It starts innocently enough: a newly registered UK company receives what looks like an official Fake Companies House letters the envelope feels formal. Inside is a document stamped with a government-like logo, written in formal language, and bearing a QR code in the corner. The letter claims that the company owes £271.00 for publishing legal information — and warns that failure to pay might affect its registration status.

Fake Companies House Letters

But here’s the truth: it’s a scam.

Fake Companies House letters are being sent to businesses across the UK, and many unsuspecting business owners are falling victim. In this article, we’ll explore how these scams work, how to spot the red flags, and what steps to take if you receive one.

Why Fake Companies House Letters Are a Growing Concern

In recent weeks, a number of UK startups and newly registered companies have reported receiving these fraudulent letters. At first glance, they appear legitimate:

The language mimics official government correspondence.

The branding is eerily similar to that of Companies House.

QR codes are included to make payment easy — and urgent.

But look closer and you’ll find inconsistencies. Some letters mention vague “legal publication fees,” while others threaten to “deregister” your company if you don’t comply. None of these demands come from Companies House.

Fake Companies House Letters

These scams target busy entrepreneurs, especially first-time business owners unfamiliar with post-incorporation procedures. That’s what makes them so dangerous.

What’s actually Going On?

The scammers behind these fake Companies House letters are betting on your uncertainty. They craft convincing letters that push you toward a third-party payment platform. Once you scan the QR code or click the link, you’re taken to a payment page that has nothing to do with the UK government. And once you pay? The scammers vanish with your money.

Red Flags to Watch Out For

Not sure if a letter is fake? Here are signs that should raise concern:

✅ Unexpected Payment Requests: Especially those that appear shortly after your company is formed.

✅ Vague Descriptions: Phrases like “legal publication fee” or “company listing services” are not standard requirements.

✅ Non-Government Domains: Anything other than GOV.UK should make you cautious.

✅ Pressure Language: Warnings like “failure to pay may affect your registration status” are often scare tactics.

✅ Imperfect Branding: Slight differences in logo design, font, or colour that don’t match official Companies House correspondence.

What To Do If You Receive a Fake Companies House Letter

Do not pay. Don’t scan the QR code or visit the website.

Do not share the letter with others who might act on it.

Shred or securely discard the letter after reporting.

Ask for help. If you’re unsure whether a letter is genuine, consult your accountant or contact a trusted advisor.

At felixAccountants, we frequently review correspondence on behalf of our clients to protect them from scams like this. Send us a copy — we’re happy to verify it.

How to Help Others Stay Safe

If you work with clients, colleagues, or team members who are also business owners, share this article with them. Better still, brief your internal team to:

Stay alert for suspicious letters and emails.

Maintain a list of official contacts and procedures for post-incorporation communication.

Educate new hires and junior staff about these scams — especially those handling mail or admin duties.

Remember: awareness is protection. Scammers rely on silence and confusion. The more people know, the fewer people fall for it.

FAQs About Fake Companies House Letters

❓ Are Companies House letters ever sent by email or post?

Yes, Companies House does send some correspondence by post and email. However, they never ask for random “legal publication” payments or fees through third-party websites.

❓ How can I check if a Companies House letter is genuine?

Check the official GOV.UK website, or email a scanned copy to phishing@companieshouse.gov.uk. Always double-check before paying.

❓ I already paid the scam fee. What should I do?

Contact your bank immediately. Then report the fraud to Action Fraud (the UK’s national reporting centre for fraud and cybercrime).

❓ Can my company be deregistered for not paying?

No. These scams have no legal authority. Your registration status with Companies House will not be affected by ignoring fraudulent letters.

❓ How often do these scams occur?

Unfortunately, they are becoming more common — especially targeting newly formed companies. Scammers know new businesses are less familiar with post-incorporation requirements.

If you’re unsure about a suspicious letter, don’t risk it — ask for help. Staying informed is your first line of defence.

