The landscape of UK buy-to-let has reached a “Big Bang” moment. With the Section 21 abolition officially taking effect as part of the Renters’ Rights Act 2025, the days of “no-fault” evictions are over. For landlords, this isn’t just a shift in tenancy management; it is a fundamental shift in tax compliance.

As the Let Property Campaign, I am here to guide you through this transition. The new legislation links your right to regain possession of your property directly to your status on the National Landlord Database, which functions as a direct data pipeline to HMRC. If you have undisclosed rental income, the window to “come clean” under favorable terms is closing fast.

The Death of Section 21 and the Rise of the Periodic Tenancy

On 1 May 2026, the Renters’ Rights Act 2025 fully takes effect, mandating the total abolition of Section 21 “no-fault” evictions. Furthermore, all tenancies are being converted into “periodic” or rolling agreements.

The National Landlord Database “Trap”

To serve a valid possession notice under these new rules—even for legitimate reasons like selling the property or moving back in—landlords must be registered on the new National Landlord Database.

The Data Link: This database is not just an administrative list; it is a direct data feed to HMRC.

The End of Ghost Landlording: It is now virtually impossible to legally manage a property or evict a tenant without your details being cross-referenced against HMRC’s “Connect” system.

Bridging the Gap: The Let Property Campaign

If the Section 21 abolition has made you realize that your tax affairs aren’t quite in order, the Let Property Campaign is your best route to compliance.

What is the Let Property Campaign?

It is a specific opportunity for individual landlords to disclose unpaid taxes on residential properties. By coming forward voluntarily, you secure more favorable terms—including lower penalties—than if HMRC finds you first through their new digital data pipelines.

Eligibility Criteria

You can use this campaign if you are an individual landlord (not a company or trust) renting out:

Single or multiple residential properties.

A room in your main home that exceeds the Rent a Room Scheme threshold.

Holiday lets or inherited properties.

UK property while living abroad.

The 3-Step Disclosure Roadmap

Step

Action

Key Deadline

1. Notify

Tell HMRC you intend to make a disclosure.

Immediately upon realizing the error.

2. Calculate

Work out tax, interest, and penalties for the relevant years.

90 days from notification.

3. Pay

Make a formal offer and pay the full amount electronically.

90 days from notification.

How Far Back Do You Need to Go?

The number of years you must disclose depends on why the tax wasn’t paid:

Reasonable Care: Maximum of 4 years.

Careless (Not taking reasonable care): Maximum of 6 years.

Deliberate: Up to 20 years.

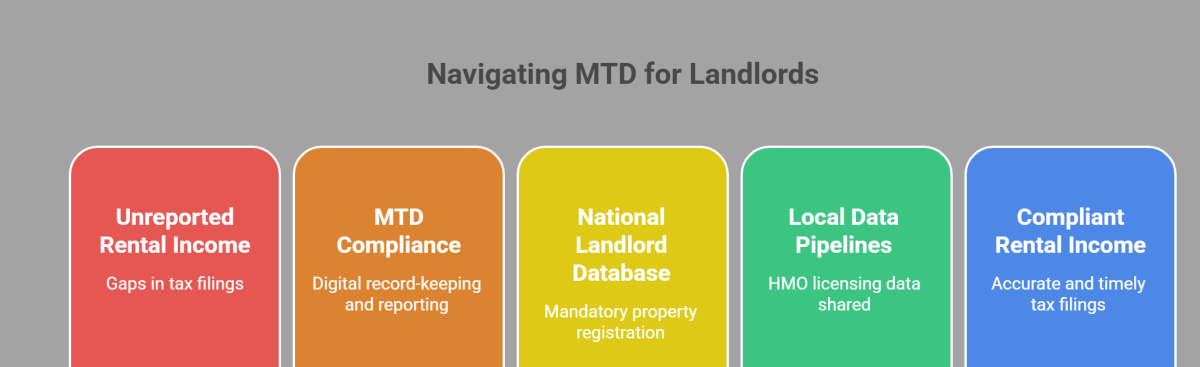

2026: The Year of Digital Enforcement

The Section 21 abolition is just one piece of a larger enforcement puzzle.

Making Tax Digital (MTD)

Since 6 April 2026, MTD for Income Tax has been mandatory for landlords earning over £50,000. This requires quarterly digital reporting, meaning HMRC sees your financial data every three months rather than once a year.

Local Council Data Pipelines

Regional enforcement is also tightening. For example, Reading Borough Council now shares HMO licensing data directly with HMRC’s “Connect” system. Automated pipelines verify landlord identities and property details, leaving no room for “accidental” omissions.

Why Voluntary Disclosure is Non-Negotiable

If HMRC discovers your undisclosed income before you notify them, the consequences are severe:

Higher Penalties: Up to 100% for UK income or 200% for offshore income.

Criminal Risk: Potential for criminal prosecution and being named on the “deliberate defaulters” list.

By contrast, voluntary disclosure through specialists like Marslands Accountants can significantly reduce the burden. Marslands report helping landlords save an average of £7,000 on their final tax bill through the expert application of allowable expenses.

Frequently Asked Questions Section 21 abolition

1. What is the impact of the Section 21 abolition on current landlords?

The Section 21 abolition means you can no longer use “no-fault” notices to end tenancies. To gain possession, you must use specific grounds (like selling or moving in) and be registered on the National Landlord Database. This registration acts as a trigger for HMRC to verify your tax compliance and rental income history.

2. Can I still evict a tenant after the Section 21 abolition?

Yes, but the process is now more rigorous. You must provide a valid reason under the revised grounds for possession. Crucially, your legal standing to evict is tied to your transparency; if you aren’t registered on the National Landlord Database—which feeds into HMRC—your possession notices will likely be deemed invalid by the courts.

3. How does the National Landlord Database link to my taxes?

The database is a digital pipeline that shares your property and identity details directly with HMRC’s Connect system. Once you register to comply with the Section 21 abolition requirements, HMRC can automatically cross-reference your property holdings against your self-assessment filings to identify any gaps in reported rental income or capital gains.

4. What should I do if I haven’t declared rental income before 2026?

You should immediately notify HMRC via the Let Property Campaign. With the Section 21 abolition making “ghost landlording” impossible, a voluntary disclosure is the only way to avoid the maximum 100–200% penalties. Starting the process now allows you to settle unpaid taxes under the campaign’s more lenient voluntary terms.

5. How many years of back-tax will HMRC look at?

If you have been “careless,” HMRC typically goes back 6 years. However, if they deem the omission “deliberate”—which is easier to prove now with the Section 21 abolition and MTD providing digital trails—they can go back 20 years. Voluntary disclosure often helps limit the scope and penalty percentage compared to an HMRC-led inquiry.

6. What expenses are allowable in a Let Property Campaign disclosure?

You can deduct “wholly and exclusively” incurred costs such as repairs, insurance, and management fees. Expert accountants, like Marslands, often help landlords save an average of £7,000 by identifying overlooked allowable expenses. Ensuring these are calculated correctly is vital now that MTD requires quarterly digital transparency for many landlords.

7. Is the Let Property Campaign available for limited companies?

No, the campaign is strictly for individual landlords. If you operate your properties through a limited company and have undisclosed income, you cannot use these specific terms. However, with the Section 21 abolition affecting all residential tenancies, companies must also ensure their digital records match the National Landlord Database to remain compliant.

8. What happens if I ignore the new tax transparency rules?

Ignoring the rules while the Section 21 abolition is in effect is highly risky. HMRC’s “Connect” system now receives data from local councils, the National Landlord Database, and MTD. Failure to disclose can lead to penalties of up to 100%, public naming as a defaulter, and the loss of your legal right to manage or regain your property.

The April 2026 MTD deadline has arrived, marking the most significant shift in property taxation in a generation. For landlords in Reading and across the UK, the transition from annual Self Assessment to quarterly digital reporting is no longer a future concept—it is a mandatory legal requirement for those with qualifying income over £50,000.

As the Let Property Campaign, I am here to ensure you navigate this “Big Bang” moment without falling into the digital traps set by automated enforcement. If the sudden transparency of Making Tax Digital (MTD) has highlighted gaps in your previous filings, the Let Property Campaign remains your primary safety net for voluntary disclosure.

The 2026 Enforcement Trifecta

The April 2026 MTD rollout does not exist in a vacuum. It is part of a three-pronged enforcement strategy designed to eliminate “ghost landlording.”

MTD for Income Tax (Active 6 April 2026): Mandatory digital record-keeping and quarterly updates for landlords earning over £50,000.

National Landlord Database (Active 1 May 2026): Under the Renters’ Rights Act 2025, registration is mandatory to legally manage properties or serve possession notices.

Local Data Pipelines (Reading): Since 1 March 2026, Reading Borough Council has extended licensing to small HMOs (3-4 occupants), sharing this data directly with HMRC’s “Connect” system.

Understanding Qualifying Income for the April 2026 MTD Deadline

A common misconception is that the £50,000 threshold applies to profit. It does not. The April 2026 MTD rules apply to your gross qualifying income—the total rent received before any expenses are deducted.

