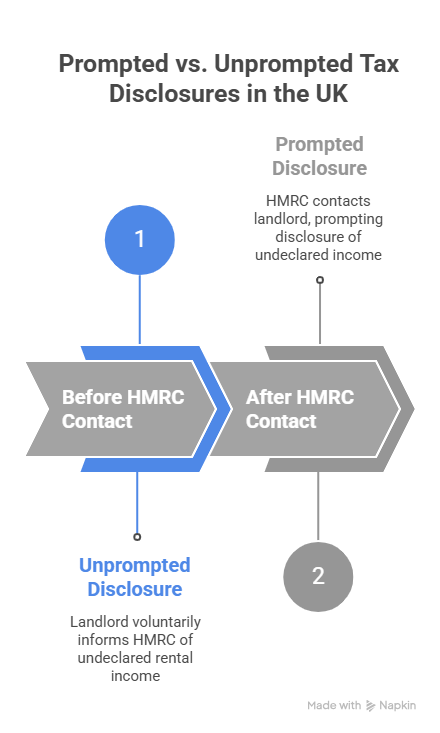

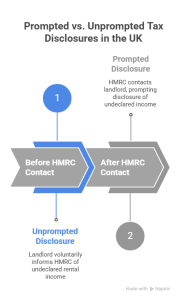

If you are a landlord with undeclared rental income, you are likely standing at a digital crossroads. On one path, you come forward voluntarily to settle your debts. On the other, you wait until a brown envelope from HMRC arrives on your doorstep. In the world of UK tax compliance, these two paths are known as Prompted vs Unprompted disclosures.

Understanding the difference between these two categories isn’t just academic—it is a financial imperative. The “Let Property Campaign” (LPC) is designed to be a bridge back to compliance, but the toll you pay to cross that bridge depends entirely on who starts the conversation.

In this deep-dive guide, we will break down the mechanics of the Let Property Campaign, compare the penalty structures of prompted vs. unprompted disclosures, and explain why the timing of your disclosure is the single most significant factor in protecting your assets.

Featured Snippet: What is the difference between Prompted vs Unprompted disclosures?

The primary difference lies in timing and cost. An unprompted disclosure occurs when a landlord voluntarily notifies HMRC of unpaid tax before any inquiry is opened. A prompted disclosure happens after HMRC contacts the landlord (often via a “nudge letter”). Unprompted disclosures carry significantly lower penalties, often starting at 0% for “reasonable care” errors.

The Anatomy of the Let Property Campaign

The Let Property Campaign is a specific disclosure opportunity for individual landlords letting out residential property. It is not available to limited companies or those letting out commercial premises.

HMRC’s goal with this campaign is efficiency. It is cheaper for the government if you do the math and hand over the tax than it is for them to assign an inspector to hunt you down. To incentivize this, they created a sliding scale of leniency.

Why Does HMRC Distinguish Between the Two?

HMRC rewards “honesty before discovery.” If you realize you’ve made a mistake and move to fix it, you are seen as a low-risk taxpayer who made an error. If you only move to fix it because you were caught, you are viewed as a high-risk taxpayer who was potentially trying to evade their obligations.

Defining the Unprompted Disclosure

An unprompted disclosure is a proactive strike. It means you have contacted HMRC to tell them you have unpaid tax before they have sent you a letter, opened an inquiry, or even hinted that they are looking at your affairs.

The Financial Benefits of Being Proactive

The most compelling reason to stay in the “unprompted” category is the penalty floor. For errors made despite taking “reasonable care,” the penalty can be as low as 0%. Even for “careless” behavior, the unprompted penalty can remain at 0% if you provide full assistance to HMRC.

The Psychological Peace of Mind

When you lead the disclosure, you control the narrative. You aren’t responding to accusations; you are presenting a professional, calculated summary of your affairs. This often leads to a much smoother settlement process and a faster conclusion.

Defining the Prompted Disclosure

A prompted disclosure is a reactive move. This usually begins when you receive a “nudge letter” or a formal notice of inquiry.

The “Nudge Letter” Trap

HMRC sends out thousands of these letters to landlords in London, Windsor, Oxford, and Reading. The letter essentially says, “We have information that you have rental income; check your records and let us know.” The moment that letter is generated and sent, your window for an unprompted disclosure has effectively slammed shut.

The Cost of Hesitation

In a prompted scenario, the “penalty floor” rises. HMRC assumes that you wouldn’t have come forward if they hadn’t nudged you. Therefore, the minimum fine for “careless” behavior jumps from 0% to 15%. If the behavior is deemed “deliberate,” the prompted penalties can be eye-watering, often reaching 35% to 70% of the tax due.

Detailed Comparison: Prompted vs. Unprompted

To help you visualize the stakes, consider this comparison of the two disclosure types across different behavioral categories.

Behavioral Categorization: The Secret Ingredient

HMRC doesn’t just look at when you disclosed; they look at why you didn’t pay in the first place. This behavior dictates which row of the penalty table you fall into.

Reasonable Care: You kept records and tried to follow the rules, but perhaps you misunderstood a complex deduction or a change in law.

Careless: You didn’t keep good records, or you “forgot” about the income for several years without checking your obligations.

Deliberate: You knew you owed tax, but you decided not to pay it.

Deliberate & Concealed: You knew you owed tax and took active steps to hide it (e.g., using offshore accounts or false names).

The Multiplier Effect: If you are “Deliberate” and “Prompted,” you are looking at the highest possible financial punishment available under the Let Property Campaign.

The Disclosure Timeline: From Start to Finish

Regardless of whether your disclosure is prompted or unprompted, the technical process follows a similar 4-step framework.

1. Notification

You notify HMRC that you intend to make a disclosure under the campaign. For unprompted cases, this is done via the Digital Disclosure Service (DDS). For prompted cases, you usually reply to the specific officer or department that contacted you.

2. Calculation (The 90-Day Clock)

Once notified, you have 90 days to prepare your figures. This includes:

Mortgage interest relief (restricted to basic rate tax credit).

Calculation of tax, interest, and your proposed penalty percentage.

3. Submission

You submit your final disclosure. At this stage, you must pay the amount in full or have a payment plan ready to propose.

4. Acceptance

HMRC reviews your submission. If they agree with your behavior categorization and your figures, they will issue an acceptance letter. The case is then closed.

Strategy: How to Move from “Prompted” back to “Leniency”

If you have already received a nudge letter, you might feel like you’ve already lost. While you can’t technically revert to “unprompted” status, you can still significantly reduce your penalties within the “prompted” range through Quality of Disclosure.

HMRC reduces fines based on:

Telling: Being 100% transparent about the errors.

Helping: Responding to their queries within days, not weeks.

Giving Access: Providing all bank statements and records without being forced to via a formal notice.

By maximizing these three factors, a landlord in Slough or Reading who has been prompted can often pull their penalty down toward the minimum floor of that category.

Case Study: The Proactive vs. The Reactive Landlord

Landlord X (Windsor): Owns a flat and hasn’t declared income for 6 years. They read about the Let Property Campaign and hire an expert to file an unprompted disclosure.

Outcome: Behavior is judged “Careless.” Penalty is negotiated to 0% because they provided full assistance and came forward voluntarily.

Landlord Y (Oxford): Owns an identical flat with the same 6-year history. They wait. HMRC sends a nudge letter. Landlord Y eventually discloses.

Outcome: Behavior is also “Careless.” Because it was prompted, the minimum penalty is 15%.

On a tax bill of £20,000, Landlord Y pays £3,000 more than Landlord X for the exact same mistake—simply because of the timing.

Serving Landlords in the South East and Beyond

Tax compliance isn’t just about numbers; it’s about local context. We provide specialized Let Property Campaign support across key regions:

London: Dealing with high-volume rental income and the complexities of the Non-Resident Landlord Scheme (NRLS).

Windsor & Reading: Supporting landlords with high-value portfolios where “deliberate” accusations from HMRC can lead to massive financial losses.

Oxford & Slough: Helping academic and professional landlords fix historical errors before they trigger a full HMRC investigation.

Prompted vs Unprompted

Overview: Quick Differences

Unprompted: Voluntary, happens before HMRC contact. Lowest penalties (0% minimum).

Prompted: Happens after HMRC contact (Nudge letters). Higher penalty floors (15% minimum for careless).

Common Goal: Both use the Let Property Campaign to settle back tax and interest.

Actionable Advice: If you haven’t been contacted yet, disclose immediately to lock in “Unprompted” status.

FAQ: People Also Ask

1. What exactly triggers a “prompted” status?

HMRC considers a disclosure prompted if it is made at a time when they have reason to believe that tax has been underpaid. This is almost always triggered by the issuance of a “nudge letter” or a notice of an intended tax return inquiry.