When a loved one passes away, managing their estate can feel overwhelming. The probate process—used to legally administer the estate—often raises the most questions. Chief among them is: Discover How Long Probate in the UK takes?

The answer depends on many factors, including the complexity of the estate, the presence of a valid will, tax issues, and how quickly documents are gathered and submitted. While simple cases may conclude within a few months, others can stretch over a year.

Probate in the UK generally takes 6 to 12 months for simple estates. However, larger or disputed estates can take significantly longer. Since January 2025, the UK Probate Registry has improved processing speeds for straightforward applications—but delays remain common.

Yes—but not for everyone. In July 2024, the average probate processing time was 9.3 weeks, an improvement from 14 weeks in July 2023. For simple wills, probate grants now take 4 to 8 weeks, down from the previous 16-week average.

However, estates involving international elements or significant assets still experience delays of 16–20 weeks or more, especially where inheritance tax (IHT) is involved.

Step-by-Step: The UK Probate Process in 2025

Here’s a simplified breakdown of the probate process, from gathering paperwork to final distribution of assets:

Step

Action

Time Frame

1

Gather documents & assess estate value

4–8 weeks

2

Submit inheritance tax forms to HMRC (if needed)

1–2 weeks

3

Wait for HMRC response & tax reference codes

4–6 weeks

4

Complete & submit probate application

1–2 weeks

5

Wait for Grant of Probate or Letters of Administration

8–16 weeks

6

Collect assets, pay debts, and distribute estate

6–12 months

Key Stages in More Detail

1. Valuation of Assets

Before applying for probate, the executor must identify and value all estate assets—bank accounts, properties, pensions, shares, and personal items. This step forms the basis of inheritance tax calculations.

2. Inheritance Tax Submission

If the estate exceeds the tax-free threshold (£325,000 as of 2025), IHT must be reported and paid—often before probate is granted. Estates eligible for reliefs (e.g., spousal or business relief) may reduce this burden.

3. Applying for the Grant of Probate

This legal document allows executors or personal representatives to access and manage the deceased’s estate. Without it, banks and institutions won’t release funds.

4. Debt Repayment

All outstanding debts—including credit cards, loans, and final utility bills—must be paid before distributing assets to beneficiaries.

5. Distributing the Estate

Once liabilities are settled, the remaining estate is distributed per the will (or under intestacy rules if no will exists). This can be straightforward or complex, depending on the number and location of beneficiaries.

probate in the UK

Factors That Can Delay Probate

Several issues can slow down probate processing:

Missing or unclear wills

Overseas property or beneficiaries

Disputes between heirs

Inheritance tax complications

Lost or delayed paperwork

Court backlogs

Taking steps early—like professional estate planning or will registration—can help your loved ones avoid unnecessary delays.

FAQs: UK Probate Process in 2025

1. How long does probate take in the UK if there’s a will?

For simple estates with a will, probate can be completed in 6–9 months, assuming no disputes or inheritance tax complications.

2. Does probate take longer without a will?

Yes. When no will exists (intestacy), the estate must follow statutory distribution rules. This adds complexity and can extend the process to 9–12 months or more.

3. What’s the fastest probate can be completed?

In rare, straightforward cases—especially where no tax is due—probate may complete in as little as 2–3 months. However, this is not the norm.

4. What causes delays in probate?

Common causes include tax issues, missing documents, property sales, legal disputes, and delays from HMRC or the Probate Registry.

5. Can I speed up the probate process?

You can help by gathering all required documents early, submitting tax forms promptly, and seeking professional advice. Avoiding disputes is also key.

Patience with Preparation Saves Time

Probate is rarely fast, but it’s often predictable. Knowing what to expect—and preparing early—can save months of delay. Whether you’re an executor handling probate now or planning ahead for your own estate, understanding the 2025 process helps protect your time, money, and peace of mind.

If the estate is small and simple, probate may only take a few months. But if the estate is large, complex, or disputed, expect a longer journey. Be informed, stay organized, and don’t hesitate to get professional guidance.