Income Type

Included in Threshold?

Gross Rental Income (UK & Overseas)

Yes

Self-Employment Income

Yes

Furnished Holiday Lets

Yes

Jointly Owned Property Share

Individual Share Only

The Reading “Trap”: Additional Licensing Meets HMRC Connect

Landlords in Reading face a unique challenge. On 1 March 2026, the council’s Additional HMO Licensing scheme became active for properties with 3 or 4 occupants.

This is more than a safety check. This licensing data serves as a direct feed to HMRC. If you apply for a license in Reading but have not declared that rental income for previous years, the April 2026 MTD digital trail will likely trigger an automated tax enquiry.

Voluntary Disclosure via the Let Property Campaign

If the new digital landscape has made you realize your past filings were “careless” or incomplete, the Let Property Campaign allows you to “come clean” under favorable terms.

Reasonable Care: HMRC may only look back 4 years.

Careless: HMRC can investigate the last 6 years.

Deliberate: Up to 20 years of back-tax, interest, and penalties.

By notifying HMRC voluntarily, you avoid the maximum 100-200% penalties associated with prompted enquiries. Specialists like Marslands Accountants report saving landlords an average of £7,000 on their final bill by identifying valid allowable expenses that landlords often overlook.

Frequently Asked Questions

1. What is the impact of the Section 21 abolition on current landlords?

The Section 21 abolition, effective 1 May 2026, removes the ability to end tenancies without a specific reason. To regain possession, landlords must use new grounds and be registered on the National Landlord Database. This registration links directly to the April 2026 MTD framework, ensuring total tax transparency before any legal possession can be granted by the courts.

2. Can I still evict a tenant after the Section 21 abolition?

Yes, but you must use Section 8 grounds, such as the new Ground 1A for selling the property. However, your legal standing is now tied to compliance. If you are not registered on the National Landlord Database—which feeds into the April 2026 MTD data net—your eviction notices will likely be ruled invalid.

3. How does the National Landlord Database link to my taxes?

The database acts as a digital pipeline to HMRC’s “Connect” system. When you register to comply with the Renters’ Rights Act, HMRC cross-references your identity against your April 2026 MTD submissions. Any discrepancy between the properties you claim to manage and the income you report will trigger an immediate compliance check.

4. What should I do if I haven’t declared rental income before 2026?

You should immediately notify HMRC through the Let Property Campaign. With the April 2026 MTD deadline now active, “ghost landlording” is no longer viable. Making a voluntary disclosure before HMRC’s automated systems flag your Reading licensing data can significantly reduce your penalties and the risk of criminal prosecution.

5. How many years of back-tax will HMRC look at?

The look-back period depends on your behavior. If you were “careless,” HMRC typically reviews 6 years. If they deem the omission “deliberate”—a conclusion easier to reach given the April 2026 MTD digital requirements—they can go back 20 years. Voluntary disclosure is the best way to limit this window and secure lower penalty rates.

6. What expenses are allowable in a Let Property Campaign disclosure?

You can deduct “wholly and exclusively” incurred costs, such as property repairs, insurance, and management fees. In the context of the April 2026 MTD shift, keeping digital receipts for these expenses is vital. Specialists like Marslands often help landlords identify overlooked deductions, saving an average of £7,000 on their final settlement.

7. Is the Let Property Campaign available for limited companies?

No, the campaign is strictly for individual landlords. While companies are not eligible for these specific voluntary terms, they are still subject to the transparency brought by the April 2026 MTD era and the National Landlord Database. Companies with undisclosed income should seek professional advice to rectify their position outside of this specific campaign.

8. What happens if I ignore the new tax transparency rules?

Ignoring the April 2026 MTD and licensing rules is high-risk. HMRC’s “Connect” system now synthesizes data from MTD, the National Landlord Database, and Reading’s HMO licensing. Failure to comply can result in penalties up to 100% of the tax due, being named a “deliberate defaulter,” and losing the legal right to manage or evict tenants.

Note: For more information on making a disclosure, visit the official GOV.UK guide or contact felixaccountants for specialist support.

HMRC isn’t guessing anymore. Between the Land Registry, bank data, and even sites like Airbnb or Zoopla, the tax office has a digital map of who owns what and who’s likely collecting rent without telling them. If you own rental property in London, Slough, or the surrounding Thames Valley and haven’t fully disclosed your income, you’re sitting on a ticking financial clock and need to contact a Let Property Campaign Expert immediately. The Let Property Campaign is your one-way escape hatch, but navigating it alone is a recipe for overpaying or, worse, triggering a full-scale forensic audit.

Don’t wait for the letter to arrive. If you have undisclosed rental income in London, Slough, Windsor, Reading, or Oxford, taking the first step today is the only way to stay in control of your finances.

You’re about to learn exactly how the disclosure process works, why local market nuances in places like Windsor and Oxford matter to your tax bill, and how an expert ensures you pay the absolute legal minimum in penalties and interest.

What is a Let Property Campaign Expert?

A Let Property Campaign expert is a specialist tax advisor who manages the voluntary disclosure of undeclared rental income to HMRC. They calculate exact tax liabilities, identify all allowable property expenses to reduce the bill, and negotiate the lowest possible penalty percentages based on the landlord’s specific circumstances and “quality of disclosure.”

The Reality of HMRC Surveillance in the M4 Corridor

HMRC’s “Connect” system is an AI-driven database that cross-references billions of data points. For a landlord in Reading or London, this means HMRC knows when a property title changes, when a deposit is protected, and when a tenant claims housing benefits at your address.

The Let Property Campaign (LPC) is a specific opportunity for landlords who have failed to disclose their rental income to come forward. It’s not a “get out of jail free” card, but it is a “stay out of court” card. If you come to them before they send you a “nudge letter,” the penalties are significantly lower. If you wait until they find you, those penalties can reach 100% of the tax owed—or lead to criminal prosecution.

Why Location Matters: From Oxford Students to Slough Corporates

Your tax disclosure isn’t just about spreadsheets; it’s about the reality of your rental market. HMRC’s benchmarks for “reasonable” rental income vary wildly across the South East.

Oxford and Windsor: High-value areas with complex HMO (House in Multiple Occupation) setups or short-term holiday lets. These often involve higher management costs and maintenance fees that many landlords forget to deduct.

London and Slough: High churn rates and corporate lets. If you’ve had periods of vacancy or spent heavily on “repair vs. improvement” (a massive distinction in tax law), an expert ensures these are categorized to your advantage.

Reading: An area with high professional rental demand where landlords often move from a primary residence to a “buy-to-let” without realizing the CGT (Capital Gains Tax) implications of their future plans.

An expert understands that a £2,000 monthly rent in Slough looks different on a balance sheet than £5,000 in Kensington. They use local market data to justify your figures if HMRC questions the “commerciality” of your arrangements.

The Danger of the “DIY” in Let Property campaign Disclosure

Many landlords think the Let Property Campaign is as simple as filling out a form and cutting a check. It’s not. The biggest risk isn’t the tax itself; it’s the interest and the penalty classification.

HMRC classifies your “failure to notify” into three buckets:

Reasonable Excuse: You had a genuine reason (illness, bereavement) for not filing.

Careless: You didn’t take enough care to get it right.

Deliberate: You knew you owed tax and chose not to pay.

A DIY filer might accidentally admit to “deliberate” behavior through poor phrasing, or fail to argue for a “reasonable excuse.” An expert acts as a shield, framing your history in the most favorable light supported by evidence. They also ensure you aren’t paying tax on “capital” items that should actually be deducted from your future Capital Gains bill rather than your current Income Tax bill.

Step-by-Step: How an Expert Navigates Your Let Property campaign

Disclosure

1. The Portfolio Audit

Before speaking to HMRC, your advisor will reconstruct your financial history. This involves gathering bank statements, letting agent statements, and receipts for every tap fixed or wall painted over the last several years. They don’t just look for income; they hunt for “missing” expenses like mortgage interest (subject to Section 24 restrictions), insurance, and service charges.

2. The Notification Phase

Once the figures are ready, your expert notifies HMRC of your intent to disclose. This creates a “standstill” period of 90 days. During this time, you are protected from certain enforcement actions while the final report is prepared.

3. Technical Calculations

Calculating the tax is the easy part. The hard part is calculating the Section 24 interest relief and the tapered penalties. Since 2017, mortgage interest isn’t a direct deduction from rental income for individual landlords; it’s a 20% tax credit. Many DIY landlords still try to deduct the full interest, which is an immediate red flag for HMRC.

4. The Disclosure Submission

The final report is sent via the Official Government Gateway. This isn’t just a number; it’s a narrative. An expert includes a “disclosure letter” explaining why the omission happened, which is vital for minimizing penalties.

5. Payment and Settlement

Your expert helps arrange payment. If you can’t pay the full amount (which often happens when multiple years of back-tax are due), they negotiate a “Time to Pay” arrangement, allowing you to spread the cost without HMRC freezing your assets.