2. Can I still use the Let Property Campaign if I got a letter?

Yes. Even if you are prompted, the Let Property Campaign is usually the most efficient way to settle. It is still better than a full, intrusive tax investigation which could look into your lifestyle, business, and other income sources.

3. Does a phone call from HMRC count as a “prompt”?

Generally, yes. If HMRC contacts you specifically about your property income, any disclosure made after that point is likely to be treated as prompted.

4. How far back does an unprompted disclosure go?

The “look-back” period depends on behavior, not the prompt status. If you were careless, it’s 6 years. If it was a reasonable excuse, it’s 4. If it was deliberate, it can be up to 20 years.

5. What if I genuinely didn’t know I had to declare it?

This is often categorized as “Careless.” While “Ignorance of the law is no excuse” is a legal maxim, an unprompted disclosure for a careless mistake often results in a 0% penalty if you help HMRC resolve the matter quickly.

6. Is the interest higher for prompted disclosures?

No, the statutory interest rate is the same. However, because prompted disclosures often take longer to resolve (due to HMRC’s involvement), more interest may accrue over time.

Why Timing is Everything

The difference between a Prompted vs Unprompted Let Property Campaign disclosure is the difference between being a “partner” in the process and being a “target.”

HMRC’s “Connect” system is running 24/7, matching Land Registry data with your tax returns. If there is a gap, a nudge letter is inevitable. By moving now—on your own terms—you drastically reduce your penalties, limit the number of years HMRC investigates, and save yourself the immense stress of a forced inquiry.

Are you ready to clear your record and protect your property investment? Learn More

If you are a landlord who has fallen behind on your tax obligations, the Let Property Campaign offers a vital pathway to regularize your affairs. However, one of the most misunderstood aspects of making a disclosure is determining whether you have a Let Property Campaign reasonable excuse for your failure to notify HMRC of your rental income. Understanding this nuance is the difference between facing a 0% penalty and a substantial fine that eats into your property investment returns.

In this comprehensive guide, we will explore the specific scenarios HMRC deems acceptable, the legal thresholds for “reasonable care,” and how you can structure your disclosure to protect your reputation and your wallet.

Featured Snippet: What is a ‘Reasonable Excuse’ for HMRC?

A reasonable excuse for the Let Property Campaign is something that stopped you from meeting a tax obligation that you took reasonable care to meet. HMRC considers circumstances such as serious illness, bereavement, unexpected postal delays, or relying on professional advice that proved incorrect, provided you corrected the error as soon as the excuse ended.

The Significance of the ‘Reasonable Excuse’ in Your Disclosure

When you engage with the Let Property Campaign, you aren’t just handing over numbers; you are providing a narrative of your behavior. HMRC uses this behavior to determine the level of penalty you will pay.

If you can demonstrate a “reasonable excuse,” you may be able to avoid penalties entirely. Without one, HMRC may categorize your behavior as “careless” or even “deliberate,” which can lead to fines ranging from 15% to 100% of the tax due. For landlords in high-value areas like London or Windsor, these percentages translate into thousands of pounds.

What HMRC Typically Accepts as a Reasonable Excuse

HMRC does not provide an exhaustive list, as every landlord’s situation is unique. However, based on case law and HMRC’s own internal manuals, the following scenarios are frequently accepted as a Let Property Campaign reasonable excuse:

1. Bereavement and Serious Illness

If the death of a close relative or a life-threatening illness occurred shortly before your tax deadline, HMRC is generally sympathetic. The key is showing that the event caused a genuine disruption that made it impossible to manage your tax affairs.

2. Reliance on Professional Advice

If you appointed a professional—such as an accountant or a solicitor—and they provided you with incorrect advice regarding your rental income, this can count as a reasonable excuse. However, you must prove that you provided that professional with all the necessary facts and that it was reasonable for you to rely on their expertise.

3. Unexpected Hospital Stays

A sudden, prolonged stay in the hospital that prevented you from accessing your records or meeting filing deadlines is a classic example of an excuse “outside of your control.”

4. Technical Failures (HMRC or Postal)

If HMRC’s online systems were down for a prolonged period, or if there was a documented national postal strike or service failure that prevented documents from arriving, these are valid excuses.

Domestic or Personal Hardship

In extreme cases, such as escaping domestic abuse or facing homelessness, HMRC recognizes that tax compliance may not have been physically or mentally possible.

What Does NOT Count as a Reasonable Excuse?

It is equally important to know what HMRC will reject. Many landlords in Oxford or Reading find themselves in trouble because they rely on “myths” rather than tax law.

“I didn’t know I had to pay tax”: Ignorance of the law is rarely accepted as a reasonable excuse. As a landlord, you are expected to understand your basic legal obligations.

“My tenant didn’t pay me on time”: While this affects your cash flow, it does not exempt you from the requirement to report the income you did receive or notify HMRC of the rental business.

“The HMRC website is too complicated”: HMRC expects you to seek help (either from them or a professional) if you find the process difficult.

“I relied on my partner/spouse”: You are legally responsible for your own tax affairs. Unless your partner had a specific legal duty or there is a “reasonable excuse” for their failure that extends to you, this will likely be categorized as “careless.”

The ‘Reasonable Care’ Comparison: Excuse vs. Carelessness

Understanding where you fall on the spectrum of behavior is essential for your Let Property Campaign submission.

Behavior Level

Criteria

Typical Penalty (Unprompted)

Reasonable Excuse

An exceptional event stopped you from filing, despite your best efforts.

0%

Reasonable Care

You made a mistake, but you acted as a “prudent person” would.

0%

Careless

You failed to take enough care, but the omission wasn’t intentional.

0% – 30%

Deliberate

You knew you owed tax but chose not to declare it.

20% – 70%

How to Prove a Reasonable Excuse: A Step-by-Step Strategy

If you believe you have a valid excuse, you must present it clearly within your disclosure narrative. Here is the framework we use for our clients:

Step 1: Identify the Timeline

HMRC requires that the excuse existed at the time the tax obligation was missed. If your “excuse” happened three years after you started renting out a property in Slough without declaring it, it won’t apply to the earlier years.

Step 2: Show When the Excuse Ended

A reasonable excuse only lasts as long as the circumstance exists. If you were ill in 2022 but recovered in 2023, you must show that you took steps to fix your tax affairs “without unreasonable delay” once you were healthy again.

Step 3: Gather Evidence

HMRC will not take your word for it. You should provide:

Medical notes or hospital discharge papers.

Death certificates for bereavement claims.

Copies of incorrect advice received from previous professionals.

Correspondence with HMRC regarding technical issues.

Step 4: Draft the Disclosure Narrative

This is where professional help is invaluable. Your narrative should link the event directly to your failure to notify. Instead of saying “I was stressed,” say “Due to [Event], I was unable to access my financial records or fulfill my statutory duties under the Taxes Management Act 1970.”

The Role of a Specialist Accountant

Navigating the Let Property Campaign is complex. HMRC’s “Connect” database is now linked to the Land Registry and bank accounts, meaning they likely already know about your rental income in Reading or London.

A specialist accountant doesn’t just do the math; they act as your advocate. We help you determine if your situation meets the threshold for “reasonable care” or a “reasonable excuse,” ensuring you don’t overpay on penalties.

Our expertise in the Let Property Campaign is tailored to the specific needs of landlords in various regions:

Windsor: Managing high-value disclosures where penalty percentages can be exceptionally high.

Oxford: Assisting academic and professional landlords who may have inadvertently missed filings due to international work or complex portfolios.

London: Navigating the Non-Resident Landlord Scheme (NRLS) and multi-property disclosures.

Reading & Slough: Supporting local landlords who have received “nudge letters” and need to act quickly to secure “unprompted” status.

Overview Optimization: Quick Facts

Definition: A reasonable excuse is an exceptional circumstance that prevented you from fulfilling your tax duties despite taking reasonable care.

Common Examples: Serious illness, bereavement, professional advice errors, and technical failures.

Invalid Excuses: Lack of funds, ignorance of the law, or simple oversight.

Penalty Impact: Proving a reasonable excuse can reduce your penalty to 0%.

Action Needed: You must rectify the tax position as soon as the excuse ends to remain eligible for leniency.

FAQ: People Also Ask

1. Can “mental health issues” count as a reasonable excuse?

Yes. HMRC recognizes that serious mental health conditions can be just as debilitating as physical ones. However, you will usually need medical evidence showing that the condition specifically prevented you from managing your financial affairs.

