Maximizing tax deductions remains the most effective way for small business owners to shield their hard-earned revenues from unnecessary liability. Every dollar overlooked on a tax return is a dollar of pure profit surrendered to the Internal Revenue Service. Following major updates codified under the One, Big, Beautiful Bill Act (OBBBA), navigating the tax code requires careful adjustment to new thresholds, phased reductions, and updated structural frameworks.

Many entrepreneurs mistakenly assume their accountants catch every write-off. In reality, accounting systems only process the data they are given. If you fail to track specialized operational outlays, your business will miss major opportunities to lower its taxable base.

Strategic planning under the current tax code requires looking past the standard expense categories. By understanding the specific mechanisms governing asset depreciation, employee reimbursements, and structural deductions, you can dramatically shift your bottom-line profitability.

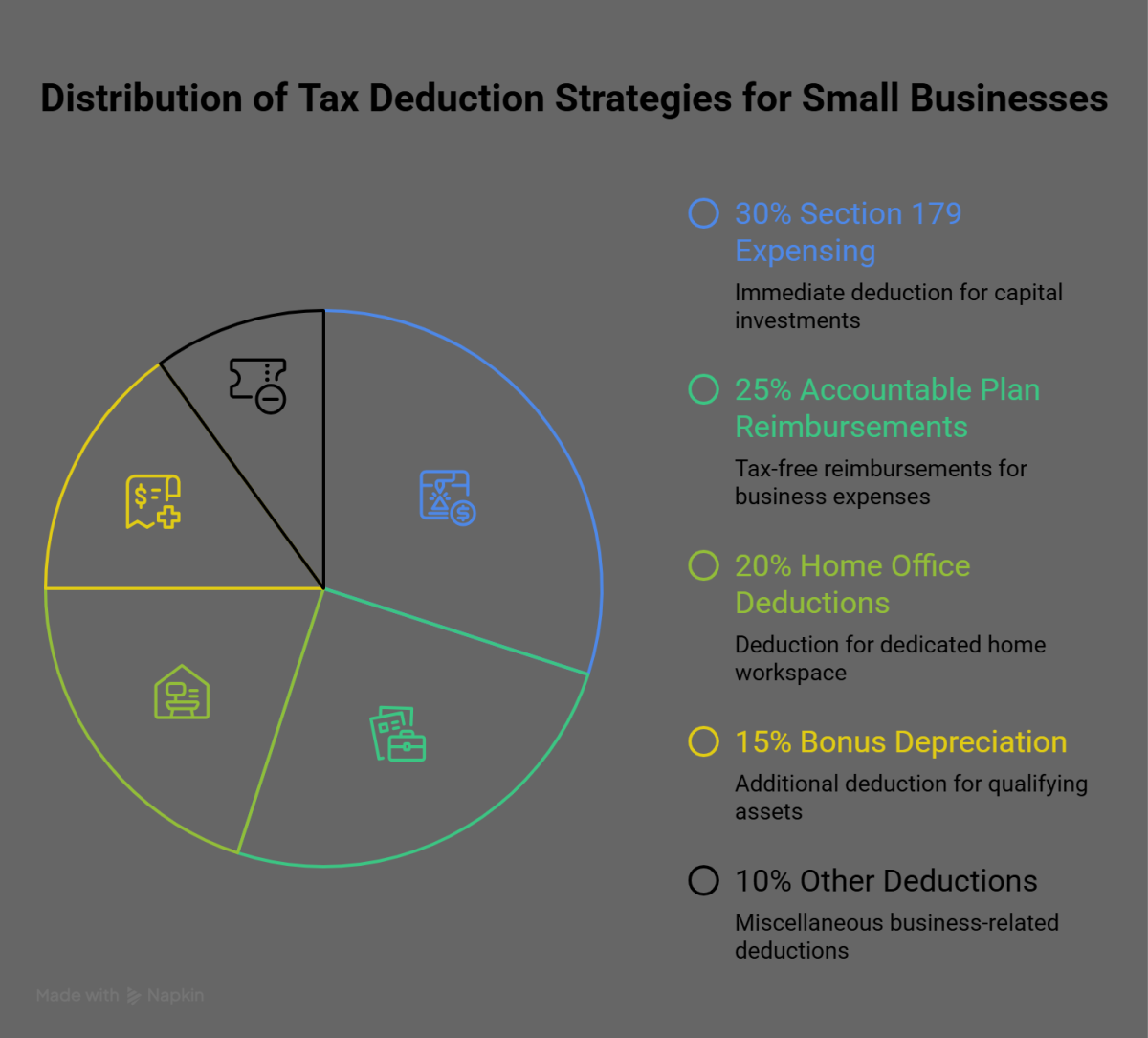

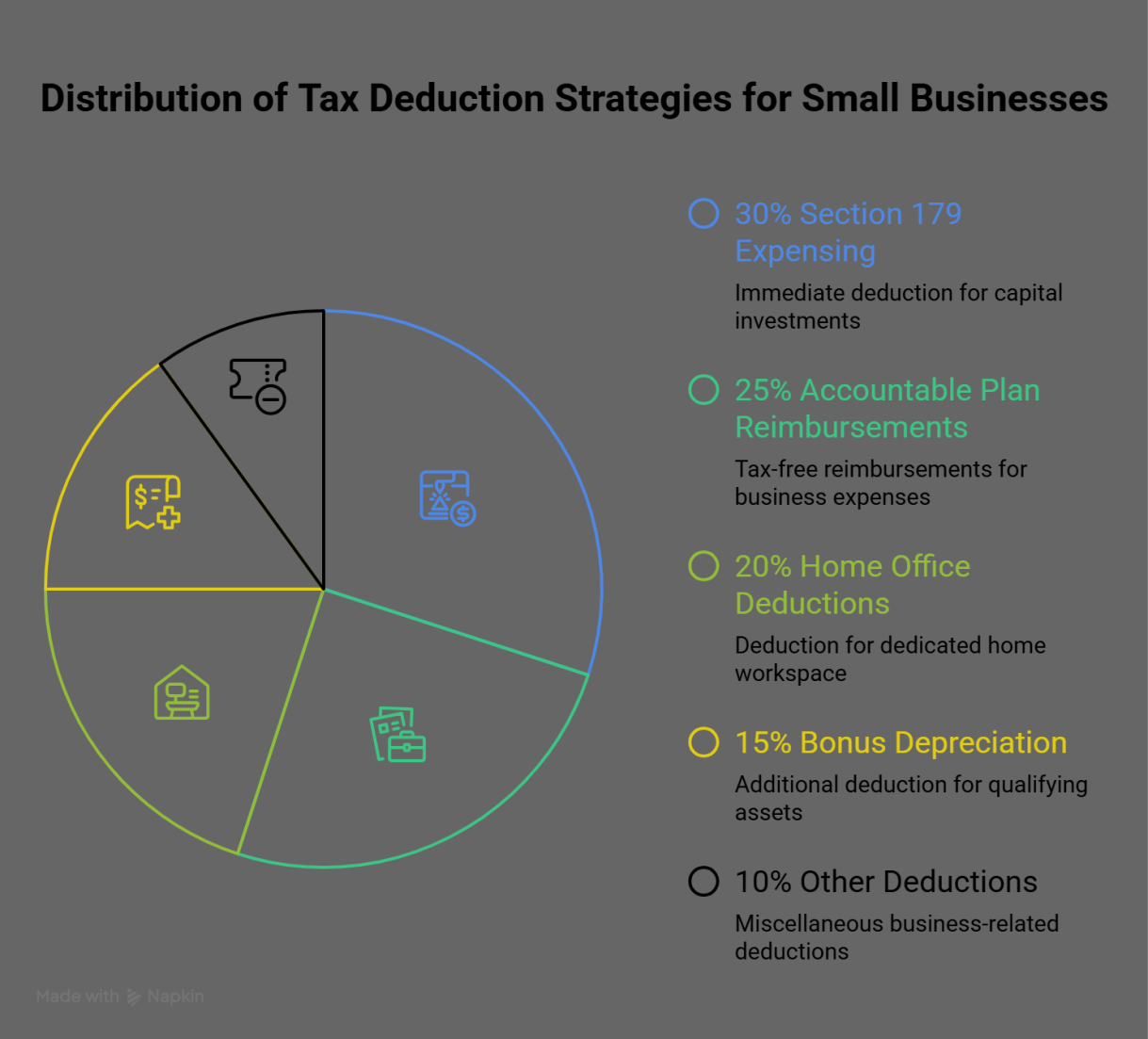

Overlooked Depreciation Strategies under Section 179

The Section 179 expensing framework provides small businesses with an immediate tool to offset capital investments. For the 2026 tax year, the maximum write-off threshold stands at $1.32 million, with the phase-out limit beginning at $3.29 million of qualifying property. This allows companies to deduct the full purchase price of qualifying equipment, machinery, and off-the-shelf software in the first year it is deployed.