Comparison: Expert Disclosure vs. HMRC Discovery

Feature

Expert-Led Disclosure

HMRC Discovery (Audit)

Penalty Rate

Often 0% – 20%

35% – 100%+

Look-back Period

Limited by “reasonable care”

Up to 20 years

Control

You lead the narrative

HMRC dictates the investigation

Stress Level

Managed by professionals

High (legal/criminal threats)

Cost

Fixed fee + lower tax

Higher tax + compound interest + huge penalties

The “Repair vs. Improvement” Trap

This is where most London and Windsor landlords lose money. If you replace a broken wooden window with a double-glazed uPVC window, HMRC usually views that as a “repair” (deductible from income tax). If you build an extension or install a high-end designer kitchen where a basic one existed, that’s an “improvement” (deductible from Capital Gains Tax when you sell).

Without an HMRC Let Property Campaign expert in Slough or London, you might try to claim an extension against your rental income. HMRC will reject it, charge you a penalty for a “careless” error, and you’ll still owe the tax. An expert knows how to categorize these costs to maximize your current cash flow while protecting your future tax position.

Is it too late if I already received a Let Property campaign letter?

If you’ve received a “nudge letter” from HMRC mentioning the Let Property Campaign, the window for a “voluntary” disclosure is closing, but it isn’t shut. You can still use the campaign, but your penalty will likely be higher than if you had come forward unprompted. However, responding with a professional report from a London tax specialist shows HMRC that you are now taking your obligations seriously. This often prevents them from digging into other areas of your finances, like your primary business or offshore investments.

Strategy Framework: The Felix Approach to Let Property campaign

We don’t just crunch numbers. We look at the “Three Pillars of Protection”:

Documentation: Creating a “bulletproof” trail of expenses to offset income.

Mitigation: Arguing for the lowest possible penalty tier based on your life circumstances.

Future-Proofing: Setting up your digital records to comply with Making Tax Digital (MTD) for landlords, so you never end up in this position again.

Whether you’re a landlord with one flat in Reading or a portfolio in Oxford, the goal is the same: total compliance with minimum financial damage.

Further Reading on Let Property campaign

To better understand your specific situation, explore our dedicated regional guides:

How many years does the Let Property Campaign go back?

HMRC can go back up to 20 years if they believe the failure to pay was deliberate. If it was a “careless” mistake, they usually look back 6 years. If you took “reasonable care” but still got it wrong, the limit is typically 4 years. An expert helps determine which limit applies to you.

What are the penalties for the Let Property Campaign?

Penalties range from 0% to 100% of the tax owed. For voluntary disclosures where the landlord was “careless” but helpful, penalties are often between 0% and 15%. If HMRC finds you first, those rates jump significantly.

Can I include mortgage interest in my Let Property campaign disclosure?

Yes, but only according to the current rules. Since April 2020, you cannot deduct mortgage interest from your rental income to calculate profit. Instead, you receive a 20% tax credit. Failing to apply this correctly in a disclosure is a common reason HMRC rejects DIY submissions.

Do I have to pay the Let Property campaign full amount immediately?

Not necessarily. While HMRC prefers immediate payment, a Let Property Campaign expert can often negotiate a payment plan (Time to Pay arrangement) if you can demonstrate that a lump sum payment would cause “undue hardship.”

Does the Let Property campaign apply to holiday lets or Airbnb?

Yes. The Let Property Campaign covers all residential property, including specialized lets like Airbnb, student housing, and holiday rentals in areas like Oxford or Windsor. It does not cover commercial property (shops or offices).

What expenses can I claim to reduce my tax bill?

You can claim letting agent fees, property insurance, maintenance and repairs (not improvements), utility bills you paid, council tax during void periods, and professional fees like accountancy or legal costs related to the tenancies.

If you have undisclosed rental income, the sheer weight of “not knowing” is often worse than the tax bill itself. You might be wondering: How much do I actually owe? How far back will they go? Is there a way to estimate the damage before I talk to HMRC? This is where understanding the Let Property Campaign penalty calculator methodology becomes your most powerful tool. By learning how to calculate these figures, you move from a place of panic to a place of strategy.

In this guide, we will walk you through the exact process of using the Let Property Campaign framework to estimate your liabilities. We’ll cover the difference between tax, interest, and penalties, and provide a step-by-step roadmap to ensure you don’t pay a penny more than is legally required. Whether you are a landlord in Windsor, Oxford, or London, this manual is designed to give you total clarity.

Featured Snippet: What is the Let Property Campaign penalty calculator?

The Let Property Campaign penalty calculator is a framework used to estimate the total cost of disclosing unpaid rental tax. It combines the total tax owed per year, statutory interest (calculated from the date the tax was due), and a percentage-based penalty (0%–100%) determined by the taxpayer’s behavior and the timing of the disclosure.

Understanding the “Cost” Pillars of a Disclosure

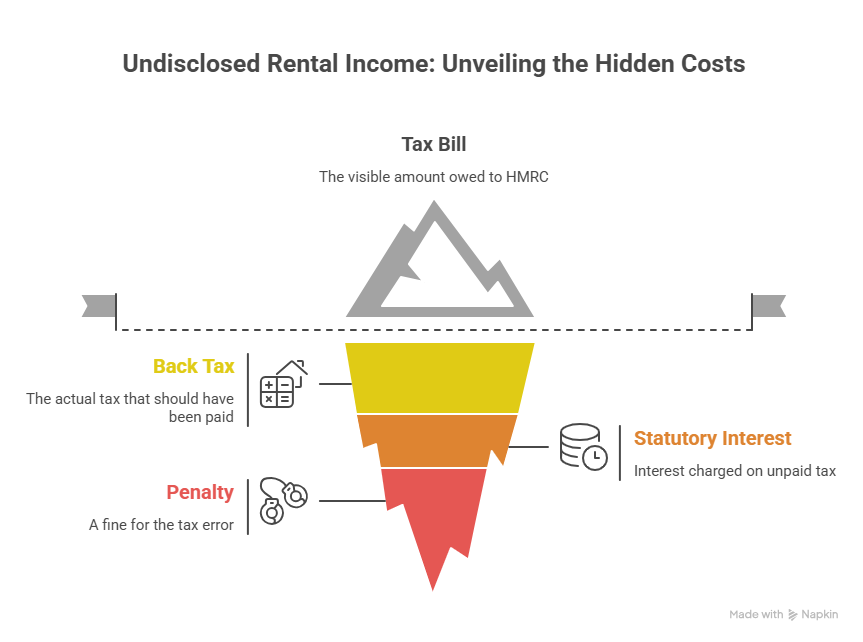

Before you start plugging numbers into a spreadsheet, you must understand that your final bill to HMRC isn’t just one number. It is built on three distinct pillars. If you miss one, your estimate will be dangerously low.

Pillar 1: The Back Tax (The Principal)

This is the actual amount of tax you should have paid on your rental profits. To find this, you must take your gross rental income and subtract “allowable expenses” (like repairs, insurance, and management fees). If you are a higher-rate taxpayer, you also need to account for the mortgage interest tax credit restrictions (Section 24).

Pillar 2: Statutory Interest

HMRC views unpaid tax as an interest-free loan you took from the government. To rectify this, they charge interest from the date the tax should have been paid until the date you actually pay it. With interest rates currently at decade-highs, this can add 20% or more to an old tax debt.

Pillar 3: The Penalty

This is the “fine” for the error. The percentage is applied to the tax amount (not the interest). This is the area where a specialist accountant provides the most value, as we can often argue for lower categories based on your circumstances.

Step-by-Step: How to Use the Penalty Calculator Framework

Since HMRC does not provide a single “one-click” calculator that handles every nuance, you must follow this structured framework to get an accurate estimate.

Step 1: Determine the Relevant Tax Years

How far back are you going?

4 Years: If you took “Reasonable Care” but made an honest mistake.

Note: Do not subtract the full mortgage payment. You can only deduct the interest element (and for individuals, this is now a 20% tax credit rather than a direct deduction from income).

Step 3: Determine Your Tax Band

Your rental profit is added to your other income (Salary, Dividends, etc.). If your total income crosses the £50,270 threshold (for 2025/26), you will owe 40% tax on the portion of rental profit sitting in the higher-rate band.

Step 4: Apply the Penalty Percentage

Use the table below to decide which percentage to apply to your tax total.

Behavior

Unprompted (You told them)

Prompted (They found you)

Reasonable Care

0%

0% – 30%

Careless

0% – 30%

15% – 30%

Deliberate

20% – 70%

35% – 70%

Step 5: Calculate Interest

You must apply the HMRC late payment interest rate to each year’s tax. Because rates change, it is best to use a specialized interest calculator or ask your HMRC Let Property Campaign expert in Slough to run the professional software.

Strategy Framework: Minimizing the “Penalty” Variable

The penalty is the only part of the equation that is negotiable. To minimize this, you must demonstrate the “Quality of Disclosure.”