2. What if I was living abroad and didn’t realize UK tax applied?

HMRC generally considers it the landlord’s responsibility to research the tax laws of the country where the property is located. This is rarely accepted as a “reasonable excuse,” but it may be categorized as “careless” rather than “deliberate,” which still helps lower the penalty.

3. How quickly do I need to disclose once the excuse ends?

HMRC uses the term “without unreasonable delay.” Generally, this means you should take action within 30 to 90 days of the excuse ceasing. Waiting a year after recovering from an illness to make a disclosure will likely invalidate the excuse.

4. Can I use a reasonable excuse if I received a nudge letter?

If you received a “nudge letter,” your disclosure is technically “prompted.” You can still claim a reasonable excuse for the original failure to notify, but the fact that HMRC found you first makes the argument harder to win.

5. Does being “too busy” count?

No. Being a busy professional in London or Windsor is never accepted as a reasonable excuse. HMRC expects you to delegate your tax affairs to a professional if you do not have the time to manage them yourself.

6. What if my accountant made the mistake?

If your accountant made a technical error despite you providing all the correct information, this is a very strong candidate for a reasonable excuse. You are essentially claiming you took “reasonable care” by hiring a professional.

7. Can “lack of money” be an excuse?

No. A lack of funds to pay the tax is not an excuse for failing to disclose the income. You should disclose the income and then negotiate a payment plan (Time to Pay) with HMRC.

To ensure you are fully informed about your obligations, we recommend reviewing these resources:

The Let Property Campaign is a fair system, but it is not a lenient one for those who are unprepared. Claiming a Let Property Campaign reasonable excuse requires more than just a good story; it requires evidence, a solid understanding of tax law, and a correctly structured disclosure.

If you are unsure whether your circumstances qualify, the worst thing you can do is wait. The interest on unpaid tax grows daily, and the risk of a “prompted” inquiry increases every time HMRC’s “Connect” system runs a data match.

By acting now and seeking professional representation, you can ensure that your behavior is categorized fairly, your penalties are minimized, and your property business can move forward with a clean slate.

Protect your reputation and your investment today.

If you are a landlord with undeclared rental income, you’ve likely heard whispers of a special HMRC scheme that allows you to “come clean” on favorable terms. But as we move deeper into the year, many property owners are asking: Is the Let Property Campaign still running in 2026? The short answer is a resounding yes. However, while the opportunity remains open, the technology HMRC uses to find you has become significantly more aggressive.

In this comprehensive guide, we will explore why the Let Property Campaign remains one of the longest-running disclosure opportunities in UK tax history, what has changed for landlords this year, and why waiting any longer to settle your affairs could be the most expensive mistake of your financial life. Whether you are managing properties in Windsor, Oxford, or London, understanding the current status of this campaign is vital for your peace of mind.

Featured Snippet: Is the Let Property Campaign active in 2026?

Yes, the Let Property Campaign is still active in 2026. It remains an open-ended disclosure opportunity for individual landlords to declare unpaid rental tax. By coming forward voluntarily before HMRC contacts you, you can benefit from lower penalty rates and a structured pathway to regularize your tax affairs.

The Longevity of the Let Property Campaign: Why is it Still Here?

The Let Property Campaign first launched in 2013. Most tax amnesties or “campaigns” last for 12 to 18 months, yet here we are in 2026, and the digital doors are still wide open. Why?

1. The Digital Revolution in Tax Tracking

HMRC’s “Connect” computer system is the primary reason the campaign hasn’t closed. Connect now cross-references billions of data points, including Land Registry records, bank interest, estate agent lists, and even short-term let platforms like Airbnb. Because the data is constantly updating, HMRC continuously finds “new” landlords who haven’t registered for Self Assessment.

2. Efficient Revenue Collection

It is far cheaper for the Treasury if you calculate your own tax and hand it over than it is for them to hire an inspector to perform a manual audit. The campaign serves as a “self-service” portal for compliance, which remains a priority for the government in 2026 as they look to close the tax gap.

3. The Surge in Professional Landlords

With the shifting economy, more people have become “accidental landlords”—perhaps moving in with a partner or inheriting a home. HMRC recognizes that many people fall into non-compliance through ignorance rather than malice, and the LPC provides a way to bring these people into the system without the need for criminal proceedings.

What Has Changed for Landlords in 2026?

While the campaign itself is the same, the environment surrounding it has shifted. If you are a landlord in Reading or Slough, you are operating under a different set of pressures than you were a few years ago.

The “Nudge Letter” Evolution

In 2026, HMRC has moved from broad-spectrum warnings to highly targeted “nudge letters.” These letters are no longer generic; they often imply that HMRC already has specific evidence of your rental activity. The moment you receive one of these, your window for an “unprompted” disclosure—which carries the lowest penalties—is effectively closing.

Section 24 and Interest Rates

The full impact of mortgage interest relief restrictions (Section 24) is now felt by all individual landlords. This means your “profit” for tax purposes might be much higher than the actual cash left in your pocket. Combined with higher interest rates on late payments, a tax debt from five years ago is significantly more expensive to settle in 2026 than it was in 2022.

Step-by-Step Guide: How to Disclose in 2026

If you’ve decided to use the Let Property Campaign to fix your tax affairs, follow this professional strategy framework to ensure the best possible outcome.

Step 1: The Notification Phase

You must notify HMRC of your intention to make a disclosure. This “stops the clock” in some regards, as it shows you are willing to cooperate. This is done through the Digital Disclosure Service (DDS).

Step 2: The 90-Day Calculation Window

Once you notify them, you have 90 days to prepare the figures. You will need:

Your other income figures (P60, dividends) to determine your tax bracket.

Step 3: Determining Behavior

You must decide if your error was “Reasonable Care,” “Careless,” or “Deliberate.” This is a legal determination. If you get this wrong, HMRC can reject your disclosure. This is why many landlords in Oxford and Windsor seek professional help to draft their narrative.

Step 4: Submission and Payment

You submit the figures, the interest, and the penalty you’ve calculated. Payment is usually required at the time of submission, though payment plans can be negotiated if you are in financial hardship.

Pros and Cons: Using the Campaign in 2026

Pros

Cons

Lower Penalties: Voluntary (unprompted) disclosures often result in 0% to 20% penalties.

Interest Costs: Statutory interest is mandatory and can be high for old debts.

Asset Protection: Settling now prevents HMRC from placing charges on your property.

Financial Scrutiny: You are essentially opening your “books” to HMRC.

Peace of Mind: No more worrying about the “brown envelope” in the mail.

90-Day Deadline: Once you start, you must finish quickly.

Why You Should Act Now (The “Prompted” Risk)

The biggest risk in 2026 is moving from an unprompted to a prompted disclosure.

Unprompted: You tell them. Penalty for a careless mistake = 0% – 30%.

Prompted: They tell you. Penalty for the same mistake = 15% – 30%.

In high-value rental markets like London, that 15% difference can represent tens of thousands of pounds. HMRC is currently running a massive data-matching exercise focused on the South East, specifically targeting landlords who have not declared income since the 2021/22 tax year.

How Felix & Co. Supports Landlords in Your Area

Navigating the Let Property Campaign requires a blend of tax expertise and a human touch. We don’t just “file papers”; we protect your livelihood.

Windsor & London: We specialize in high-net-worth disclosures where complex tax brackets and multiple properties make the calculations difficult.

Oxford: We help academic and professional landlords who may have moved abroad and inadvertently became “Non-Resident Landlords” without following the correct tax procedures.

Reading & Slough: We provide rapid response services for those who have received nudge letters and need to minimize their prompted penalty rates.

Is it open? Yes, the Let Property Campaign is fully operational in 2026.

Who is it for? Individual landlords (not companies) letting residential property.

What are the benefits? Reduced penalties and avoidance of criminal prosecution.

What is the risk of waiting? HMRC’s “Connect” system is likely to find undeclared income, leading to “prompted” status and higher fines.

How long does it take? 90 days from notification to final submission.

FAQ: People Also Ask

1. Will the Let Property Campaign close soon?

There is no official closing date. However, HMRC can withdraw the “favorable terms” at any time. As their data-matching becomes more perfect, the need for a “voluntary” scheme diminishes, so acting now is safer than waiting for a potential closure.

2. I only have one property. Does HMRC really care?

Yes. HMRC’s system doesn’t differentiate between a landlord with fifty properties and a landlord with one. If the Land Registry shows you own a second home and your tax return doesn’t show rental income, you are a target for a nudge letter.

3. Can I declare income from 10 years ago?

Yes. The Let Property Campaign allows you to go back up to 20 years if the non-disclosure was deliberate. If it was a “reasonable excuse,” you may only need to go back 4 years.