The critical tactical error most owners make is focusing solely on the date of purchase. The IRS strictly mandates that an asset must be placed in service before December 31 to qualify for the deduction. If you purchase a server rack or specialized manufacturing machinery in late December, but the equipment sits in crates until January, you cannot claim the write-off for that tax year. It must be completely installed, configured, and operational.

Bonus depreciation complicates this strategy. Under current law, bonus depreciation has stepped down to 60% for property placed in service during 2026. Because Section 179 allows for a 100% upfront deduction up to the cap, business owners must sequence their asset deductions carefully. You should exhaust your Section 179 limits on assets that do not qualify for other preferential treatments before applying the 60% bonus depreciation to remaining capital expenditures.

Vehicles present another heavily restricted territory. The “SUV loophole” or Section 179 heavy vehicle deduction applies to vehicles with a Gross Vehicle W

eight Rating (GVWR) between 6,000 and 14,000 pounds. While passenger sedans face strict luxury automobile depreciation caps, heavy trucks, vans, and large SUVs used more than 50% for business can qualify for immediate expensing limits.

The Mechanics of an Accountable Plan

Many businesses reimburse workers or founders for out-of-pocket operational costs using simple, flat monthly stipends. Doing so turns tax deductions into taxable employee income. If you give a remote team member a flat $100 monthly allowance for internet and phone expenses without requiring documentation, the IRS classifies that payout as ordinary wages. This triggers payroll taxes for the company and income taxes for the recipient.

To secure tax deductions without generating tax liabilities, companies must implement a formal accountable plan under IRS Publication 463. This administrative framework relies on three rigid criteria:

- Business Connection: The expense must be ordinary and necessary, incurred while performing services for the company.

- Substantiation: The individual must provide documentary evidence, such as receipts, logs, or invoices, within a reasonable period (typically 60 days).

- Return of Excess: Any allowance overages must be returned to the business within a reasonable period (typically 120 days).

By utilizing an accountable plan, the business deducts the exact cost of home internet, cellular plans, travel, and specialized training as a direct operating expense. The employee receives the reimbursement completely tax-free. Transitioning from flat stipends to an accountable plan shields your company from unnecessary FICA exposure.

Home Office Deductions and Shared Utilities

The home office write-off remains heavily underutilized due to lingering fears of triggering an audit. This hesitation costs remote entrepreneurs thousands in potential tax deductions. To qualify under current IRS guidelines, a home workspace must meet two uncompromising conditions: it must be your principal place of business, and it must be used exclusively and regularly for work.

Exclusive use means the space cannot serve a dual purpose. A dedicated room or a clearly partitioned area of a room satisfies the rule. A desk placed in the corner of a child’s playroom or utilizing the dining room table does not. If a single square foot of the designated zone is used for personal activities, the entire space loses its eligibility.Owners can calculate the deduction using either the simplified method or the actual expense method:

| Method | Calculation | Maximum Limit | Recordkeeping Requirements |

| Simplified Method | Fixed rate of $5 per square foot | Up to 300 sq. ft. ($1,500 maximum) | Basic proof of square footage and business use |

| Actual Expense Method | Percentage of home square footage applied to total housing costs | Unlimited; proportional to actual costs | Detailed utility bills, rent receipts, mortgage interest statements, insurance |

For owners renting high-cost residential property, the actual expense method yields far greater tax deductions. If your dedicated workspace consumes 20% of your apartment’s total footprint, you can write off 20% of your rent, electricity, heating, trash collection, and renter’s insurance. Furthermore, home internet and cell phone connections should be isolated from the general home office calculation.

If you have a single internet line used for both commercial operations and family streaming, you can deduct the exact percentage dedicated to work. Maintaining a completely separate broadband connection or secondary cellular line dedicated solely to the company streamlines this process, allowing for a clean 100% deduction without complex tracking logs.

Maximizing the Qualified Business Income Deduction

The Section 199A Qualified Business Income (QBI) deduction allows eligible sole proprietors, partnerships, S corporations, and LLCs to deduct up to 20% of their qualified business income. For the 2026 tax year, the core inflation-adjusted thresholds sit at roughly $203,000 for single filers and $406,000 for married individuals filing jointly.

Once your pass-through net income crosses these specific limits, phase-out rules introduce complex restrictions based on the nature of your company. If your enterprise is classified as a Specified Service Trade or Business (SSTB)—which includes fields like law, medicine, consulting, financial services, and performing arts—the deduction begins to claw back. Above the upper phase-out limits, the QBI deduction drops to zero for SSTBs.