Land and Buildings Transaction Tax (LBTT), introduced on April 1, 2015, is a tax levied on property transactions in Scotland. Among the various reliefs available, Multiple Dwelling Relief (MDR) stands out as a significant mechanism designed to reduce the tax burden for purchasers acquiring multiple dwellings in a single or a series of linked transactions, ensuring they don’t pay disproportionate tax compared to purchasing a single property.

LBTT replaced the UK Stamp Duty Land Tax (SDLT) for Scottish properties. For residential properties, LBTT is charged on properties with a value over the threshold of £145,000. Above this amount, increasing tax rates apply to different portions of the property value, with higher rates for more expensive properties.

These thresholds are designed to ensure fairness, with lower-value transactions often exempt from tax, while higher-value properties contribute progressively more. However, for transactions valued above the threshold, LBTT also provides various reliefs subject to different conditions. Among the various reliefs available, Multiple Dwelling Relief (MDR) stands out as a significant mechanism designed to reduce the tax burden for purchasers acquiring multiple dwellings in a single or a series of linked transactions, ensuring they don’t pay disproportionate tax compared to purchasing a single property.

Multiple Dwelling Relief

Although MDR has been abolished in England and Northern Ireland for transactions completed or substantially performed after 1 June 2024, the relief remains applicable in Wales and Scotland. This guide provides a detailed discussion of MDR in Scotland.

If a MDR claim is successful under the LBTT, the tax liability is reduced by calculating the tax based on the average value of the dwellings purchased rather than the total consideration. MDR can lead to substantial tax savings, particularly in transactions involving high-value properties. MDR is particularly beneficial for property investors, developers, and individuals purchasing multiple residential units, such as flats in a block or houses in a development.

However, the relief is subject to specific conditions, requires careful calculation and may be withdrawn under certain circumstances. As such, it is recommended to consult with a professional to ensure an accurate assessment and avoid either overpayment of LBTT or overestimation of the relief.

What is Multiple Dwellings Relief?

The provisions regarding MDR are provided under Schedule 5 of the Land and Buildings Transaction Tax (Scotland) Act 2013 (the “Act”).

At its core, MDR is rooted in the principle of preventing disproportionate taxation that would arise from treating the purchase of multiple dwellings as a single, large-value transaction. Because LBTT is charged on a slab basis, without MDR, buyers engaging in such transactions would face significantly higher LBTT rates than those purchasing individual properties. This punitive effect could stifle investment in the Scottish housing market, discourage the development of multi-dwelling properties, and ultimately impede the efficient functioning of the property sector.

Multiple Dwelling Relief

MDR, therefore, serves as a vital instrument in fostering a balanced and equitable tax regime, one that acknowledges the distinct nature of multiple dwelling acquisitions.

The relief is available when two or more dwellings are purchased as part of a single transaction or a series of linked transactions. The LBTT is then calculated based on the average price per dwelling, multiplied by the number of dwellings, subject to a minimum tax amount. This method usually results in a lower overall tax bill compared to calculating the tax on the total consideration without relief.

To qualify for MDR in Scotland, the following conditions must be met:

The transaction must involve two or more dwellings.

The dwellings must be separate and self-contained.

The transaction can be a single purchase or a series of linked transactions.

It is important to determine whether each unit qualifies as a “dwelling.” A dwelling is typically defined as a building or part of a building used or suitable for use as a residential property.

How to Calculate Multiple Dwellings Relief

The basic steps for calculating MDR are:

Divide the total purchase price by the number of dwellings to get the average price per dwelling.

Apply the LBTT rates to the average price to calculate the tax for a single dwelling.

Multiply the single dwelling tax by the number of dwellings.

Ensure that the final amount is not less than the minimum tax threshold (£10 per dwelling).

This calculation often results in significant tax savings, especially in high-value multi-unit transactions.

