using your Payment Reference Number (PRN) | Binding disclosure agreement |

| 4 | Settle Liability | Pay the total balance in full or negotiate a Time-to-Pay arrangement | Settle before the 90-day deadline |

Eligibility for LPC Disclosure

The Let Property Campaign covers a broad range of residential landlords. Anyone with undeclared rental income from residential property can apply.

- Renting out a room in your main home for more than the £7,500 Rent a Room scheme threshold.

- Renting out single or multiple residential properties.

- Living abroad while renting out UK property.

- Living in the UK while renting out property abroad.

- Renting out holiday home rentals, even when you use the property personally.

Exceptions

The scheme does not apply to every landlord. You cannot use the LPC disclosure process for:

- Commercial properties like shops, garages, or lockup storage units.

- Properties owned by corporate entities, companies, or trusts.

HMRC Nudge Letters

HMRC cross-checks tax returns with external data sources like the Land Registry, local council records, and letting agent reports. If their records show property activity without matching tax entries, they issue a formal warning letter.

If you receive a nudge letter, act promptly. Ignoring this letter can lead to formal tax audits, forced assessments, and higher penalties. Learn more about managing compliance queries in our guide to HMRC Investigations and Nudge Letters.

How to Start an LPC Disclosure

Following the correct steps ensures your submission proceeds smoothly through HMRC systems.

Step 1: Notify HMRC

Start by informing HMRC of your intention to disclose your rental income. Submit your notification online through the official Digital Disclosure Service (DDS) on GOV.UK.

If you are reporting income for someone who has passed away, state clearly on the form that you act on behalf of an estate.

At the notification stage, you do not need to provide financial figures or calculate taxes owed. HMRC will review your details and issue a unique Disclosure Reference Number (DRN). Keep this reference for all communications.

Required Notification Information

Prepare these records before completing the initial notification form:

- Personal Details: Full name, current address, date of birth, email address, telephone number, Unique Taxpayer Reference (UTR), National Insurance Number, primary occupation, and VAT registration number (if registered).

- Property Information: Number of letting properties, full property addresses, original purchase price, acquisition dates, ownership split details, co-owner names and addresses, letting agency details, and reasons why rental income was not previously declared.

Calculating Taxes for Your LPC Disclosure

Once you receive your DRN, you have 90 days to prepare and submit your formal disclosure.

Step 2: Calculate Tax Owed

Determine total rental income for each undeclared tax year. Do not include income you already declared on previous tax returns.

Deduct allowable operational expenses to find your net taxable profit. Allowable expenses include property repairs, letting agent fees, safety certificates, property insurance, and direct running costs. Apply your annual Personal Allowance where available. Calculate Income Tax based on the tax brackets for each specific year.

Step 3: Make a Formal Offer

Complete the formal disclosure form using your figures. This submission creates a legally binding contract between you and HMRC once accepted.

Step 4: Submit Payment

Pay your outstanding balance within the 90-day window. Use the Payment Reference Number (PRN) provided on your notification letter.

If you cannot pay the full amount at once, contact the Let Property Campaign Helpline before submitting your disclosure. You must establish a formal payment arrangement before sending the disclosure. Reach out to our advisors through our contact page for professional support.

Penalties under the Let Property Campaign

HMRC calculates penalties as a percentage of the total unpaid tax. Penalty rates depend on your behavior, whether your disclosure was prompted or unprompted, and how well you cooperate.

You can earn penalty reductions based on your cooperation level across three categories:

- Telling (30% weight): Explaining how errors occurred.

- Helping (40% weight): Assisting HMRC in calculating exact liabilities.

- Giving access to records (30% weight): Providing full documentation promptly.

Penalties for Failure to Notify

These penalties apply if you never registered for Self Assessment to report property income.

| Behaviour Type | Unprompted Disclosure | Prompted Disclosure |

| Non-deliberate (within 12 months of tax due date) | 0% to 30% | 10% to 30% |

| Non-deliberate (12 months or more after tax due date) | 10% to 30% | 20% to 30% |

| Deliberate non-compliance | 20% to 70% | 35% to 70% |

| Deliberate and concealed non-compliance | 30% to 100% | 50% to 100% |

Example Case: HMRC discovered John owned a UK rental property with undeclared rental income. John knew about his filing duty but didn’t intend to conceal facts. HMRC classified this case as Prompted and Deliberate Failure to Notify, placing it in the 35% to 70% penalty bracket. John provided full cooperation, earning a 70% reduction within that range. His final calculated penalty was £9,039.

Penalties for Inaccurate Returns

These rates apply if you filed Self Assessment returns but omitted your rental figures.

| Behaviour Type | Unprompted Disclosure | Prompted Disclosure |

| Reasonable care taken | No penalty | No penalty |

| Careless error | 0% to 30% | 15% to 30% |

| Deliberate inaccuracy | 20% to 70% | 35% to 70% |

| Deliberate and concealed inaccuracy | 30% to 100% | 50% to 100% |

Example Case: Hailey noticed after submitting her tax return that she forgot her rental income. She submitted a voluntary correction through an Unprompted and Careless Inaccuracy filing. Her penalty range was 0% to 30%. Thanks to thorough cooperation, she received a 70% penalty reduction, bringing her final charge to £5,388.

Frequently Asked Questions

How does HMRC find out about undeclared rental income?

HMRC uses an automated data matching system called Connect. It gathers records from the Land Registry, tenant deposit schemes, letting agencies, local councils, mortgage applications, and electoral rolls. Discrepancies between this data and your tax returns trigger automatic compliance checks.

How far back can HMRC investigate under the LPC?

The time frame depends on your behavior. You go back up to 4 years if you took reasonable care. The window extends to 6 years for careless mistakes. If you deliberately concealed income, HMRC assesses back taxes up to 20 years.

What happens if I ignore an HMRC nudge letter?

Ignoring a nudge letter increases your risk. HMRC will likely open a formal tax investigation. You lose access to favorable voluntary penalty rates. Penalties can reach 100% of unpaid tax, and serious cases face criminal prosecution.

Does an LPC disclosure need to include other income sources?

Yes. When submitting an LPC disclosure, you must declare all previously unreported income or gains. This includes untaxed business profits, dividends, interest, or capital gains.

Can I pay my tax liability in installments?

Yes. If you cannot pay the balance immediately, you can negotiate a time-to-pay agreement. You must contact HMRC to set up this plan before submitting your 90-day disclosure form.

Can I use the LPC if HMRC has already started investigating me?

No. If HMRC opens a formal enquiry or compliance check before you notify them, you cannot use the campaign. You must disclose your income directly to the investigating officer, though prompt disclosure still helps reduce penalties.

| LPC Disclosure Guide: Step-by-Step HMRC Process Book Your Comprehensive Property Tax Review |