4. What if I can’t afford the tax bill?

HMRC is generally willing to set up a “Time to Pay” arrangement if you are honest and proactive. A specialist accountant can help negotiate these terms so you aren’t forced to sell your property to pay the tax.

5. Are Airbnb and short-term lets included?

Technically, Airbnb hosts can use the Digital Disclosure Service, but the Let Property Campaign is specifically optimized for residential landlords. If you have “Rent a Room” income or short-term lets, you should still disclose, but the rules on expenses may vary.

6. How does HMRC find out about my rental income?

They use “Connect” to scan the Land Registry, the Electoral Roll, bank accounts (for regular large deposits), and data shared by estate agents and local councils (housing benefit payments).

7. Do I need an accountant to do this?

You can do it yourself, but it is high-risk. One mistake in your expense calculation or “behavior” categorization can lead to HMRC rejecting the disclosure and opening a full, intrusive audit.

The Best Time to Act is Now

The Let Property Campaign is still running in 2026, but it is not a “free pass.” It is a window of opportunity that is gradually being crowded by more advanced HMRC surveillance.

For landlords in Slough, Reading, Windsor, and London, the choice is simple: lead the conversation with HMRC on your terms and save thousands in penalties, or wait for them to lead the conversation on their terms. By using this campaign effectively, you can wipe the slate clean, protect your assets, and ensure your property investment remains a source of profit rather than a source of stress.

When landlords realize they have undeclared rental income, the first question they ask is usually: “How many years of back-tax am I going to have to pay?” There is a common misconception that HMRC can only look back at the last few years. In reality, the “statute of limitations” for Tax Look-back is flexible. In 2026, under the Let Property Campaign (LPC), the length of your “look-back” period depends entirely on your behaviour. HMRC categorizes your actions into three buckets: Reasonable Care, Careless, and Deliberate.

At Felix Accountants, we specialize in analyzing your history to ensure you only pay for the years legally required. Here is a breakdown of the 4, 6, and 20-year rules.

1. The 4-Year Rule: “Reasonable Care”

If you can prove that you took reasonable care but still made a mistake, HMRC is limited to looking back only 4 years.

What defines “Reasonable Care”?

HMRC acknowledges that tax is complicated. You might fall into this category if:

You sought advice from a professional that turned out to be incorrect.

You made an honest mathematical error despite keeping good records.

You reasonably believed you didn’t owe tax (e.g., your expenses legitimately wiped out your profit, but you didn’t realize you still had to file a nil return).

The Result: You pay the tax and interest for the last 4 years, and often, you can negotiate a 0% penalty.

The most common category for “accidental landlords” is Careless Behaviour. This applies if you failed to tell HMRC about your rental income because you didn’t check the rules, but you weren’t trying to hide the money.

Examples of Careless Behaviour:

You moved in with a partner and rented your old flat but “forgot” to tell HMRC.

You assumed your letting agent was paying your tax for you.

You didn’t keep proper records and guessed your figures.

The Result: HMRC can go back 6 years. Penalties for an unprompted disclosure in this category typically range from 0% to 30%.

3. The 20-Year Rule: “Deliberate” or “Failure to Notify”

This is the most serious category. If HMRC believes you knew you had a tax obligation and chose to ignore it, or if you failed to notify them that you had started a rental business, they can go back 20 years.

What defines “Deliberate” Behaviour?

You intentionally kept rental income out of your tax returns to pay less tax.

You provided false information to HMRC or concealed records.

You have been a landlord for a decade but never registered for Self Assessment.

The Result: You must disclose every year of income for the last two decades. Penalties for deliberate acts are much higher, ranging from 20% to 100% (and up to 200% if the income involves offshore accounts).

4. The “Offshore” Exception: The 12-Year Rule

In 2026, there is a specific mid-tier rule for landlords who live abroad or have overseas rental property. If an error involves offshore income or gains, and it was “Careless” or even if “Reasonable Care” was taken, HMRC has a standard look-back period of 12 years. The only way to stick to 4 or 6 years in an offshore context is to prove a very specific “reasonable excuse.”

5. How Behaviour Impacts Your Penalty (The “Felix” Strategy)

At Felix Accountants, our job is to act as your advocate. HMRC will often start by assuming a landlord was “Deliberate” to maximize the tax collected. We counter this by:

Evidence-Based Arguments: We present your “Reasonable Excuse” (e.g., serious illness, bereavement, or reliance on a trusted family member) to move you from the 20-year bracket to the 6 or 4-year bracket.

Proactive Disclosure: By using the Let Property Campaign voluntarily, we demonstrate that you are not “concealing” income, which is the strongest defense against the 20-year rule.

Tax Look-back

Behaviour

Assessment Period

Penalty (Unprompted)

Reasonable Care

4 Years

0%

Careless

6 Years

0% – 30%

Deliberate

20 Years

20% – 70%

Deliberate & Concealed

20 Years

30% – 100%

6. Can HMRC Find Me After 20 Years?

Many landlords think, “I’ve been doing this for 15 years and haven’t been caught yet; surely I’m safe?” In the digital age, the answer is no. HMRC’s Connect system has a “long memory.” When you eventually sell the property, the Land Registry data from 20 years ago will be cross-referenced with your tax history. If there’s a 20-year gap where you owned a second property but paid no tax, an investigation is highly likely at the point of sale.

Frequently Asked Questions (FAQs)

Q1: What if my rental business made a loss 5 years ago?

If you made a legitimate tax loss in a specific year (e.g., due to major repairs), that year does not “count” toward your liability, though it still falls within the look-back window. We can often use those losses to offset profits in later years.

Q2: My father died and left me a rental property he never declared. How many years do I pay?

For deceased estates, the rules are slightly different. Usually, HMRC is limited to looking back 6 years prior to the date of death, provided the executors settle the matter promptly.

Q3: Does the 20-year rule apply if I simply didn’t know the law?

HMRC generally argues that “ignorance of the law is no excuse.” However, if we can show you had a “Reasonable Excuse” for not knowing (such as being given bad advice by a previous accountant), we can often fight to keep the period to 6 years.

Q4: If I come forward now, can I choose which years to pay?

No. An LPC disclosure must be “full and complete.” You cannot “cherry-pick” years. If you disclose 5 years but HMRC finds you’ve been a landlord for 15, they will reject your disclosure and open a fraud investigation.

Q5: Will HMRC ask for bank statements from 20 years ago?

If you are in the 20-year bracket and don’t have records, we use “Reasonable Estimations.” We can use historic rental averages and ONS data to recreate your accounts in a way that HMRC will accept.

Know Your Years, Protect Your Future

Determining your “behaviour” is the most technical part of a tax disclosure. Don’t guess and end up paying for 20 years when you only owed 6.

Contact Felix Accountants today. We will review your history and ensure your disclosure is handled with the correct look-back period.

It is January 2026. The world of Small Business Tax has shifted beneath our feet yet again. For years, business owners operated under the looming threat of “sunsets”—the expiration of favorable tax laws. In the United States, the uncertainty regarding the Tax Cuts and Jobs Act (TCJA) kept many entrepreneurs frozen. In the UK, the “Making Tax Digital” (MTD) can was kicked down the road repeatedly.

The 2026 fiscal environment is defined by permanence and digitization. In the US, key small business incentives have been solidified, removing the guesswork but raising the stakes on compliance. In the UK, the digital tax dragnet has finally closed, forcing high-turnover sole traders into quarterly reporting as of this April. Globally, the distinction between “local” and “international” business has vanished, with VAT rules on digital services catching even small freelancers in their net.

This guide is not a collection of “quick tips.” It is a comprehensive operational manual for the small business owner who views taxes not as a bill to be paid, but as a variable cost to be managed. Whether you run a marketing agency in Limbe with UK clients, a university in Cameroon, or a consultancy in London, the principles of tax efficiency remain the same: Defer Income, Accelerate Expenses, Optimize Structure, and Leverage Incentives.

The Foundational Pillars of Tax Efficiency

Before we discuss Section 179 or Dividend Allowances, we must address the unsexy truth: Tax strategy is impossible without data integrity.

The “Audit-Ready” Mindset: Why Documentation is King

In 2026, tax authorities (IRS, HMRC, and others) are using AI-driven enforcement. They do not need to audit you manually to find discrepancies; their algorithms flag “anomalies” in real-time.

The “Receipt” is Dead; The “Evidence” is Alive: A credit card statement line reading “AMZN MKTPLACE” is no longer sufficient. You need the granular invoice showing what was bought. Was it a camera for the business, or a toy for your child?