Multiple Dwelling Relief

Practical Example

Suppose an investor purchases four flats in a block for a total price of £800,000. Without MDR, LBTT would be calculated on the full amount, attracting a higher tax bracket. With MDR:

Average price per dwelling = £800,000 / 4 = £200,000

LBTT on £200,000 (per dwelling) might be, for example, £7,600

Total LBTT = £7,600 x 4 = £30,400

Without MDR, tax on £800,000 might be closer to £40,000+, depending on rates. Thus, MDR saves the buyer nearly £10,000.

How to Claim Multiple Dwellings Relief

MDR must be claimed in the LBTT return submitted to Revenue Scotland. If you are amending a previous return, a revised return must be submitted within 12 months of the filing date. Supporting documents may be required to substantiate the claim.

It is advisable to work with a tax adviser or property accountant to ensure that all the qualifying conditions are met and the calculation is correct

Common Mistakes to Avoid

Incorrect classification of dwellings: Not all units may meet the definition of a “dwelling.”

Failure to link transactions: Related purchases not reported as linked may disqualify the claim.

Underestimating tax liability: If MDR is withdrawn later, interest and penalties may apply.

Missing the deadline: Claims must be made in the original return or through an amendment within the statutory period.

Multiple Dwellings Relief under LBTT continues to be a valuable tax-saving opportunity for property investors and developers in Scotland. Understanding the rules, eligibility, and how to correctly calculate and claim MDR can lead to substantial savings. However, the complexity of the rules means professional advice is crucial.

UK Property Accountants can guide you through the MDR process to ensure compliance and maximize relief. Reach out today to learn how we can support your property transactions in Scotland.

FAQs: Multiple Dwellings Relief (MDR) Under LBTT

What is Multiple Dwellings Relief (MDR) under LBTT?

MDR is a relief available under Scotland’s LBTT that reduces tax liability when purchasing two or more residential properties in a single or linked transaction.

Who qualifies for MDR in Scotland?

Anyone purchasing two or more separate dwellings in a single or linked transaction may qualify, provided the properties are suitable for residential use.

How do I calculate LBTT with Multiple Dwellings Relief?

Divide the total price by the number of dwellings to get an average, apply LBTT rates to that average, then multiply by the number of dwellings.

Can I claim MDR on linked transactions?

Yes. Linked transactions are treated as a single transaction for MDR, provided they form part of a single arrangement or deal.

What properties are considered “dwellings” for MDR?

Properties that are self-contained and suitable for use as a residence, such as houses, flats, and maisonettes.

Is MDR available if I’m buying both residential and non-residential properties?

Yes, MDR can still apply. The relief is based on the portion of the consideration attributed to dwellings only.

Can I claim MDR if I’ve already claimed other reliefs like Group Relief?

No, MDR cannot be claimed if certain other reliefs like Group Relief or Charities Relief are already claimed.

How do I claim MDR on my LBTT return?

You must include the claim in your LBTT return to Revenue Scotland. If needed, amend the return within 12 months to include the relief.

What happens if my MDR claim is incorrect?

An incorrect claim may result in withdrawal of the relief, along with penalties and interest on the underpaid LBTT.

Is MDR still available in 2025 for property purchases in Scotland?

Yes, MDR remains in effect in Scotland (and Wales) as of 2025, though it has been abolished in England and Northern Ireland.

Can I amend a previous LBTT return to include MDR?

Yes. You can amend a return within 12 months from the filing date to claim MDR, provided you meet the criteria.

Does MDR apply to leasehold transactions?

No. MDR is not available for transactions classified as leases for LBTT purposes.

What’s the difference between MDR and other LBTT reliefs?

MDR specifically targets transactions involving multiple dwellings. Other reliefs like Group or Charities Relief have different eligibility rules.

How much can I save using Multiple Dwellings Relief?

Savings vary but can be thousands of pounds. The more high-value dwellings involved, the greater the potential tax savings.

Should I consult a property accountant before claiming MDR?

Yes. MDR rules are complex, and professional advice ensures accurate claims and maximum tax savings.

