Maximizing legitimate tax deductions remains the most effective action an enterprise leader can take to protect corporate revenue. Pass-through business structures provide excellent operational flexibility, but they naturally expose your net profits to aggressive self-employment levies. Every dollar you fail to account for represents an unnecessary transfer of wealth directly to the federal government.

Following extensive updates codified under the One, Big, Beautiful Bill Act (OBBBA), legal avoidance requires a precise understanding of evolving depreciation rules, structural changes, and administrative frameworks. Many founders assume standard accounting applications capture every available offset, yet software only interprets the information it receives. You must actively implement structural tax reduction mechanisms to ensure your company keeps its hard-earned capital.

Optimizing your annual filing requires shifting away from basic expense logging. By adjusting your entity classifications, implementing specialized corporate reimbursement frameworks, and maximizing retirement allocations, you can structurally reduce your taxable base.

Entity Restructuring and the S Corporation Mechanism

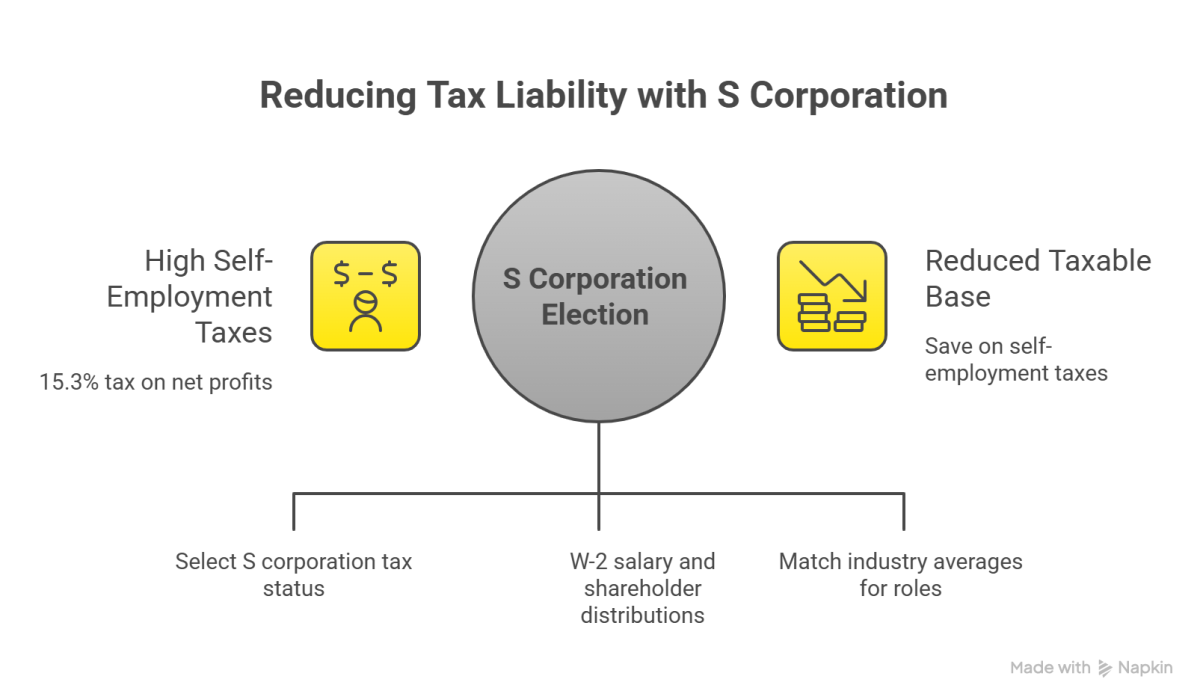

The default pass-through classification forces a single-member LLC to pay a 15.3% self-employment tax on 100% of its net operational profits. You can legally alter this financial trajectory by filing IRS Form 2553 to select an S corporation tax status. This structural optimization preserves your limited liability protections while shifting how the federal government assesses payroll taxes on your distributions.

Once the S corporation status takes effect, you divide your corporate earnings into two separate components: a W-2 salary and shareholder distributions. Your W-2 wage remains subject to standard FICA obligations, while the remaining operational profits flow to your personal return entirely free from self-employment taxes.

For example, under a standard LLC structure with a net income of $140,000, the entire amount is subject to the 15.3% self-employment tax, resulting in a total FICA tax liability of approximately $21,420. By optimizing as an S corporation, you can split that same $140,000 net income into a reasonable W-2 salary of $65,000 and a shareholder distribution of $75,000. FICA taxes only apply to the salary portion, while the distribution portion remains entirely exempt, saving you roughly $11,475 in self-employment taxes.

The Internal Revenue Service closely monitors S corporation business owners to ensure W-2 compensation matches industry averages for comparable roles. If you set an unrealistically low wage to maximize tax-exempt distributions, the government can reclassify your entire distribution pool during an audit. This strategy typically yields clear financial advantages once your company’s clean net income safely surpasses $75,000 annually.

Implementing Accountable Plans for Clear Deductions

Many managers distribute flat monthly stipends to cover team internet fees, mobile connections, or travel costs. The IRS explicitly treats undocumented monthly stipends as ordinary taxable wages, which increases your corporate payroll obligations.

To convert personal operational outlays into clean corporate tax deductions, your company must formalize a written Accountable Plan under IRS Publication 463. This administrative framework enables owners and staff to claim tax-free reimbursements for expenses incurred while advancing business operations.

An eligible reimbursement process demands absolute adherence to three core statutory requirements. First, the expense must have a clear commercial intent, meaning it is ordinary and necessary for your specific industry. Second, the claimant must provide proportional verification by submitting receipts, mileage records, or invoices within 60 days. Third, any excess funds advanced must return to the corporate account within 120 days.