Telling: Did you tell HMRC everything, or did you wait for them to ask?

Helping: Did you provide your spreadsheets and receipts quickly?

Giving Access: Did you allow HMRC to check your records?

Landlords in Reading and London who provide a “Full and Unprompted” disclosure can often see their penalties for carelessness reduced to 0%.

Real-World Example: The “Careless” Disclosure

Imagine a landlord in Oxford who didn’t declare £10,000 in rental profit per year for the last 4 years. They are a basic-rate (20%) taxpayer.

Tax Owed: £2,000 per year x 4 years = £8,000

Interest: (Estimate) £1,200

Penalty (Unprompted/Careless): Let’s say 10% = £800

Total Bill:£10,000

If this same landlord had waited for a “nudge letter,” the penalty could easily double or triple, and HMRC might insist on looking back 6 or 20 years instead of 4.

Pros and Cons of DIY Calculation vs. Professional Assistance

DIY Calculation

Pros: Free; gives a rough “ballpark” figure immediately.

Cons: High risk of missing tax credits; often results in overpaying tax or underestimating penalties; no protection if HMRC challenges the figures.

Professional Specialist (Felix & Co.)

Pros: Access to professional-grade Let Property Campaign penalty calculator software; expert negotiation of penalty categories; identifying obscure allowable expenses (e.g., specific proportions of home office/travel).

Cons: Upfront accountant fee. However, the tax savings usually far exceed the fee.

Why Location Matters: High-Value Service Areas

If you own property in Windsor or London, the stakes are higher. Rental yields are higher, and the likelihood of being pushed into the 40% or 45% tax bracket is almost certain. In these areas, HMRC’s “Connect” system is particularly aggressive in cross-referencing Land Registry data with high-value stamp duty records.

Our specialists in Reading, Slough, and Oxford understand the local market nuances, such as HMO (House in Multiple Occupation) regulations and how they impact your “Allowable Expenses” calculation.

Interest: Always mandatory; currently based on base rates + 2.5%.

Timeline: You have 90 days to pay once you notify HMRC of your intent to disclose.

Expert Advice: Always aim for “Unprompted” status to keep penalties at the minimum floor.

FAQ: People Also Ask

1. Can I use an online calculator for the Let Property Campaign?

There are basic tools online, but they rarely account for the complexities of Section 24 mortgage interest restrictions or changing interest rates. For an accurate disclosure, a manual calculation by a specialist is recommended to avoid HMRC rejecting your figures.

2. What happens if the calculator shows I owe more than I have?

Do not let this stop you from disclosing. Once the liability is calculated, we can help you negotiate a “Time to Pay” arrangement with HMRC, allowing you to pay the debt in monthly installments.

3. Does the penalty apply to the interest as well?

No. The penalty percentage is only applied to the “Tax Lost” (the principal). Interest is a separate charge that is added to the total.

4. How does the “10% rule” work for offshore property?

If the property is abroad, the rules change. Penalties for offshore income can be significantly higher (up to 200%) depending on the “territory” and the information-sharing agreements in place.

5. If my calculator shows £0 tax due, do I still need to disclose?

If your expenses and personal allowance mean no tax is due, you may not need to use the campaign, but you should still ensure your records are up to date. Making a “Nil” disclosure can sometimes be a strategic move to prevent future HMRC inquiries.

6. Is the calculator different for prompted disclosures?

The formula is the same, but the “Penalty %” will have a higher minimum. For example, a careless mistake that is prompted has a minimum penalty of 15%, whereas an unprompted one can be 0%.

From Uncertainty to Action

Using the Let Property Campaign penalty calculator methodology is the first step toward taking back control of your finances. While the numbers might seem daunting, remember that HMRC rewards those who come forward. By identifying your tax, interest, and penalty liabilities now, you can build a disclosure that is accurate, honest, and optimized to save you money.

Don’t let the fear of a calculation keep you in the dark. Whether you are in Slough, Windsor, or London, the best time to calculate your disclosure was yesterday; the second best time is today.

If you’ve been renting out property in the UK without declaring all of your rental income to HMRC, you are not alone — and you may still have the opportunity to put things right before the taxman comes to you. The HMRC Let Property Campaign is a government-backed voluntary disclosure scheme specifically designed for residential landlords with undeclared rental income. Understanding it — and acting on it quickly — could save you thousands of pounds in penalties and protect you from serious legal consequences.

In this guide, we explain exactly what the Let Property Campaign is, how it works, what penalties you could face, and how working with an experienced Let Property Campaign accountant can make the whole process as straightforward as possible.

What is the Let Property Campaign? (Featured Snippet)

The Let Property Campaign is an HMRC voluntary disclosure scheme for UK landlords who have undeclared rental income. It allows landlords to come forward, declare outstanding tax liabilities, pay what they owe (including interest), and typically receive lower penalties than if HMRC investigates first. The campaign has been open since 2013 and remains active.

What Is the HMRC Let Property Campaign?

The Let Property Campaign (LPC) was launched by HMRC in September 2013 as a targeted initiative to bring UK residential landlords who owe tax on rental income back into compliance. Unlike a full HMRC investigation — which can be costly, stressful, and result in heavy penalties — the LPC offers a structured, more forgiving route for landlords to disclose unpaid tax themselves.

It applies to landlords who rent out one or more residential properties in the UK and have not correctly declared their income to HMRC. This includes landlords who have filed no tax return at all, those who have understated their income, and those who have claimed ineligible expenses. You can find HMRC’s official guidance on the scheme at gov.uk.

The campaign is not a tax amnesty — you will still pay the tax you owe, plus interest. But landlords who come forward voluntarily under the LPC benefit from reduced penalty rates compared to those who wait for HMRC to come to them.

Who Does the Let Property Campaign Apply To?

The campaign is open to any UK individual landlord letting out residential property. This includes:

Landlords who have never registered for self-assessment

Landlords who filed returns but omitted or understated rental income

Landlords who inherited property and have since rented it out

Landlords with overseas rental income not declared in the UK

Landlords who rent out a room in their main residence beyond the Rent-a-Room allowance

The LPC does not cover commercial property, partnerships, or companies — for those cases, HMRC has separate disclosure routes.

How Far Back Does the Let Property Campaign Go?

One of the most common questions we receive at Felix Accountants is: “How far back does the Let Property Campaign go?” The answer depends on the nature of the non-disclosure.

HMRC applies a tiered look-back period based on the perceived intent of the landlord:

Innocent error (careless): 4 years back from the current tax year

Careless or negligent behaviour: 6 years back

Deliberate non-disclosure: 20 years back

For most landlords who simply didn’t realise they needed to declare rental income, the look-back period is typically 4 to 6 years. However, if HMRC decides the failure was deliberate, they can go back up to 20 years, which can result in a very significant tax bill.

Important:

Coming forward under the Let Property Campaign proactively — before HMRC contacts you — is classified as ‘unprompted’. This gives you the most favourable penalty treatment and signals to HMRC that you are acting in good faith.

Let Property Campaign Penalties: What Will You Actually Pay?

Many landlords delay disclosing undeclared rental income because they worry about the financial hit. But the penalty structure under the Let Property Campaign is designed to reward early, voluntary disclosure — meaning the sooner you act, the less you pay.

Penalty Rates at a Glance

Here is how the penalty rates break down depending on your disclosure type:

Disclosure Type

Penalty Range

Typical Scenario

Unprompted

0% – 30%

Landlord comes forward voluntarily

Prompted

15% – 30%

HMRC contacts landlord first

Prompted (deliberate)

30% – 70%

Deliberate non-disclosure

Offshore/concealment

Up to 200%

Offshore assets or deliberate concealment

In addition to penalties, HMRC charges interest on unpaid tax from the date the tax was due. This is currently calculated at the Bank of England base rate plus 2.5%, which means the longer you leave it, the more the interest builds up. A qualified Let Property Campaign accountant can use HMRC’s online tools to calculate the exact interest and penalty figures before you make a formal disclosure.

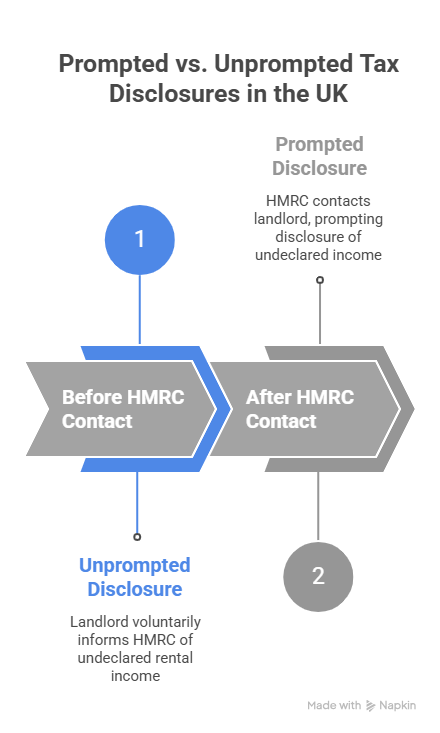

Prompted vs Unprompted Disclosure

These two terms matter enormously when it comes to your penalties. An unprompted disclosure means you contact HMRC before they contact you. A prompted disclosure means you only come forward after receiving a nudge letter, a compliance check, or direct contact from HMRC.