Chancellor Rachel Reeves has unveiled the Spring Statement 2025 introducing a range of measures aimed at boosting the UK economy, driving growth, and ensuring fiscal stability. However, her proposals faced strong opposition, with Shadow Chancellor Mel Stride highlighting potential risks and criticizing the government’s handling of economic policies.

Economic Growth Forecast

Reeves addressed the downgraded UK growth forecast by the Office for Budget Responsibility (OBR), which was reduced from 2% to 1% for 2025. Growth projections for subsequent years show a slow recovery:

Spring Statement 2025

2026: 1.9%

2027: 1.8%

2028: 1.7%

2029: 1.8%

Despite external global challenges, Reeves reassured that government investments in infrastructure and innovation would support long-term growth. However, Stride criticized these measures, arguing that the UK’s economic slowdown was the result of the government’s own policies.

Capital Spending & Economic Expansion

To stimulate economic expansion, Reeves announced a £2 billion annual increase in capital spending aimed at funding key infrastructure and defense projects. These investments are expected to:

Create job opportunities in skilled sectors

Strengthen defense capabilities

Boost advanced manufacturing hubs in Glasgow, Derby, and Newport

Stride argued that while capital spending is necessary, it does not compensate for past economic mismanagement.

Housing Growth & Planning Reforms

The Chancellor introduced planning reforms to accelerate housing development, targeting the construction of 1.3 million new homes over five years. These changes aim to address the UK’s ongoing housing crisis by streamlining bureaucratic hurdles.

Stride, however, questioned whether these reforms would be effective enough to tackle housing shortages, pointing out past failures in increasing affordable housing supply.

Inflation Target & Fiscal Stability Spring Statement 2025

Reeves reaffirmed the government’s commitment to achieving the 2% inflation target by 2027. Although inflation recently dropped to 2.8%, it remains above the Bank of England’s preferred level.

Stride countered that inflation under Reeves’ leadership was double previous forecasts, blaming government policies for persistent price pressures affecting households and businesses.

Public Sector Reforms & Efficiency

To improve efficiency and cut waste, Reeves announced a £3.25 billion Transformation Fund and set a goal of saving £3.5 billion annually by 2029/30. These savings will be achieved through:

Voluntary exit schemes for public sector workers

Civil service workforce reductions

AI and digital transformation in key services

Welfare Cuts & Budget Adjustments

The government plans to reduce welfare spending, including cuts to Universal Credit and freezes on allowances for new claimants. While Reeves defended these cuts as necessary for long-term sustainability, Labour MPs expressed concerns about the impact on vulnerable citizens.

Stride strongly opposed these measures, warning that they could worsen poverty levels and disproportionately affect low-income families.

Reduction in Foreign Aid Spending

The Chancellor announced a reduction in foreign aid spending to 0.3% of gross national income, saving £2.6 billion by 2029/30. Critics argue that this move weakens the UK’s global leadership and diplomatic standing, but Reeves justified it as a necessary adjustment given domestic fiscal constraints.

Skills Development & Workforce Training

To address labor shortages, the government is investing £600 million in construction worker training programs, targeting the upskilling of 60,000 workers. This investment aims to strengthen technical and vocational education, ensuring a skilled workforce for critical sectors.

Crackdown on Tax Evasion

The government plans to increase tax fraud prosecutions by 20% annually, expecting to generate £1 billion in additional revenue. This move is part of a broader initiative to improve tax fairness and compliance.

Stride criticized this effort, arguing that without stronger enforcement mechanisms, the crackdown may not achieve its desired financial impact.

Household Income & Economic Outlook

According to the OBR, real household disposable income is now projected to grow at nearly twice the anticipated rate, meaning the average household could be £500 better off under current policies.

Fiscal Predictions from the OBR

The OBR report confirmed that the Chancellor has restored some fiscal headroom, allowing for possible tax cuts or spending increases while still adhering to fiscal rules. However, it warned that escalating global trade disputes could negatively impact future economic stability.