The “Business Purpose” Memo: Every significant expense in your cloud accounting software must have a memo. “Lunch with Client” is weak. “Lunch with John Doe (Client X) to discuss Q2 Marketing Strategy and contract renewal” is bulletproof.

Separation of Church and State: The Commingling Sin

The single destroyer of tax savings is “commingling”—mixing personal and business funds.

The Corporate Veil: If you run a Limited Company or LLC, commingling funds (paying your home mortgage from the business account) allows courts to “pierce the corporate veil,” rendering you personally liable for business debts.

The Deduction Denial: In an audit, if an inspector finds personal expenses hidden in business accounts, they will often disallow all expenses, forcing you to prove every single transaction from scratch.

You cannot manage 2026 taxes with 2010 tools. Your stack must be integrated:

Bank: A digital-first business bank (Monzo, Starling, Mercury, Relay) that integrates via API.

Ledger: Cloud accounting (Xero, QuickBooks Online, Sage) that pulls bank feeds daily.

Expense Management: A receipt capture tool (Dext, Hubdoc) that OCRs receipts and attaches them to the ledger transaction.

Tax Planner: Software that estimates tax liability monthly, not annually.

United States Tax Strategies (The 2026 “Extension” Reality)

Applicable to US Citizens, US Residents, and US-Connected Businesses.

The fear of the “2025 Cliff” has passed. Recent legislation (often referred to in 2026 circles as the “TCJA Extension” or the “Growth Act”) has solidified the pro-business landscape.

1. The Permanent 20% Pass-Through Deduction (Section 199A)

This is the crown jewel for S-Corps, LLCs, and Sole Proprietors.

The Strategy: You can deduct 20% of your “Qualified Business Income” (QBI) from your taxes. Effectively, you are only taxed on 80% of your earnings.

2026 Update: This provision, which was set to expire at the end of 2025, has been made permanent.

The Trap: High earners (approx. >$190k Single / >$380k Married) in “Specified Service Trades or Businesses” (SSTBs)—like doctors, lawyers, and consultants—face a phase-out.

The Fix: If you are an SSTB near the threshold, aggressive retirement contributions (Solo 401k) can lower your taxable income below the phase-out line, restoring the full 20% deduction.

Small Business Tax S

2. Section 179 & The Return of 100% Bonus Depreciation

The phase-down of Bonus Depreciation (which dropped to 80%, then 60%, then 40% in previous years) has been reversed.

Section 179 (2026 Limits): You can now expense up to $2.5 Million (inflation-adjusted) in equipment. This includes “Off-the-shelf” software, heavy vehicles (over 6,000 lbs), and office furniture.

Bonus Depreciation: 100% Bonus Depreciation is back. This allows you to write off the entire cost of eligible property in year one, even if it creates a Net Operating Loss (NOL).

Strategy: If you have a high-profit year in 2026, purchasing a company vehicle or upgrading your entire IT fleet before December 31st can wipe out significant tax liability.

3. The R&D Pivot: Domestic vs. Foreign Expensing

A major divergence has occurred in how the US treats R&D.

Domestic R&D: If you hire US-based developers or engineers, you can now immediately expense 100% of those costs (a reversal of the painful amortization rules of 2022-2025).

Foreign R&D: If you hire developers outside the US (e.g., in Cameroon or India), you cannot immediately expense those costs. You must amortize (spread) them over 15 years.

Impact: For a US agency hiring offshore talent, your taxable profit might be much higher than your cash profit. You need to plan for this “phantom tax” bill.

4. Estate Tax & The “Sunset” Avoidance

The doubling of the Estate Tax Exemption (approx. $14M+ per person) has been retained. This is critical for business owners with illiquid value (e.g., a valuable brand or software IP). You can gift shares of your business to trusts now without triggering tax, locking in the value outside of your estate.

United Kingdom Tax Strategies (The Digital & Rate Shift)

Applicable to UK Residents and UK Limited Companies.

The UK landscape in 2026 is dominated by the reality of Corporation Tax hikes and Making Tax Digital.

1. Surviving the April 2026 MTD Mandate

The waiting is over. As of April 6, 2026, Making Tax Digital (MTD) for Income Tax is mandatory for sole traders and landlords earning over £50,000.

The Change: You can no longer file a single annual return. You must file quarterly updates via compatible software, plus a Final Declaration.

The Strategy: If you are hovering near £50k turnover, consider incorporating (becoming a Ltd Company). MTD for Corporation Tax is not yet mandated in 2026, giving you an escape route from the quarterly reporting headache of the sole trader regime.

2. Navigating the 25% Corporation Tax Rate

The “small profits rate” of 19% still exists, but the marginal trap is painful.

Profits < £50k: Taxed at 19%.

Profits > £250k: Taxed at 25%.

The Trap (£50k – £250k): Profits in this “Marginal Relief” band are effectively taxed at 26.5%.

The Strategy: If your profit is likely to land in the £50k-£250k band, aggressively accelerate expenses (Pension contributions, equipment purchase) to bring profit down to £50k, or accept the higher rate and focus on growth to push through to £250k where the rate stabilizes at 25%.

3. The “Salary vs. Dividend” Equation in 2026

The classic strategy of “Low Salary + High Dividend” is under pressure due to the slashed Dividend Allowance (now negligible at £500 or less) and higher Dividend Tax rates.

Salary: Take a salary up to the Primary Threshold (approx £12,570) to qualify for State Pension credits without paying National Insurance.

Dividends: Still tax-efficient compared to salary, but the margin is thinner.

The Shift: More directors are moving to Interest Payments. If you lent money to your company (Director’s Loan), charge the company commercial interest. The interest is a deductible expense for the company (saves 19-25% Corp Tax) and is taxed as savings income for you (which has a £1,000 allowance for basic rate taxpayers).

4. Pension Power: The Director’s Ultimate Relief

With the Annual Allowance at £60,000 (check 2026 inflation adjustments), this remains the #1 UK tax shelter.

Employer Contribution: Your company pays £60,000 directly into your SIPP.

The Math: The company saves up to £15,000 (25%) in Corporation Tax. You pay zero Income Tax or National Insurance. It is the only way to extract profit 100% tax-efficiently.

International & Emerging Markets (Global/Cameroon)

For the digital nomad, the agency owner with global clients, or the entrepreneur in emerging markets like Cameroon.

1. Transfer Pricing for Digital Agencies

If you have a Cameroon agency serving UK clients, or a UK Ltd contracting a Cameroon team:

The Risk: Tax authorities want to ensure you aren’t artificially shifting profit to the low-tax jurisdiction.

The Arm’s Length Principle: You must charge a “market rate” for services between your entities. If your Cameroon team does the coding, the UK entity cannot pay them $1. The UK entity must pay a fair market price, leaving a reasonable profit margin in the UK (for sales/marketing) and shifting the bulk of revenue to Cameroon (where production happens).

Cameroon Benefit: Service exports from Cameroon are zero-rated for VAT. This means you don’t charge UK clients VAT, but you can recover input VAT on your Cameroon expenses.

2. VAT on Digital Services (The Global Dragnet)

In 2026, almost every jurisdiction (EU, UK, South Africa, etc.) has “Place of Supply” rules for digital services.

The Rule: If you sell a digital download (e-book, course) to a consumer in France, you owe French VAT, even if you are in Limbe or London.

The Strategy: Use a “Merchant of Record” (like Paddle, Gumroad, or LemonSqueezy). They act as the reseller, handling the global VAT registration and filing for you. The fee they charge (5%) is far cheaper than hiring an accountant to file VAT returns in 27 EU countries.

3. Incentive Zones: The “Economic Disaster” Strategy (Cameroon Specific)

For entrepreneurs in regions like Southwest Cameroon (Limbe), the 2025/2026 Finance Laws offer aggressive incentives to rebuild the economy.

Noseen Zone (Disaster Zone) Benefits: New investments can qualify for massive tax holidays (exemptions from Company Tax for 3-5 years) and tax credits (up to 80% of investment cost).

Education Sector: As a university director, remember that tuition income is VAT exempt, and specialized educational equipment often enjoys custom duty waivers.

Advanced Wealth Extraction

How to get money out of the business efficiently.

1. Hiring Family: The Income Splitting Code

Concept: Shift income from your high tax bracket (40%+) to a family member’s lower bracket (0-20%).

Implementation: Hire your spouse or children for legitimate roles (Social Media Manager, Admin Assistant).

US Benefit: Wages paid to children <18 by a parent-owned Sole Prop are exempt from FICA taxes.

UK Benefit: Utilize the child’s Personal Allowance (tax-free up to ~£12,570).