The difference can be dramatic: unprompted disclosures for non-deliberate errors attract penalties starting at 0%, while prompted disclosures for the same error can attract 15% or more. If you have received an HMRC nudge letter, do not delay — act immediately.

Step-by-Step: How to Make a Let Property Campaign Disclosure

The process has four main stages. Getting each one right is critical to minimising your tax bill and avoiding further investigation.

Step 1 – Notify HMRC

Before you can make a formal disclosure, you must notify HMRC of your intention to disclose. You do this online at gov.uk. HMRC will then issue you with a unique disclosure reference number.

Step 2 – Gather All Relevant Records

This is where most landlords need professional help. You will need records of all rental income received, any eligible expenses you wish to claim, bank statements and tenancy agreements, and records of any mortgage interest (though the rules here changed significantly from 2017 onwards).

Step 3 – Calculate the Tax, Interest, and Penalties Owed

Using HMRC’s disclosure calculator — or more accurately, working with an experienced Let Property Campaign specialist — you will calculate the precise amount owed for each tax year in the look-back period. This includes income tax on net rental profit, National Insurance if applicable, interest on the unpaid tax, and any penalties applied at the appropriate rate.

Step 4 – Submit the Disclosure and Pay

Once the figures are agreed and your disclosure reference number is in hand, you submit the full disclosure to HMRC online and make payment. HMRC gives you 90 days from your initial notification to complete the process.

Pro tip from Felix Accountants:

Do not attempt a Let Property Campaign disclosure without professional guidance. Errors in your disclosure — overstating income, missing eligible deductions, or misclassifying expenses — can result in a higher tax bill than necessary, or flag your case for further investigation.

Why You Need a Let Property Campaign Accountant

The LPC process appears straightforward on paper. In practice, calculating the correct figures, understanding which expenses are allowable, navigating post-2017 mortgage interest relief restrictions, and presenting your disclosure in the most favourable light requires genuine expertise. The wrong approach can cost you significantly more than the accountant’s fees.

At Felix Accountants, our Let Property Campaign specialists have helped landlords across London, Windsor, Slough, Reading, and Oxford navigate the process smoothly and cost-effectively. We advise on:

Which tax years need to be included in your disclosure

How to calculate your allowable expenses correctly, including repairs, letting agent fees, and insurance

How mortgage interest restrictions apply to your specific situation

Whether any wear and tear allowances or capital allowances apply

How to present your disclosure to minimise your penalty exposure

How to respond if HMRC asks further questions after your disclosure

Whether you are based in London or use our specialist services in Windsor, Oxford, Reading, or Slough, our team provides clear, fixed-fee guidance so you know exactly what you will pay before we begin.

Let Property Campaign: Reasonable Excuse — Can You Avoid Penalties Entirely?

HMRC does recognise the concept of a “reasonable excuse” — a genuine reason why you failed to declare your rental income. If accepted, it can reduce or even eliminate your penalties entirely. However, HMRC applies the standard strictly.

What HMRC may accept as a reasonable excuse:

Bereavement of a close family member around the time returns were due

Serious or life-threatening illness preventing you from managing your affairs

A fire, flood, or theft that destroyed your financial records

Genuine uncertainty about whether income was taxable (in limited circumstances)

What HMRC will typically not accept:

Not knowing you had to register for self-assessment

Relying on someone else who failed to act on your behalf

Forgetting to file or pay

Lack of funds to pay

If you believe you have a reasonable excuse, document it thoroughly. Our team at Felix Accountants can advise on whether your circumstances are likely to be accepted and how to present your case effectively.

Is the Let Property Campaign Still Running in 2026?

Yes. As of 2026, the HMRC Let Property Campaign is still open and active. There is currently no announced end date for the scheme. However, HMRC has significantly increased its data-matching capabilities in recent years — using information from letting agents, Land Registry records, deposit protection schemes, and overseas disclosures — which means it is becoming increasingly likely that undeclared landlords will be identified proactively.

The window of opportunity to benefit from the most favourable penalty treatment is narrowing. If you are a landlord with any undeclared rental income, now is the time to act — not when an HMRC letter arrives on your doormat.

Pros and Cons of Using the Let Property Campaign

Advantages of Making a Voluntary Disclosure

Lower penalties — potentially 0% for unprompted non-deliberate disclosures

Avoidance of a full HMRC investigation, which can be far more intrusive and costly

Peace of mind and removal of a significant source of financial and legal stress

Ability to correct the record and move forward with a clean compliance history

More control over the process compared to being investigated by HMRC

Potential Drawbacks to Be Aware Of

You will pay all the tax owed plus interest — there is no reduction in the underlying liability

If HMRC finds errors in your disclosure, it can prompt further scrutiny

The 90-day window to complete disclosure after notifying HMRC can feel tight

Without professional help, it is easy to overclaim or underclaim expenses

Property Campaign Windsor

A Real-World Example: What a Let Property Campaign Disclosure Looks Like

Case Study (anonymised):

A landlord in Windsor came to Felix Accountants after letting out two buy-to-let properties for six years without filing self-assessment returns. Combined rental income over the period was approximately £78,000. After allowable expenses, the taxable profit was significantly lower. We prepared a full 6-year look-back disclosure, correctly applied mortgage interest restrictions, and filed an unprompted disclosure with HMRC. The final settlement included back taxes and interest — but zero penalties, saving the client over £4,500 compared to a prompted disclosure at standard penalty rates.

Related Articles You May Find Useful

If you found this guide helpful, you may also want to read our detailed resources on the Let Property Campaign on the Felix Accountants website:

Frequently Asked Questions About the Let Property Campaign

1. How far back can HMRC go under the Let Property Campaign?

HMRC can typically look back 4 years for innocent errors, 6 years for careless non-disclosure, and up to 20 years for deliberate evasion. Most landlords fall into the 4–6 year category, but your specific situation should be assessed by a qualified accountant before you notify HMRC.

2. What are the penalties for not declaring rental income?

Penalties range from 0% for unprompted voluntary disclosures of innocent errors up to 200% for deliberate offshore concealment. In addition to penalties, HMRC charges interest on all unpaid tax from the date it was originally due. Acting voluntarily before HMRC contacts you will always produce the lowest penalty outcome.

3. Can I use the Let Property Campaign if HMRC has already contacted me?

Yes, but your disclosure will be classified as ‘prompted’, which means higher minimum penalty rates apply. Even so, making a full and accurate disclosure remains far better than ignoring HMRC’s contact. If you have received a nudge letter or compliance check notice, contact a Let Property Campaign specialist immediately.

4. How much does it cost to use a Let Property Campaign accountant?

Fees vary depending on the number of years involved, the complexity of your property portfolio, and the work required to reconstruct records. At Felix Accountants, we offer transparent, fixed-fee packages for Let Property Campaign disclosures. A free initial consultation will give you a clear quote before any work begins.

5. What happens after I submit my Let Property Campaign disclosure?

HMRC will review your disclosure and, in most cases, accept it and issue a statement of account for payment. In some cases, they may ask clarifying questions. If your disclosure is accurate and complete, the process typically concludes smoothly. You should retain all supporting records for at least 5 years in case HMRC follows up.

6. Is the Let Property Campaign the same as a tax amnesty?

No. The Let Property Campaign is not an amnesty — you will still pay all the tax you owe plus statutory interest. The benefit is in the reduced penalties compared to what HMRC would impose following a formal investigation. It is best understood as a structured, lenient route back into compliance rather than a debt write-off.

7. Can overseas rental income be disclosed under the Let Property Campaign?

Yes, but it is more complex. Overseas rental income may also be subject to double taxation agreement provisions, foreign tax credits, and additional HMRC reporting requirements. Felix Accountants has specific experience with overseas property disclosures under the LPC — contact us if you have international rental income to declare.

Get Expert Help With Your Let Property Campaign Disclosure Today

Whether you are a landlord in London, Windsor, Slough, Reading, or Oxford — or anywhere else in the UK — Felix Accountants offers specialist Let Property Campaign advice and full disclosure management. Our team combines deep HMRC compliance knowledge with a practical, client-first approach.

Visit us at felixaccountants.com or call our team directly. We make the Let Property Campaign process simple, transparent, and as cost-effective as possible for every landlord we work with.

Felix Accountants are specialist Let Property Campaign accountants serving landlords across London, Windsor, Slough, Reading and Oxford. This article is for general guidance only and does not constitute formal tax or legal advice. Always consult a qualified professional before making a disclosure to HMRC.