Despite Reeves’ efforts to present a comprehensive economic recovery plan, opposition leaders remain unconvinced. With ongoing debates on inflation, welfare reforms, and tax policies, the Spring Statement 2025 has set the stage for continued political and economic discussions in the UK.

FAQs of Spring Statement 2025

1. What were the key highlights of the Spring Statement 2025?

The statement covered economic growth forecasts, capital spending, housing development, public sector reforms, welfare cuts, and tax policies.

2. How will the UK government tackle inflation?

The government aims to achieve a 2% inflation target by 2027 through monetary policies and fiscal adjustments.

3. What changes were announced for welfare spending?

The government plans to cut Universal Credit benefits and freeze allowances for new claimants.

4. How will the tax system change under this statement?

The government is cracking down on tax fraud with a 20% increase in annual prosecutions, expecting to raise £1 billion in revenue.

5. What were the opposition’s main criticisms?

Shadow Chancellor Mel Stride argued that economic growth had been halved, inflation remained too high, and welfare cuts would hurt vulnerable citizens.

As a property investor in the UK, rental income taxes are a significant factor to consider when managing your investments. The tax you pay on your rental income can affect your profitability, so understanding how it works is essential. This article will cover everything you need to know about rental income taxes, including how to calculate them, what expenses you can deduct, and strategies to reduce your tax liability.

1. How Is Rental Income Taxed?

In the UK, any income you earn from renting out property is subject to income tax. The amount you pay depends on your total income for the year and your tax band.

Tax Rates:

Basic Rate (20%): Income up to £50,270.

Higher Rate (40%): Income between £50,271 and £125,140.

Additional Rate (45%): Income over £125,140.

You will be taxed based on your net rental income, which is your total rental income minus any allowable expenses (discussed in Section 3).

Example:

If you earn £15,000 in rental income and spend £5,000 on allowable expenses, your taxable rental income is £10,000. If you’re in the basic tax band, you’ll pay 20% of that, or £2,000 in tax.

2. Filing Your Rental Income Tax

If you’re a property investor, you’ll need to report your rental income on a Self Assessment tax return. This is typically due by 31 January each year for the previous tax year (which runs from 6 April to 5 April).

2. Keep detailed records of your rental income and expenses.

3. Fill in the property section of the Self Assessment form.

4. Submit your return and pay any taxes due by the deadline.

Failure to submit on time can result in penalties, so it’s essential to stay on top of deadlines.

3. Allowable Expenses: What Can You Deduct?

To calculate your net rental income, you can deduct certain allowable expenses from your total rental income. These are costs incurred from managing and maintaining the rental property. Common allowable expenses include:

Mortgage Interest: You can claim 20% of the mortgage interest as a tax credit (due to recent changes in tax relief).

Repairs and Maintenance: Costs of fixing damage or wear and tear, such as repairing a roof or fixing a boiler, are deductible.

Letting Agent Fees: Fees paid to property managers or letting agents can be deducted.

Insurance: Premiums for landlord insurance policies covering buildings, contents, or liability.

Council Tax and Utility Bills (if you, as the landlord, are responsible for paying them).

Legal and Professional Fees: Costs for legal advice or accountancy services related to your rental property.

Advertising Costs: Any money spent marketing the property to find tenants.

Non-Deductible Expenses:

You can’t deduct expenses related to improvements or renovations. For example, replacing a kitchen or adding an extension would be considered a capital expense, not an allowable one.

Example:

If you earn £12,000 in rental income and have £6,000 in allowable expenses, you would only be taxed on the remaining £6,000.

If you decide to sell your rental property, you may have to pay Capital Gains Tax (CGT) on the profit you make from the sale. This tax applies to the difference between the purchase price and the sale price, minus any allowable expenses for improvements or legal fees.

CGT Rates for Property:

18% for basic-rate taxpayers.

28% for higher-rate taxpayers.

You are entitled to an annual CGT allowance of £6,000 (2024). This means you don’t pay tax on the first £6,000 of any gains.