2. The “Augmented” Home Office Deduction

Renting to Your Business (US – “Augusta Rule”): You can rent your home to your business for up to 14 days a year tax-free. The business gets a deduction for the rental expense (at fair market rates, e.g., for a board meeting or video shoot), and you personally report zero income on your tax return.

Use of Home (UK): Avoid the flat rate (£6/week). Use the actual cost method, apportioning rent, mortgage interest, electricity, and council tax by floor area and usage time.

3. Travel: Bleisure and the “Wholly and Exclusively” Rule

The Strategy: Combine business trips with leisure (“Bleisure”).

The Rule: The primary purpose of the trip must be business.

Execution: Fly to London for a client meeting on Friday. Stay for the weekend. Fly back Monday.

Deductible: Flights (100%), Hotel (Friday night), Meals (Friday).

Non-Deductible: Hotel (Sat/Sun), Personal meals.

Win: You would have paid for the flight anyway; now it is tax-deductible.

Conclusion & Implementation Roadmap

Tax savings in 2026 are not found in secret offshore accounts; they are found in the disciplined execution of the tax code.

Your Q1 2026 Roadmap:

January: File your UK Self Assessment (Deadline Jan 31). Ensure your US W-2s and 1099s are issued.

February: Review your Entity Structure. Are you approaching the £50k MTD threshold? Are you hitting the profit level where an S-Corp election (US) makes sense?

March: US Corporate Tax Deadline (March 15 for S-Corps).

April: UK Tax Year End. MTD Mandate Begins.

Final Thought: The goal is not to pay zero tax. The goal is to pay the legal minimum so you have the capital to reinvest, grow, and secure your financial future.

Frequently Asked Questions (FAQs)

I am a freelancer with clients in the US and UK. Where do I pay tax?

You generally pay tax on your worldwide income in the country where you are “Tax Resident” (usually where you spend 183+ days). However, the US taxes on citizenship, so US citizens must file a US return regardless of where they live. You use “Double Taxation Treaties” to avoid paying twice—claiming a credit in one country for taxes paid in the other.

Is the “Augusta Rule” (tax-free rental of home) applicable in the UK?

No. The Augusta Rule (Section 280A) is a specific US tax code provision. In the UK, renting your home to your business is more complex and can trigger Capital Gains Tax issues on your private residence. Stick to the “Use of Home” allowance in the UK.

Does the 2026 MTD mandate apply to Limited Companies?

Not yet. The April 2026 mandate is for Income Tax (Sole Traders and Landlords). MTD for Corporation Tax is planned for a later date (likely 2028 or beyond). Incorporating is a valid strategy to delay MTD compliance requirements.

Can I deduct my MBA or Master’s degree tuition as a business expense?

US: Yes, if the education maintains or improves skills required in your current trade. It cannot qualify you for a new trade.

UK: Generally No for Sole Traders (it is seen as putting you in a position to trade, not an expense of trading). Yes for Limited Companies if it is relevant to the employee’s role, but it may be a “Benefit in Kind” if not structured correctly.

What is the “Zone Economique” tax credit rate for Cameroon in 2026?

Under the 2025 Finance Law revisions, the tax credit for investments in Economic Disaster Zones (like the Southwest/Limbe) is 80% of the qualifying investment amount. This credit can be carried forward for 5 years. You must obtain certification from the Ministry before claiming.

Welcome to 2026. The days of the “tax inspector” manually reviewing your file with a calculator and a cup of tea are long gone. Today, HMRC compliance and audit risk are defined by one word: Data.

HMRC has evolved into one of the most sophisticated data-mining organizations in the world. Their supercomputer system, “Connect,” cost over £100 million to build and now houses more data on UK citizens than the British Library. It doesn’t just look at your tax return; it looks at your life.

For the business owner in 2026, compliance is no longer about “not getting caught.” It is about “data matching.” If the lifestyle you portray on Instagram doesn’t match the income you declare on your Self Assessment, Connect knows. If your credit card turnover is 20% higher than your declared VAT turnover, Connect knows.

This comprehensive guide is your survival manual. We will dismantle the mechanisms of HMRC’s enforcement, expose the specific triggers for 2026 audits, and provide a rigid framework for protecting your business.

The HMRC “Connect” System – What They Know About You

To manage HMRC compliance and audit risk, you must first understand the adversary. The “Connect” system is the brain of HMRC. It cross-references over 55 billion lines of data to identify “anomalies.”

The Data Dragnet: 30+ Sources You Didn’t Know About

Most taxpayers assume HMRC only sees what is on their P60 or P11D. This is a dangerous misconception. In 2026, Connect pulls data from:

Bank Accounts: Not just interest earned, but direct feeds of turnover and large transactions.

Land Registry: Every property purchase, sale, and transfer is logged. Connect immediately flags if someone declaring £20,000 income buys a £1 million house.

Online Marketplaces: Amazon, eBay, Vinted, and Etsy are legally required to report seller income. The “side hustle” is now fully visible.

Digital Platforms: Airbnb and Booking.com share host income data.

Crypto Exchanges: Coinbase, Binance, and others provide transaction logs to HMRC.

Social Media: Yes, HMRC investigators use web-crawling bots to match public lifestyle posts (luxury holidays, new cars) with reported income.

DVLA: Ownership of high-value vehicles.

Insurance Companies: Insuring a boat or a diamond ring? HMRC knows.

Flight & Passenger Data: Spending 184 days abroad? Connect tracks your residency status automatically.

The AI Algorithms: How “Anomalies” Are Flagged

Connect does not need a human to spot a liar. It uses benchmarking algorithms.

The “Benchmarking” Risk: Connect knows the average profit margin for a “Coffee Shop in South London.” If the average is 15% and you report 3%, you are a statistical outlier. This triggers an automatic “risk score.”

The “Cash Gap”: If your business accepts credit cards, merchant acquirers (Worldpay, Stripe) report your card turnover. Connect estimates your cash turnover based on industry averages. If you declare zero cash, but the industry average is 20%, you get flagged.

HMRC compliance

The 2026 Audit Triggers – Why You Get Selected

Audits (or “Enquiries” as HMRC calls them) are rarely random. In 2026, they are surgical strikes based on risk scores.

The “Red Flags” of 2026

Inconsistent Figures: If your VAT return says turnover was £100,000 but your Corporation Tax return says £80,000, this is an immediate trigger.

Directors’ Loan Accounts (DLA): If your DLA is consistently overdrawn and no Section 455 tax is paid, or if it is “written off” without being declared as income, this is a top priority for 2026.

Large Changes Year-on-Year: If your profit drops by 50% without a clear commercial reason (like a pandemic or recession), it looks suspicious.

Salary Sacrifice Errors: With National Insurance rates high, schemes for electric cars or bicycles are popular. HMRC is aggressively auditing these to ensure they are set up correctly.

Low Tax Liability vs. Lifestyle: The “rich pauper” scenario. If you declare minimal income but live in an expensive postcode, Connect’s “means testing” algorithm will flag you for an Aspect Enquiry.

Sector-Specific Targets in 2026

Construction: The Construction Industry Scheme (CIS) is a perennial target. The focus in 2026 is on “Gross Payment Status” abuse and misclassification of labour-only sub-contractors.

Hospitality & Takeaways: The focus here is Electronic Sales Suppression (ESS). HMRC is looking for “zapper” software used to delete sales from tills.

Agencies (Marketing/Recruitment): The focus is on IR35 (Off-Payroll Working). Are your contractors actually disguised employees?

Making Tax Digital (MTD) – The 2026 Penalty Regime

April 2026 is the watershed moment for Making Tax Digital for Income Tax Self Assessment (MTD ITSA).

The April 2026 Mandate: Who is In?

If you are a sole trader or landlord with a combined gross income (turnover, not profit) of over £50,000, you are mandated to join MTD from April 6, 2026.

Note: The threshold drops to £30,000 in April 2027.

The Points-Based Penalty System

Gone are the immediate £100 fines for being a day late. MTD introduces a “points” system, similar to a driving licence.

The Point: You get 1 point for every missed submission deadline (Quarterly Update).

The Threshold: Once you reach 4 points, you receive a £200 financial penalty.

The Escalation: EVERY subsequent late submission while you are at the threshold triggers another £200 fine.

Resetting: To wipe your points, you must meet a “period of compliance” (usually 12 months of perfect filing).

Digital Record Keeping: The New Legal Standard

The biggest audit risk in MTD is “Digital Links.” You cannot copy-paste figures from a spreadsheet into software. The data must flow digitally (via CSV import or API).