Published by Felix Accountants | Let Property Campaign Specialists across London, Windsor, Slough, Reading & Oxford

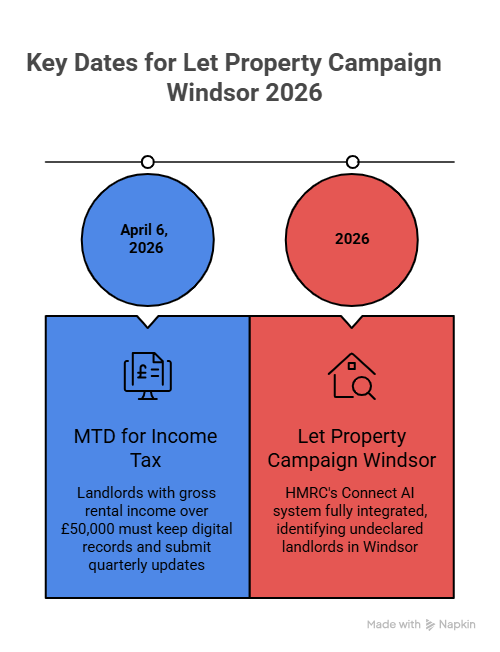

Let Property Campaign Windsor: The Definitive 2026 Disclosure Handbook for Royal Borough Landlords

The Let Property Campaign Windsor is currently the most significant tax compliance initiative for property owners in the Royal Borough of Windsor and Maidenhead. As we move through 2026, the era of “invisible” rental income has officially ended. HM Revenue & Customs (HMRC) has fully integrated its “Connect” AI system, a multi-billion pound data-mining tool that cross-references over 30 different data sources to identify undeclared landlords. For those owning prestigious assets in the SL4 and SL5 postcodes, the high rental yields that make Windsor attractive also make it a primary target for tax enforcement.

The Property Campaign Windsor Market and Why HMRC is Watching

Windsor is not a standard rental market; it is a high-wealth ecosystem. Properties here range from historic Grade II listed townhouses near Windsor Castle to modern luxury apartments in Eton.

The Short-Term Let Surge

Windsor’s status as a global tourist destination means short-term rentals via platforms like Airbnb are at an all-time high. In 2024, HMRC mandated that these platforms share host data directly. If you have been letting out a spare room or a whole property for the Royal Ascot or summer tourism without declaring the income, the Let Property Campaign Windsor is your only route to avoiding a full-scale criminal investigation.

From April 6, 2026, the rollout of MTD for Income Tax has changed the game. Landlords with a gross rental income over £50,000 must now keep digital records and submit quarterly updates. This shift to real-time reporting is exposing years of historical “gaps” in tax filings.

Step-by-Step: Navigating the Let Property Campaign

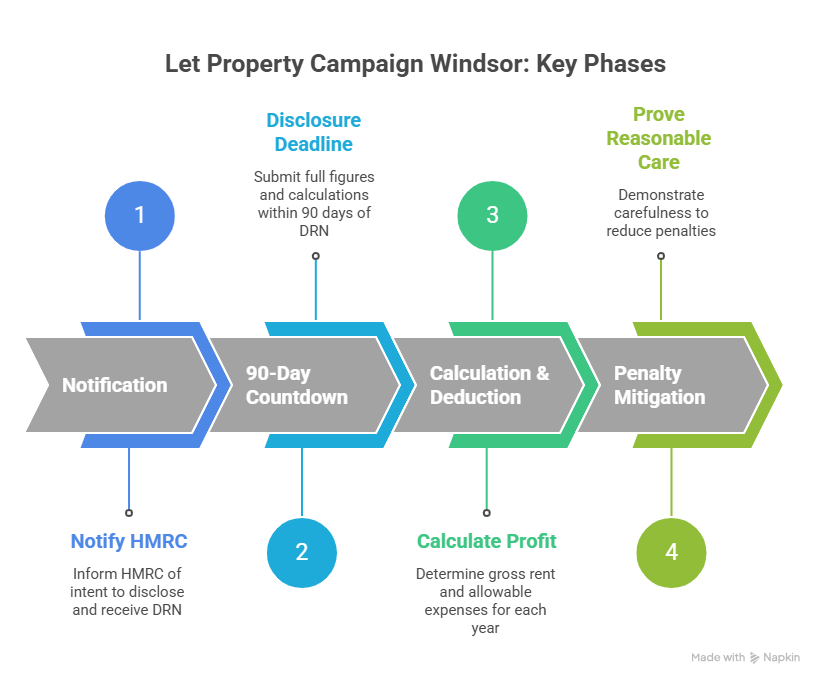

Participating in the campaign is a structured process. It is not as simple as sending a check; it requires a detailed forensic look at your finances over several years.

Phase 1: The Notification

The first step is to notify HMRC of your intent to disclose. Once this is done, you are assigned a Disclosure Reference Number (DRN). This “stops the clock” on certain more aggressive enforcement actions, but it starts a new 90-day countdown to provide the full figures.

Phase 2: Calculating Undeclared Income and Deductions

This is where professional precision is required. You must calculate your gross rent for every year you failed to file. However, you are only taxed on the profit. In Windsor, where property maintenance is exceptionally high, identifying every “allowable expense” is vital.

Repairs vs. Improvements: Replacing a Victorian sash window like-for-like is a deductible repair. Installing a brand-new conservatory is a capital improvement, which is handled differently.

Management Fees: Premium Windsor letting agents often charge 12%–15%. We ensure every penny of this is deducted.

Penalty Mitigation and “Reasonable Care”

HMRC’s penalty regime in 2026 is based on “behavioral” assessments. If we can prove you acted with “Reasonable Care” or that your failure was “Careless” rather than “Deliberate,” we can reduce penalties from 100% down to 0%–20%.

To ensure your blog provides maximum value and answers the most common queries your clients have, I have developed 6 unique, highly detailed FAQs for each of the three articles. These are tailored to the 2026 tax landscape and the specific needs of Windsor property owners.

Property Campaign Windsor

FAQs for Property Campaign Windsor

What exactly triggers an HMRC “nudge letter” in Windsor?

In 2026, the trigger is usually an “anomaly” found by the Connect AI system. For example, if the Land Registry shows you own a second property in SL4, but your tax return shows no rental income, or if a deposit was protected with a scheme but no corresponding tax was paid, a letter is automatically generated.

Can I use the Let Property Campaign if I have multiple properties in the Royal

Borough? Yes. The campaign is designed for individual landlords regardless of whether they own a single studio in Clewer or a large portfolio of HMOs (Houses in Multiple Occupation) across Windsor and Maidenhead.

Is there a minimum amount of rental income before I need to disclose?

You have a £1,000 “Property Allowance” each year. If your gross rental income (before expenses) is over £1,000, you must declare it. For most Windsor rentals, where monthly rents exceed this annually, disclosure is almost always mandatory.

How does the 2026 Making Tax Digital (MTD) rollout affect my disclosure?

MTD requires real-time digital record-keeping for those earning over £50,000. If you are moving onto MTD software now, any “missing years” in your digital history will be immediately obvious to HMRC, making a voluntary disclosure via the campaign even more urgent.

What if I let my property to family members at a “mate’s rate”?

Even if you charge below-market rent, the income is still taxable. However, you cannot claim a tax loss if your expenses exceed the subsidized rent. The campaign allows you to regularize these informal arrangements.

Will HMRC visit my Windsor property as part of the campaign?

Generally, no. The Let Property Campaign is a “desk-based” disclosure. By providing a full and accurate digital disclosure, you significantly reduce the chance of an intrusive face-to-face audit or property inspection. Learn More

Many UK residents believe that if their rental property is located in another country, the income is “off-limits” to HMRC. This is a dangerous misconception. If you are a UK tax resident, you are generally taxed on your worldwide income. This includes that holiday home in Spain, the apartment in Dubai, or the family home in India. The Let Property Campaign is not just for domestic landlords; it is a critical lifeline for those with international portfolios to regularize their tax affairs before the “Worldwide Disclosure Facility” or automated data sharing catches up with them.

In this deep-dive guide, we will explore the specific complexities of disclosing foreign rental income, how Double Taxation Agreements (DTAs) work in your favor, and why the penalties for overseas non-disclosure under the Let Property Campaign can be significantly harsher than for UK-based properties. Whether you are in Windsor, Oxford, or London, if your assets are abroad, this guide is for you.

Featured Snippet: Does the Let Property Campaign apply to overseas property?

Yes, the Let Property Campaign applies to UK tax residents who have undisclosed rental income from overseas properties. While the campaign is the primary route for domestic disclosure, it can also be used for foreign residential lets. However, failure to disclose overseas income can lead to “Requirement to Correct” penalties, which can reach 200% of the tax due.

The days of “hidden” offshore bank accounts and untraceable foreign property titles are effectively over. HMRC now employs a sophisticated digital dragnet to identify UK residents with interests abroad.

1. The Common Reporting Standard (CRS)

Over 100 countries now participate in the CRS, an automated system that shares financial account information across borders. If you have a bank account in France or South Africa receiving rent, that information is automatically flagged to HMRC’s “Connect” system.