Example:

If you bought a property for £200,000 and sell it for £250,000, your gain is £50,000. After applying the £6,000 allowance, you would be taxed on £44,000.

5. Strategies to Reduce Your Tax Liability

Reducing your tax liability as a property investor is possible through careful planning. Here are a few strategies you can use:

a. Claim All Available Expenses

Maximize your deductions by keeping thorough records of all allowable expenses. This reduces your taxable rental income, lowering your tax bill.

b. Use a Limited Company

Many investors are choosing to purchase property through a limited company. Corporate tax rates (currently 19%) are lower than higher-rate income tax, and mortgage interest can still be deducted in full. However, there are additional costs for setting up and maintaining a company, so it’s not suitable for everyone.

c. Spread Ownership Between Spouses

If your spouse pays tax at a lower rate, consider transferring part of the ownership of the property to them. This spreads the rental income and reduces the overall tax bill.

Example:

If you’re a higher-rate taxpayer and your spouse is in the basic tax band, transferring 50% of the property to them could mean they pay only 20% on their share of the rental income, instead of 40%.

d. Capital Allowances for Furnished Properties

If you let out a furnished property, you may be eligible for capital allowances. This allows you to claim for items such as furniture, appliances, and fixtures.

e. Rent a Room Scheme

If you rent out part of your home, you can earn up to £7,500 tax-free under the Rent a Room Scheme. This only applies if you’re renting out furnished rooms in your main residence, not a separate rental property.

6. What Happens If You Don’t Pay Rental Income Tax?

Failing to declare your rental income can lead to penalties from HMRC. If you’re caught under-reporting or failing to report your income, you could face:

Fines of up to 100% of the unpaid tax.

Interest on the unpaid amount.

Criminal charges in severe cases.

To avoid these penalties, make sure you file your tax return on time and declare all rental income accurately.

As a property investor in the UK, rental income tax is an unavoidable part of owning property. Understanding how taxes work and taking full advantage of allowable expenses and tax-saving strategies can help you maximize your returns. Whether you’re managing a buy-to-let or considering selling a property, it’s essential to plan your tax strategy carefully.

If you’re unsure about the best approach, consulting with a tax professional can help you navigate the complexities of the UK tax system and reduce your overall liability.

FAQs

How do I calculate my rental income tax?

Subtract allowable expenses from your total rental income to get your taxable rental income. Then, apply the relevant tax rate based on your income band.

Can I deduct mortgage payments from rental income?

You can deduct the interest portion of your mortgage payments, but the principal repayment isn’t deductible.

Is renting out my property through a limited company worth it?

It depends on your personal circumstances. For high earners, it could save money on taxes, but it comes with additional administrative costs.

What happens if I don’t file my rental income tax return on time?

HMRC can fine you, and you may also owe interest on any unpaid taxes.

Property Allowance

The UK offers a property allowance that allows individuals to earn up to £1,000 per tax year from property rental income without paying tax. If your rental income exceeds this allowance, you can choose to deduct the £1,000 instead of actual expenses when calculating your taxable profit. This can be beneficial for landlords with minimal expenses. gov.uk

Non-Resident Landlords

If you reside outside the UK but receive rental income from a UK property, you’re still liable to pay UK income tax on that income. The Non-Resident Landlord Scheme requires either your tenant or letting agent to deduct basic rate tax from your rental income before it’s paid to you, unless you have received approval from HMRC to receive the income gross. gov.uk

Record-Keeping and Reporting

Maintaining accurate records of all rental income and expenses is essential. Landlords are required to report rental income to HMRC through the Self Assessment tax return system. Proper documentation supports the figures reported and ensures compliance, helping to avoid potential penalties for misreporting. ukpropertyaccountants.co.uk

Capital Allowances

While traditional buy-to-let residential properties have limited scope for capital allowances, landlords of furnished holiday lettings (FHL) can claim capital allowances on items such as furniture, equipment, and fixtures. This can significantly reduce taxable profits. However, it’s important to note that upcoming tax changes in 2025 may affect the benefits associated with FHLs. ft.com