For non-SSTB businesses operating above the thresholds, the deduction is strictly limited to the greater of:

50% of the W-2 wages paid by the business

OR

25% of the W-2 wages + 2.5% of the unadjusted basis immediately after acquisition (UBIA) of qualified property

Pass-through owners can intentionally manage their QBI position through entity structuring and compensation design. If you operate an S corporation and your revenue is tracking well above the threshold, paying yourself too low a salary reduces the company’s total W-2 wage pool, which can inadvertently cap your overall QBI deduction.

Conversely, a sole proprietor facing an SSTB phase-out can lower their modified adjusted gross income (MAGI) by maximizing contributions to a solo 401(k) or a defined benefit plan, pulling their income back below the threshold to rescue the full 20% write-off.

Mileage, Travel, and S Corporation Compensation

The standard mileage rate has risen to 72.5 cents per mile, as detailed in IRS Notice 2026-10. This rate accounts for fuel, depreciation, insurance, and maintenance. Despite the higher rate, owners frequently forfeit this deduction by failing to maintain a contemporaneous mileage log. Retrospective logs reconstructed at the end of the year via calendar entries often fail to survive IRS scrutiny during an examination. A valid log must record the date, destination, exact business purpose, and starting and ending odometer readings for every trip.

For heavy vehicle usage, calculating actual expenses—including actual fuel costs, repairs, insurance, and structural depreciation—often yields greater tax deductions than the standard mileage rate. However, once you choose the actual expense method for a leased vehicle, you cannot switch to the standard mileage rate in subsequent years.

Travel expenses outside your local tax home present another area of lost opportunity. While business meals remain restricted to a 50% deduction rule, related travel costs like airfare, lodging, dry cleaning, and rideshares are 100% deductible. When combining business trips with personal vacation days, the primary purpose of the trip must be commercial.

If a trip is primarily personal, you cannot deduct the transportation costs, though you can still claim specific expenses incurred on the days dedicated purely to business activities. For S corporation owners, vehicle and travel deductions intersect directly with owner compensation audits. The IRS is actively targeting S corporations that pay owners minimal W-2 salaries to avoid payroll taxes while taking large corporate distributions.

Your salary must reflect “reasonable compensation” for your industry and role. Failing to balance this structure properly can lead the IRS to reclassify your distributions as wages, wiping out planned savings and exposing the business to back taxes, interest, and substantial penalties.

Frequently Asked Questions

What are the most common tax deductions small businesses miss?

Small business owners frequently miss tax deductions tied to localized operational costs, including home office internet allocations, localized vehicle mileage tracked via contemporaneous logs, and capital purchases managed via Section 179. Many also forfeit savings by using flat employee stipends instead of formalized, tax-free accountable plans, which converts clean deductions into taxable payroll liabilities.

How do I claim a deduction for a home office setup?

To claim home office tax deductions, your workspace must serve as your principal place of business and be used exclusively for commercial activities. You can calculate the deduction using the simplified method at five dollars per square foot up to 300 square feet, or the actual expense method to deduct a proportional percentage of rent, utilities, and insurance.

Are business meals fully deductible this year?

Business meals are not fully deductible; they are subject to a strict 50% limitation. To qualify for this partial write-off, the food and beverages must not be lavish or extravagant under the circumstances, and the owner or an employee must be present when the meal is provided to a client or prospect.

Can I deduct vehicle expenses using both mileage and actual costs?

You cannot combine both methods for a single vehicle within the same tax year; you must choose between the standard mileage rate or the actual expense method. If you select the standard mileage rate in the first year the car is available for use, you can switch to actual expenses later, but leasing structures lock you into your initial choice.

What software subscriptions qualify for a business write-off?

Any software subscription directly required to operate, market, or secure your company qualifies for a complete operational deduction. This includes accounting platforms, customer relationship management tools, web hosting, cybersecurity protocols, and specialized industry applications, provided they are used exclusively for your commercial operations.

How does the Section 179 deduction work for equipment purchases?

The Section 179 provision allows companies to deduct the complete purchase price of qualifying equipment and software up front, rather than depreciating the asset over several years. The equipment must be fully placed in service and functional within the business before midnight on December 31 of the filing year.

What is the difference between a tax deduction and a tax credit?

A tax deduction reduces your total taxable income, lowering the base upon which your liability is calculated based on your marginal bracket. A tax credit provides a dollar-for-dollar reduction of your final tax liability, making credits inherently more valuable than deductions when optimizing your overall financial return.

Can startup costs be deducted before the business officially opens?

The IRS allows entrepreneurs to deduct up to $5,000 of qualifying startup costs and an additional $5,000 of organizational costs in the year active operations begin. These upfront tax deductions phase out dollar-for-dollar if your total startup expenditures surpass the designated threshold, with any remaining balances amortized over a 180-month period.