2. The Worldwide Disclosure Facility (WDF)

While the Let Property Campaign is excellent for residential property, HMRC also runs the WDF for general offshore income. However, for many landlords, the LPC remains a viable and often more specialized route if the income is strictly residential.

3. Requirement to Correct (RTC)

The RTC legislation introduced a legal obligation for taxpayers to correct any offshore tax non-compliance. Missing the deadline for this has created a new penalty regime where the starting point is often 150% to 200% of the tax owed.

Key Challenges for Overseas Landlords

Disclosing foreign income under the Let Property Campaign involves more than just converting currency. You must navigate a minefield of international tax laws.

Foreign Tax Credits and Double Taxation

If you have already paid tax on your rental income in the country where the property is located, you shouldn’t have to pay it all over again in the UK. This is managed through Double Taxation Agreements (DTAs). You can usually claim Foreign Tax Credit Relief (FTCR) to offset the tax paid abroad against your UK liability.

Note: You cannot claim more credit than the UK tax due on that same income.

Currency Conversion Hurdles

HMRC requires all figures to be reported in GBP. This means you must convert your rental income and expenses using the exchange rates applicable at the time the income was received or the expense was incurred. Using a single “end-of-year” rate is often inaccurate and can be challenged by HMRC.

Non-UK Allowable Expenses

Not all expenses allowed in a foreign country are allowed in the UK. For example, some countries allow for “depreciation” of the building, which is strictly prohibited for UK residential property tax calculations.

Comparison: UK vs. Overseas Disclosure Penalties

The stakes are much higher when the property crosses a border. HMRC categorizes countries into “territories” based on how much information they share.

Feature

UK Property Disclosure

Overseas Property Disclosure

Data Sharing

High (Land Registry/Banks)

Very High (CRS/Automatic Exchange)

Max Penalty

100% of tax due

Up to 200% (Category 2 & 3 territories)

Look-back Period

Up to 20 years

Up to 20 years (Standard RTC rules apply)

Complexity

Moderate

High (DTAs, FTCR, Currency)

Step-by-Step: Disclosing Foreign Income via the Let Property Campaign

If you have a property in Slough, Reading, or London but the income is coming from an apartment in Spain, here is the roadmap to compliance.

Step 1: Determine Your Tax Residency

Are you a UK resident? If you spend more than 183 days in the UK, or if your “only home” is here, you are likely taxed on your worldwide income. This is the foundation of your disclosure.

Step 2: Collect International Records

You need foreign bank statements, local tax returns filed in the property’s country, and receipts for repairs. These must be translated if necessary.

Step 3: Calculate the “Net” in GBP

Apply the correct HMRC exchange rates. Subtract UK-allowable expenses from the gross rent.

Step 4: Apply Foreign Tax Credit Relief

Identify the tax already paid to the foreign government. This will be deducted from your UK tax bill, but it will not reduce the interest or penalties charged by HMRC.

Step 5: Draft the Narrative

Explain why the income wasn’t declared. Many landlords in Windsor or Oxford genuinely believed the DTA meant they didn’t have to tell HMRC at all. While this isn’t a “Reasonable Excuse,” it can be argued as “Careless” rather than “Deliberate,” saving you 50% or more in penalties.

Strategy Framework: The “Territory” Assessment

When using the Let Property Campaign for overseas assets, you must identify your “Territory Category”:

Category 1: Countries like the USA, France, and Germany (High info sharing). Penalties are similar to UK rates.

Category 2: Countries with less robust sharing. Penalties are higher.

Category 3: Countries that do not share information. Penalties are the most severe.

Landlords in Windsor, London, and Oxford often have diverse international portfolios. HMRC’s “High Net Worth Unit” specifically looks for discrepancies between a taxpayer’s lifestyle in the UK and their reported global income. If you own a high-value home in London but report minimal income, HMRC may use their “Connect” system to look for foreign property ties that haven’t been declared.

The risk isn’t just a fine; it’s a full-scale investigation into all your global assets. The Let Property Campaign acts as a “firebreak,” allowing you to settle the property aspect before it leads to a wider audit.

Overview: Overseas Disclosure Summary

Rule: UK residents are taxed on worldwide rental income.

Relief: You can usually deduct tax paid abroad from your UK bill (Foreign Tax Credit Relief).

Currency: All income must be converted to GBP using HMRC-approved rates.

Penalties: Can reach 200% if the property is in a non-cooperative territory.

Opportunity: The Let Property Campaign is the best way to voluntarily disclose residential foreign lets.

FAQ: People Also Ask

1. If I paid tax in Spain, why do I owe HMRC?

UK tax rates are often higher than foreign rates. You pay the difference to HMRC. For example, if you paid 19% in Spain but your UK marginal rate is 40%, you owe HMRC the remaining 21%. Furthermore, you are legally required to report the income even if no tax is due.

2. What if the property is owned by a foreign company?

The Let Property Campaign is for individuals. If the property is owned through an offshore company or trust, different (and often more complex) disclosure rules apply. You should seek specialized advice immediately.

3. Can I claim travel expenses to visit my overseas property?

HMRC is very strict here. You can only claim the “wholly and exclusively” part of the trip. If you spent 2 days at the property and 12 days on the beach, the flight cost is generally not deductible.

4. Does the 90-day deadline apply to overseas disclosures?

Yes. Once you notify HMRC via the Digital Disclosure Service, you have 90 days to prepare the calculations and pay the debt. International disclosures often take longer to prepare due to the need for foreign records, so start gathering data before you notify.

5. What is the “Requirement to Correct” (RTC)?

It was a piece of legislation that required everyone with offshore tax issues to disclose by September 2018. Because that deadline has passed, any disclosure made now is automatically subject to the much higher “Failure to Correct” penalty regime.

6. My foreign property is at a loss. Do I still disclose?

Yes. Reporting a foreign loss is beneficial as it can often be carried forward to offset future profits from the same foreign property business.

Bringing Your Global Wealth Home

Handling an overseas property disclosure alone is a recipe for disaster. Between currency fluctuations, treaty overlaps, and the looming threat of 200% penalties, the technical margin for error is zero.

The Let Property Campaign is your opportunity to bring your international affairs into the light on your own terms. By acting now, you protect your UK reputation, secure your assets in London, Windsor, or Reading, and ensure that your foreign investments remain a blessing, not a legal curse.

Don’t let a border be the reason you face a 200% fine.

If you have undisclosed rental income, the Let Property Campaign is your best route to making things right with HMRC before they find you first. But for most landlords, the biggest hurdle isn’t just the back taxes—it’s the fear of the unknown, specifically: “How much is an accountant going to charge me to fix this?”

In this comprehensive guide, we break down the reality of Let Property Campaign accountant fees, what factors influence the price, and why the “cheapest” option might end up being the most expensive mistake you ever make.

What is the Let Property Campaign?

The Let Property Campaign is an ongoing disclosure opportunity by HMRC that allows individual landlords who have failed to declare their rental income to come forward voluntarily. By doing so, landlords can benefit from lower penalty rates compared to those HMRC catches through their own investigations.

Featured Snippet Answer:

Accountant fees for the Let Property Campaign typically range from £500 to £2,500+, depending on the number of tax years involved, the complexity of your property portfolio, and the quality of your records. A specialist accountant ensures you claim all allowable expenses, potentially saving you thousands in tax and penalties.

Why You Need a Specialist for Your Disclosure

You might be tempted to handle the disclosure yourself or ask a high-street accountant who handles general retail accounts. However, the Let Property Campaign is a specialized area of tax law.

HMRC’s “Connect” computer system pulls data from the Land Registry, estate agents, and even social media. When you submit a disclosure, it needs to be bulletproof. A specialist doesn’t just “fill in forms”; they provide a shield between you and HMRC, ensuring that the “reasonable care” argument is used to minimize penalties.

Breaking Down Accountant Fees: What Are You Paying For?

When you receive a quote for Let Property Campaign assistance, the fee usually covers several critical stages of work. Understanding these will help you compare quotes accurately.

1. Initial Assessment and Scoping

Before an accountant can give you a fixed price, they must review the “health” of your tax affairs.

How many years have been missed?

Are you a UK resident or a non-resident landlord?

Is the property owned individually, jointly, or through a company?

2. Data Reconstruction and Calculation

This is the most labor-intensive part of the process. If you haven’t kept perfect records, your accountant will need to reconstruct your profit and loss statements. This involves:

Analyzing bank statements for rental income.

Identifying every possible allowable expense (repairs, insurance, management fees, etc.).

Calculating the finance cost restriction (Section 24) if you are a higher-rate taxpayer.

3. The Disclosure Submission

The digital disclosure involves more than just numbers. It requires a narrative. Your accountant must explain why the tax wasn’t paid. Was it a “failure to take reasonable care,” or was it “deliberate”? The way this is phrased can be the difference between a 0% penalty and a 70% penalty.

4. Negotiating the Settlement

After submission, HMRC may ask follow-up questions. A specialist accountant includes representation in their fee, ensuring they handle the “back-and-forth” so you don’t have to.