By leveraging a formal accountable plan, your business can claim direct tax deductions for shared home utilities, digital tool subscriptions, and vehicle mileage without triggering employee-level income taxes.

Home Office Deductions and Boundary Management

The home office write-off offers a substantial tax benefit, yet many remote business owners avoid it out of audit anxiety. You can claim these tax deductions safely by maintaining clear physical and functional boundaries within your primary residence. The IRS demands that your workspace serve as your principal place of business and remain exclusively dedicated to commercial activity.

Dual-use areas do not qualify for this treatment. If your workspace contains a guest bed or double-functions as a family entertainment zone, the entire room loses its tax-deductible status. You can compute your deduction using the simplified method or the actual expense method.

| Measurement Approach | Calculation Metric | Maximum Allowance | Recordkeeping Rules |

| Simplified Method | Fixed $5 per square foot | Up to 300 sq. ft. ($1,500 maximum) | Basic verification of area dimensions |

| Actual Expense Method | Percentage of residential square footage applied to housing costs | Proportional to total expenses | Itemized records of rent, utilities, insurance |

For companies leasing high-value residential property, tracking actual expenditures regularly generates far superior tax deductions. If your workspace occupies 25% of your home’s total area, you can write off 25% of your rent, electrical grid costs, and seasonal climate control bills.

Section 199A and the Pass-Through Shield

The Section 199A Qualified Business Income (QBI) deduction enables eligible pass-through owners to deduct up to 20% of their net business income before ordinary income taxes apply. For the 2026 tax year, the baseline threshold limits match inflation adjustments, sitting at $201,750 for single filers and $403,550 for married individuals filing joint returns.

When your pass-through net income exceeds these limits, complex statutory phase-outs apply based on your industry classification. If your firm operates as a Specified Service Trade or Business (SSTB)—such as a consulting agency, medical practice, law firm, or financial advisory—the deduction phases down and eventually hits zero. Under the OBBBA, the phase-in range itself has been liberalized, which gives business owners a larger cushion before the full limitation completely restricts the write-off.

For non-SSTB operations with revenues exceeding the caps, the deduction relies on a specific wage and property limitation:

Maximum Deduction =max left 50% text of corporate W-2 wages 25% text of W-2 wages + 2.5% of the property basis

If your service-based company approaches the threshold limit, you can protect your QBI deduction by intentionally reducing your personal Modified Adjusted Gross Income (MAGI). Directing corporate profits into pre-tax retirement structures lowers your personal taxable income, keeping your business beneath the phase-out boundary.

Maximizing 100% Bonus Depreciation under the OBBBA

Following the legislative implementation of the One Big Beautiful Bill Act (OBBBA), 100% bonus depreciation has been permanently restored for qualified business property placed in service during 2026. This adjustment provides an immediate cash flow benefit, completely reversing the previous phase-down timelines that threatened to phase the benefit out entirely.

When your company purchases qualifying assets like network servers, industrial machinery, field equipment, or specialized commercial software, you can write off the entire cost in the first year.

To secure this deduction, you must place the asset into active service before midnight on December 31. Purchasing equipment that remains in shipping crates until the following January postpones the entire tax write-off by a full calendar year. IRS Notice 2026-11 confirms that both the contract acquisition date and the operational placed-in-service date must comply with these timing rules to capture the full first-year value.

Frequently Asked Questions

How do LLC tax write offs work?

LLC tax write offs work by reducing your business’s net taxable income before profits flow through to your personal tax return. When you claim eligible tax deductions for ordinary and necessary business expenses, you lower the overall profit base that is subject to federal income and self-employment taxes.

How much can an LLC write off?

An LLC can write off any amount of eligible expenses, provided the costs are ordinary, necessary, and directly connected to running the business. There is no flat statutory limit on total operating tax deductions, but capital investments and startup costs must follow specific annual thresholds and depreciation schedules.

How do LLC owners avoid taxes?

LLC owners avoid taxes legally by maximizing deductions, establishing corporate accountable plans, and electing S corporation status to shield distributions from self-employment levies. They also utilize advanced asset depreciation strategies under the OBBBA framework and maximize pre-tax contributions to self-employed retirement accounts to lower their total adjusted gross income.

Can a single-member LLC write off expenses?

Yes, a single-member LLC can write off expenses directly by documenting ordinary and necessary business outlays on Schedule C of IRS Form 1040. These tax deductions lower the pass-through income figure that is ultimately subject to personal income tax and federal self-employment tax assessments.

Can you deduct LLC expenses on personal taxes?

You can deduct LLC expenses on personal taxes because default LLC structures operate as pass-through entities where all financial activities flow directly to your personal return. You report these business tax deductions on Schedule C or Schedule E, which ultimately reduces your overall personal tax obligation.

What is the difference between a deductible expense and a capital expenditure?

A deductible expense is an operational cost completely written off within the current tax year, such as office rent, marketing, or utilities. A capital expenditure represents an investment in a long-term asset that must be depreciated over its useful life, unless accelerated by Section 179 or bonus depreciation rules.

What documentation is required to support LLC write-offs?

To support LLC tax deductions, the IRS requires comprehensive documentation, including itemized receipts, corporate bank statements, canceled checks, paid invoices, and contemporaneous travel logs. These records must clearly demonstrate the exact amount, transaction date, vendor identity, and specific commercial purpose of each claimed expenditure.

What business expenses are tax deductible?

Business expenses are tax deductible if they are universally recognized as ordinary and necessary within your specific industry. Common examples include corporate software subscriptions, marketing campaigns, professional legal advice, dedicated home office facilities, employee payroll costs, and vehicle mileage accrued during commercial transport operations.