Audit Risk: If HMRC inspects your records and finds you are “typing” totals into Xero rather than importing them, you are non-compliant with the Digital Record Keeping Regulations, carrying a potential penalty of up to £3,000.

HMRC compliance

The R&D Tax Credit Crackdown – The New Battleground

Research & Development (R&D) Tax Credits were once a “free money” bonanza. In 2026, they are HMRC’s #1 fraud target.

The “Anti-Abuse Unit” and Mass Rejections

HMRC now estimates nearly 5-10% of R&D claims are fraudulent or erroneous. In response, they have established a dedicated Anti-Abuse Unit.

The Change: HMRC is no longer “processing now, checking later.” They are freezing payments and launching enquiries before paying out.

The “Technical Uncertainty” Test

The most common reason for audit and rejection in 2026 is the failure to prove “Scientific or Technological Uncertainty.”

The Trap: Using an off-the-shelf software plugin to build a website is not R&D.

The Requirement: You must prove you attempted to resolve a technological problem that a “competent professional” in the field could not easily solve.

Why Advertising Agencies are Under Fire

In late 2025 and early 2026, HMRC issued “Nudge Letters” specifically to the Advertising and Marketing sector.

Why? Many agencies claimed R&D for building standard websites, CRMs, or data analytics dashboards. HMRC views this as “commercial application of existing technology,” not R&D. If you are an agency owner, audit your past claims immediately.

“Nudge” Letters – The Psychological Warfare

HMRC has a dedicated “Behavioural Insights Team.” They know that a terrifying legal letter is less effective than a “helpful” nudge that makes you question your own honesty.

Interpreting the “One-to-Many” Letter

These are letters sent to thousands of taxpayers at once based on broad data matching.

The Tone: “We have information that suggests you may have X… please check your return.”

The Trap: They don’t tell you what they know. They want you to panic and disclose everything.

Common Nudges in 2026

Crypto Assets: “We have received data from crypto exchanges.” (Reminding you that crypto to fiat trades are taxable events).

Offshore Income: “You may have income from overseas.” (Triggered by the Common Reporting Standard data sharing).

Directors’ Loans: “Your accounts show a loan written off.” (Reminding you this is taxable as a dividend/earnings).

To Respond or Not to Respond?

Do: Review your affairs immediately.

Don’t: Ignore it. If you ignore a nudge letter and HMRC later opens an enquiry, they will view your error as “Deliberate” rather than “Careless,” doubling the penalties.

Handling an Audit – A Tactical Playbook

You receive a brown envelope. It’s an “Opening Letter” for a Check of Self Assessment. What do you do?

1. The “Golden Rule” of Communication

Never speak to HMRC directly. HMRC officers are trained to gather information. A casual chat about your “weekend in Spain” can be used to prove you have a holiday home you didn’t declare.

Action: Appoint a professional tax advisor immediately. All correspondence goes through them.

2. The Schedule 36 Information Notice

HMRC will send a list of documents they want (Bank statements, invoices, emails).

Tactical Check: Is the request “Reasonably Required”? Often, HMRC asks for personal bank statements or spousal data they have no legal right to see. Your accountant should challenge excessive requests.

3. Negotiating Penalties: “Suspended” vs. “Careless”

If you made a mistake, the game is about Penalty Mitigation.

Careless: You tried but failed (0-30% penalty).

Deliberate: You knew and did it anyway (20-70% penalty).

Deliberate & Concealed: You tried to hide it (30-100% penalty).

The Goal: Argue for “Careless” and ask for a Suspended Penalty. This means if you stay compliant for 2 years, the fine is wiped out.

HMRC compliance

Conclusion & The Compliance Checklist

HMRC compliance and audit risk in 2026 is manageable, but it requires a proactive, digital-first approach. You cannot hide in the shadows; the Connect system casts too much light.

Your 2026 Survival Checklist:

Digital Health Check: Are your bank feeds integrated? Are receipts scanned?

R&D Audit: If you claimed R&D, do you have a technical report written by a competent professional?

DLA Review: Is your Director’s Loan Account in credit? If overdrawn, has S455 tax been paid?

Turnover Watch: Are you approaching the £50k MTD threshold?

Insurance: Do you have “Tax Investigation Insurance”? (This pays your accountant’s fees if you get investigated – highly recommended).

Frequently Asked Questions (FAQs)

What triggers an HMRC investigation most frequently in 2026?

The most common trigger is a data mismatch in the Connect System. If your declared income doesn’t match the lifestyle data (property, cars) or financial data (bank interest, card turnover) HMRC holds, an enquiry is automatic. Additionally, the Construction and R&D sectors are under “campaign” scrutiny.

Can HMRC look at my personal bank account?

Not automatically. During a standard enquiry, they can only request business records. However, if they suspect “broken records” (i.e., they can prove your business books are unreliable), they can issue a “Schedule 36 Notice” to demand personal statements to verify your means.

What are the penalties for R&D tax credit fraud?

They are severe. Beyond repaying the credit with interest, penalties can range from 30% to 100% of the tax due. In cases of deliberate fraud, HMRC is increasingly pursuing criminal prosecution and naming/shaming directors, which disqualifies them from running companies in the future.

Do I really need to keep digital receipts for MTD?

Yes. Under the Digital Record Keeping rules, you must store a digital copy of the receipt. A shoebox of paper receipts is no longer compliant. You don’t need to keep the paper original once it is scanned, but the digital copy must be legible and retrievable.

How far back can HMRC investigate?

Normal Enquiry: 12 months after the filing deadline.

Careless Error: Up to 6 years.

Deliberate Error (Fraud): Up to 20 years.

Note: If they find a deliberate error in one year, they will almost always open the previous 20 years.

The Era of “Continuous Compliance” Self-Assessment

2026 marks a pivotal shift in the global regulatory landscape. We have moved past the era where “compliance” was a once-a-year box-ticking exercise. From the tax offices in the UK to the defense corridors of the Pentagon, regulators are demanding more data, faster reporting, and higher standards of verification.

For business owners, Finance Directors, and IT leaders, 2026 is the year of enforcement. The grace periods of the post-pandemic years have evaporated. The UK’s HMRC is aggressively closing the gap on digital tax reporting; the US Department of Defense (DoD) is actively enforcing cybersecurity standards in contracts; and the IRS has solidified its reporting windows for healthcare coverage.

This comprehensive guide serves as your operational manual for 2026. It dissects the four most critical self-assessment frameworks impacting businesses today:

If you are a UK-based business owner, a sole trader, or a high-net-worth individual, the immediate priority in January 2026 is the 2024/25 tax year filing.

1 The Critical Deadlines for 2026

The UK tax year runs from April 6 to April 5. The self-assessment cycle currently concluding covers the tax year 6 April 2024 to 5 April 2025.

31 October 2025 (Paper Deadline): PASSED. If you intended to file a paper return, this deadline has already passed. You must now file online to avoid penalties.

31 January 2026 (Online Deadline): This is the hard deadline for filing your electronic tax return. The system closes at midnight.

31 January 2026 (Payment Deadline): Crucially, this is also the deadline to pay:

Any “balancing payment” owed for the 2024/25 tax year.

The first Payment on Account for the 2025/26 tax year (usually 50% of your previous year’s tax bill).

2 The Penalty Regime: Why “A Few Days Late” Costs More Than You Think

HMRC operates an automated penalty system. There is no human reviewing your file to see if you had a busy week; the computer simply issues the fine.

The Instant Fine: If your return is not received by 11:59 PM on January 31, you receive an automatic £100 penalty. This applies even if you have zero tax to pay or if you have already paid the tax.

3 Months Late: Daily penalties of £10 per day begin, up to a maximum of £900 (90 days).

6 Months Late: A further penalty of 5% of the tax due or £300, whichever is greater.

12 Months Late: Another 5% or £300 charge. In cases of deliberate concealment, this can rise to 100% of the tax due.

3 The “Making Tax Digital” (MTD) Shadow

While you rush to file the 2024/25 return, you must recognize that this is the final “traditional” filing year for many.

April 6, 2026 marks the start of MTD for Income Tax for sole traders and landlords with income over £50,000.

Implication: If your 2024/25 return (the one you are filing now) shows turnover above £50,000, you are legally mandated to start using MTD-compatible software from April 2026.

Action: Do not just file your return; audit your turnover. If you breach the threshold, you have less than 90 days to procure software like Xero, QuickBooks, or Sage.

Self-Assessment

US Healthcare Compliance – The Affordable Care Act (ACA)

For US employers, specifically “Applicable Large Employers” (ALEs) with 50+ full-time equivalent employees, the ACA reporting window is a critical Q1 obligation.