Average Fee Structures for Landlord Disclosures

While every case is unique, here is a general framework of what you can expect to pay for professional Let Property Campaign services.

Complexity Level

Description

Estimated Fee Range

Low

1 Property, 1–3 years missed, good records

£500 – £950

Medium

1–2 Properties, 4–10 years missed, partial records

£1,000 – £1,800

High

Multiple properties, 10–20 years, poor records, non-resident

£2,000 – £5,000+

Factors That Increase the Cost:

Missing Records: If the accountant has to manually download and categorize five years of bank statements, the hourly or fixed rate will climb.

Capital Gains Issues: If you sold a property during the period of non-disclosure, the complexity triples.

HMRC Inquiry: If HMRC has already sent you a “nudge letter,” the stakes are higher and the work is more urgent.

The “Cost” of Not Hiring a Specialist

It is a common mistake to view accountant fees as a pure expense. In reality, a specialist in the Let Property Campaign often pays for themselves through:

Expense Optimization: Many landlords don’t realize they can claim for things like property specific proportions of phone bills, travel to the property, or certain legal fees.

Penalty Mitigation: HMRC penalties are based on your behavior. An expert can argue for the lowest possible percentage by proving your disclosure is “unprompted” and “full.”

Interest Calculations: HMRC interest rates fluctuate. Accountants use specialized software to ensure you aren’t overcharged on the statutory interest.

Step-by-Step: The Process of Working with an Accountant

If you choose to work with a firm like Felix & Co., here is the roadmap you can expect:

Step 1: The Discovery Call

You’ll discuss the timeline of your rental income. It is vital to be 100% honest here. The Let Property Campaign only protects you if your disclosure is full and accurate.

Step 2: The Formal Quote

Based on the number of years and properties, you’ll receive a fixed-fee quote. This provides peace of mind—you won’t be hit with “hidden hours.”

Step 3: Information Gathering

You’ll provide bank statements, mortgage interest certificates, and receipts for repairs.

Step 4: Draft Calculations

Your accountant will show you the estimated tax, interest, and penalties due. You’ll review these before anything is sent to HMRC.

Step 5: Submission & Payment Plan

Once you approve, the disclosure is submitted. If you cannot afford the lump sum, your accountant can help negotiate a Time to Pay arrangement with HMRC.

Comparison: DIY Disclosure vs. Professional Representation

Feature

DIY Disclosure

Professional Accountant

Accuracy

High risk of missing expenses

Maximum tax efficiency

Penalty Risk

HMRC may challenge “Reasonable Care”

Expertly negotiated penalties

Stress Level

High (dealing with HMRC directly)

Low (Agent handles all comms)

Time Investment

20–40+ hours of research/math

Minimal (just providing documents)

Outcome

Potential for future audits

Peace of mind and “Full Disclosure”

Serving Landlords Across the UK

Whether you are a local landlord or an expat living abroad, tax laws apply the same way. We provide specialized support for the Let Property Campaign in these key areas:

Windsor: Specialized advice for high-value rental portfolios and HMOs.

Oxford: Expert tax planning for academic and professional lets.

London: Navigating the complexities of the capital’s rental market and non-resident landlord status.

Reading & Slough: Localized support for landlords facing HMRC nudge letters.

Google AI Overview: Quick Facts

What is the Let Property Campaign? A voluntary disclosure scheme for landlords to report unpaid tax on rental income.

Who can use it? Individual landlords (not companies or trusts) renting out residential property in the UK or abroad.

What are the costs? You must pay the back tax, interest, and a penalty. Accountant fees are separate but highly recommended to ensure accuracy.

How far back does HMRC go? Up to 20 years depending on why the tax wasn’t paid (innocent mistake vs. deliberate evasion).

1. Can I use the Let Property Campaign if HMRC has already contacted me?

Yes, but it may be considered a “prompted” disclosure. This usually results in higher penalties than an “unprompted” disclosure. However, using the campaign’s framework is still better than waiting for a full tax investigation.

2. What happens if I can’t afford to pay the tax due?

HMRC is often willing to set up a payment plan (Time to Pay) if you disclose voluntarily. A specialist accountant can help present your financial position to HMRC to secure a manageable monthly installment.

3. Does the campaign cover commercial property?

No. The Let Property Campaign is strictly for individual landlords letting out residential property. If you have undisclosed income from commercial property, you must use the Digital Disclosure Service under a different category.

4. Will I go to jail for not declaring rental income?

Criminal prosecution for rental tax is rare for those who come forward voluntarily. HMRC’s primary goal is to collect the tax, interest, and penalties. The Let Property Campaign is specifically designed to bring people back into the system without criminal proceedings, provided the disclosure is honest.

5. How long does the process take?

Once you notify HMRC of your intent to disclose, you have 90 days to calculate and submit your figures. An accountant typically needs 2–4 weeks to prepare a high-quality disclosure depending on the volume of data.

6. Are accountant fees for the disclosure tax-deductible?

Generally, the cost of preparing a tax return is not deductible against rental income for individuals. However, the peace of mind and the tax savings found through professional expertise far outweigh the lack of deductibility.

Investment vs. Expense

Navigating the Let Property Campaign alone is like walking through a minefield without a map. While the accountant fees might seem like an added burden, they are a vital investment in your financial security. A mistake in your disclosure can lead to HMRC opening a full inquiry into all your financial affairs—not just your property.

By hiring an expert, you ensure that every allowable expense is claimed, every penalty is challenged, and your reputation with HMRC is restored.

If you have received a “nudge letter” from HMRC or have suddenly realized that your rental income hasn’t been declared for several years, your first instinct is likely panic. You aren’t alone. Thousands of landlords across the UK find themselves in this exact position every year. The primary source of that anxiety? Let Property Campaign penalties.

The fear of a massive, life-altering fine often keeps landlords in the shadows, but staying there is the most expensive mistake you can make. In this guide, we will strip away the jargon and explain exactly how HMRC calculates penalties, the difference between an “innocent mistake” and “deliberate evasion,” and—most importantly—how you can reduce your financial exposure by using the Let Property Campaign correctly.

Featured Snippet: What are the penalties for the Let Property Campaign?

HMRC penalties for the Let Property Campaign typically range from 0% to 100% of the unpaid tax. The exact rate depends on whether your disclosure is unprompted (you told them first) or prompted (they caught you), and whether the error was due to reasonable care, carelessness, or deliberate concealment. Voluntary disclosures usually result in significantly lower fines.

Understanding the Let Property Campaign Framework

Before we dive into the percentages, it’s crucial to understand what the Let Property Campaign (LPC) actually is. It is an ongoing opportunity for individual landlords to bring their tax affairs up to date on the best possible terms.

HMRC’s “Connect” database is now more sophisticated than ever, pulling data from the Land Registry, banks, and deposit protection schemes. They likely already know about your rental property. The LPC is your “get out of jail relatively cheaply” card. If you come forward before they open an official inquiry, you are making an unprompted disclosure, which is the single most important factor in lowering your penalty.

The Three Pillars of HMRC Penalty Calculations

HMRC does not just pick a number out of a hat. They use a strict statutory framework to determine your fine. To understand your potential “bill,” you need to look at three things: Behavior, Timing, and Cooperation.

1. Taxpayer Behavior (The “Why”)

This is the most subjective and critical part of your disclosure. HMRC categorizes your failure to pay tax into three buckets:

Reasonable Care: You tried to do the right thing but made a mistake (e.g., you thought a certain expense was deductible when it wasn’t). Penalties can be 0%.

Careless: You failed to take reasonable steps to get your tax right (e.g., you didn’t bother to check the rules or keep records). Penalties are usually between 0% and 30%.

Deliberate: You knew you owed tax and intentionally didn’t declare it. Penalties start at 20% and can soar to 70%.

Deliberate and Concealed: You hid income and took active steps to cover your tracks (e.g., creating false invoices). This is where you hit the 100% (or higher for offshore income) penalty mark.

2. Timing (The “When”)

Unprompted Disclosure: You contact HMRC before they have any reason to believe your tax affairs are wrong. This earns you the lowest possible penalty rates.

Prompted Disclosure: You come forward after HMRC sends you a letter or starts an inquiry. Even if you “confess,” the minimum penalty floor is much higher because they had to find you first.

3. Quality of Disclosure (The “How”)

Even after you’ve been categorized, you can still lower the fine within that category’s range by:

Telling: Fully explaining the omissions.

Helping: Providing all necessary records and calculations quickly.

Giving: Allowing HMRC access to records they might not already have.

Penalty Percentage Breakdown: A Comparison Table

The following table illustrates how the “penalty floors” change based on your behavior and whether you or HMRC moved first.

Behavior Category

Unprompted Disclosure (Min/Max)

Prompted Disclosure (Min/Max)

Reasonable Care

0% / 0%

0% / 30%

Careless

0% / 30%

15% / 30%

Deliberate

20% / 70%

35% / 70%

Deliberate & Concealed

30% / 100%

50% / 100%