1 The “Permanent Extension” Schedule

Historically, the deadline to furnish forms to employees was January 31st. However, the IRS has instated a permanent automatic extension for this specific deadline, shifting the compliance rhythm for 2026.

Deadlines for 2025 Reporting (Due in 2026):

Furnish Forms to Employees (Form 1095-C):

Deadline:March 2, 2026

Requirement: You must provide every eligible full-time employee with a copy of Form 1095-C. This form proves they had health insurance offer coverage (Code 1A, 1E, etc.) and helps them file their own taxes.

Strategy: While you have until March 2, it is best practice to issue these alongside W-2s in late January to reduce employee confusion.

File with the IRS (Electronic):

Deadline:March 31, 2026

Requirement: You must transmit Form 1094-C (the transmittal “cover sheet”) and all copies of Form 1095-C to the IRS AIR system.

Threshold Change: The e-filing threshold is now 10 returns. If you have 10 or more information returns (W-2s + 1095s combined), you must file electronically. Paper filing is effectively dead for ALEs.

2 Common Pitfalls for 2026

The “Controlled Group” Trap: If you own multiple companies (e.g., a staffing firm and a software company), the IRS aggregates their employees to see if you hit the 50-employee ALE threshold. You cannot split your workforce into three smaller companies to avoid ACA reporting.

Code 1A vs. 1E: Misclassifying an offer of coverage on Line 14 of the 1095-C is the most common trigger for IRS Penalty Letter 226J. Ensure your HR software is correctly coding “Qualifying Offers.”

The New Frontier – CMMC 2.0 (US Defense Contracts)

If you are a contractor, subcontractor, or supplier to the US Department of Defense (DoD), 2026 is the year the Cybersecurity Maturity Model Certification (CMMC) becomes real.

1 The 2026 Status: Phase 1 Rollout

As of January 2026, we are deep into Phase 1 of the CMMC rollout.

Requirement: Self-Assessments are now mandatory for all relevant contracts.

Contract Clauses: You will start seeing CMMC requirements appear in Requests for Information (RFIs) and Requests for Proposals (RFPs).

2 Your Obligations by Level

The CMMC model has three levels. Most small businesses (SMBs) in the supply chain fall into Level 1 or Level 2.

Level 1 (Foundational):

Who: Contractors handling Federal Contract Information (FCI). (e.g., simple emails from the government, non-sensitive contract details).

Action: You must perform an annual Self-Assessment against 17 basic security controls (passwords, antivirus, door locks).

Submission: You must sign a document by a senior official affirming compliance and upload your score to the Supplier Performance Risk System (SPRS).

Deadline:Immediate. You cannot be awarded a new contract without this score in the system.

Action: Implementation of 110 controls from NIST SP 800-171.

2026 Shift: While some contracts still allow Self-Assessment for Level 2, the DoD is moving toward requiring Third-Party Assessments (C3PAO). In 2026, you should be preparing for a third-party audit.

Q1 2026 Milestone: DoD contracts starting in 2026 will increasingly verify your SPRS score before award. If you have a negative score (meaning you have open Plan of Action & Milestones, or POAMs), you may be deemed ineligible.

3 The False Claims Act Risk

Self-Assessment

The Department of Justice has launched a “Civil Cyber-Fraud Initiative.” If you submit a Self-Assessment claiming you have 2-factor authentication when you actually don’t, this is considered fraud. Whistleblowers (e.g., your own disgruntled IT employees) can report you and receive a percentage of the fine. Do not falsify your self-assessment.

Payment Security – PCI DSS v4.0

The Payment Card Industry Data Security Standard (PCI DSS) regulates anyone who accepts credit cards (Visa, MasterCard, Amex).

1 The “Future-Dated” Requirements Are Now Active

PCI DSS v4.0 was released years ago, but it contained roughly 50 “future-dated” requirements that gave businesses until March 31, 2025 to implement.

By January 2026, these are fully mandatory. If you are still relying on PCI DSS v3.2.1 habits, you are non-compliant.

2 Key v4.0 Changes You Must Audit Now

Multi-Factor Authentication (MFA): Previously, MFA was mostly for remote access. Under v4.0, MFA is generally required for all access to the Cardholder Data Environment (CDE), even if you are sitting inside the office.

Anti-Phishing Mechanisms: You must have technical controls (like DMARC, SPF, and DKIM) to prevent your domain from being used for phishing, and you must train personnel on phishing awareness.

e-Commerce Skimming Protection: If you have a website payment page, you must have a script monitoring solution that alerts you if unauthorized code (like a digital skimmer or “Magecart” attack) is added to your payment page.

3 The Self-Assessment Questionnaire (SAQ)

Most small merchants do not need a full audit; they complete an SAQ.

Deadline: Determined by your merchant bank (Acquirer). Usually, it is the anniversary of when you first opened your account.

Action: Check your merchant portal (e.g., Worldpay, Stripe, Square dashboard). If your PCI status says “Non-Compliant,” you are likely paying a monthly “Non-Compliance Fee” of $20-$50. Completing the SAQ removes this fee immediately.

Strategic Compliance Management

Managing these disparate deadlines requires a centralized approach. You cannot rely on sticky notes.

CMMC Self-Assessment (Upload to SPRS prior to contract award)

2 The “Self-Assessment” Mindset

Whether it is tax or cybersecurity, the regulator is shifting the burden of proof to you.

Tax: You must prove your expenses are legitimate.

Cyber: You must prove your firewall is active.

Data: You must prove you offered health insurance.

Best Practice: Adopt an “Audit-Ready” posture. Do not prepare documents for the deadline. Maintain a “Compliance Folder” (digital secure vault) where evidence (receipts, log files, insurance certificates) is dropped monthly. When the deadline arrives, the work is simply packaging, not creating.

Self-Assessment

Frequently Asked Questions (FAQs)

I am a UK Director living abroad. Do I still need to file by Jan 31?

Yes. Residency status does not change the filing deadline. If you have UK-sourced income (like rental property or dividends), you must file your Self Assessment by January 31, 2026. However, non-residents cannot use the standard HMRC online software; you must use “commercial software” or file by paper (which deadline has passed). You should seek a specialist accountant immediately to file via commercial software to avoid penalties.

I missed the CMMC Level 1 self-assessment. Can I still bid on a DoD contract?

Generally, no. Contracting Officers are instructed to check the SPRS database before making an award. If your score is missing or is too old (older than 3 years), you are ineligible. You can perform the assessment and upload the score today; it usually takes 24-48 hours to reflect in the system.

Does the ACA reporting requirement apply if I have 48 full-time employees and 10 part-time ones?

Likely yes. The ACA uses “Full-Time Equivalents” (FTE). You must aggregate the hours of your part-time staff. If their combined hours equal 2 full-time workers, you have 50 FTEs (48 + 2). You would be an Applicable Large Employer (ALE) and must report.

Can I just pay the £100 HMRC fine and file later?

You can, but it is dangerous. The £100 is just the “entry fee.” The daily penalties (£10/day) kick in after 3 months. More importantly, late filing keeps the “enquiry window” open longer, meaning HMRC has more time to investigate your affairs. Filing late raises a “risk flag” on your account profile.

What is the difference between PCI DSS compliance and certification?

“Certification” usually implies an external audit by a QSA (Qualified Security Assessor) resulting in a Report on Compliance (ROC). This is for huge merchants (Level 1). “Compliance” for small merchants usually just means truthful completion of the Self-Assessment Questionnaire (SAQ). Both are legally binding. You don’t need a “certificate” on the wall, but you need a valid SAQ on file.

If you ask the average small business owner what their largest single expense is, they might guess payroll, inventory costs, or perhaps commercial rent. They would almost certainly be wrong. Over the lifetime of a successful small business, the single largest expense is taxation.

Taxes are a relentless financial current, eroding profit margins not just once a year, but with every transaction, every hire, and every sale. Yet, ironically, it is the expense that business owners spend the least amount of strategic energy managing. Most view taxes through a lens of compliance and fear—a bureaucratic hurdle to be cleared once a year to avoid penalties.

This mindset is expensive.

Treating taxes solely as a compliance issue is akin to ignoring your supply chain costs until the end of the year and just paying whatever invoice arrives. Successful entrepreneurs understand that taxes are a variable cost. Like any variable cost, they can be managed, reduced, and optimized through proactive strategy.

The difference between a struggling business and a thriving one often comes down to cash flow. And there is no faster way to improve cash flow than by legally reducing your tax liability. Every dollar saved in taxes is a dollar that can be reinvested into marketing, used to hire better talent, spent on upgrading equipment, or simply taken home as reward for the immense risk of entrepreneurship.

The Scope of This Guide