Tax Rates and Personal Allowance in the UK

The UK income tax system is progressive, with rates increasing with higher income levels. As of the 2024/25 tax year, the personal allowance is £12,570, meaning you don’t pay tax on the first £12,570 of your income. However, this allowance decreases by £1 for every £2 of income over £100,000, and is completely removed once your income exceeds £125,140. gosimpletax.com

Penalties for Non-Compliance

Failing to accurately report rental income or missing tax return deadlines can result in significant penalties. Common mistakes include not registering for Self Assessment on time, failing to pay the tax bill promptly, and simple errors such as typos in personal information or the unique tax reference (UTR). It’s crucial to file early and accurately to avoid interest accruals and penalties. thetimes.co.uk

By staying informed about these aspects of rental income taxation, you can better manage your property investments and ensure compliance with HMRC regulations

UK Property Rental Income & Tax FAQs

How is property rental income taxed in the UK? Rental income is taxed as part of your overall income and is subject to Income Tax at 20% (basic rate), 40% (higher rate), or 45% (additional rate) depending on your total earnings. You can deduct allowable expenses before calculating taxable profit.

Do foreign investors have to pay tax in the UK on rental income? Yes, non-residents must pay UK Income Tax on rental income from UK properties. They are usually taxed at the same rates as UK residents but may need to register under the Non-Resident Landlord Scheme (NRLS).

Do renters pay property tax in the UK? Renters do not pay property tax, but they are responsible for Council Tax, unless the landlord includes it in the rent. Council Tax varies by local authority and property valuation band.

Do I pay tax on rental income if I have a mortgage in the UK? Yes, rental income is taxable even if you have a mortgage. However, landlords can no longer deduct mortgage interest directly but receive a 20% tax credit on mortgage interest payments.

How can I avoid paying tax on rental income in the UK? You cannot avoid tax, but you can reduce it by deducting allowable expenses (repairs, insurance, property management fees) and using tax-efficient ownership structures like joint ownership or holding property through a limited company.

What is the tax rate on rental income for non-residents in the UK? Non-residents are taxed at the same rates as UK residents (20%, 40%, or 45%) but may be eligible for double taxation relief if their home country has a tax treaty with the UK.

What is the capital gains tax on rental property in the UK? When selling a rental property, Capital Gains Tax (CGT) applies:

18% for basic rate taxpayers

24% for higher and additional rate taxpayers (was 28% before April 2024) A £6,000 annual CGT allowance (2024/25) applies before tax is due.

Can I put rental income into a pension in the UK? Yes, you can contribute rental income into a pension (like a SIPP), but tax relief is available only up to 100% of your annual earned income (not passive income like rent).

Which countries have a double taxation agreement with the UK? The UK has double taxation treaties with over 130 countries, including the USA, Canada, Australia, France, Germany, China, and India. These treaties prevent taxpayers from being taxed twice on the same income.

Is there tax on UK residential property for non-residents? Yes, non-residents must pay Income Tax on rental income and Capital Gains Tax (CGT) on property sales. They may also be subject to Stamp Duty Land Tax (SDLT) and Annual Tax on Enveloped Dwellings (ATED) if owning through a company.

Can foreigners rent out property in the UK? Yes, foreigners can rent out property in the UK, but they must comply with UK tax laws and may need to register under the Non-Resident Landlord Scheme (NRLS) if living abroad.

Are utilities included in rent in the UK? It depends on the tenancy agreement. Some landlords include utilities (gas, electricity, water, internet, council tax) in the rent, while others require tenants to pay separately.

What is the new landlord tax in the UK? Recent changes include:

Mortgage interest tax relief limited to 20%

Higher CGT rates (was 28%, now 24% for landlords)

Making Tax Digital (MTD) for landlords earning over £50,000 (from April 2026)

Is rent taxable if my boyfriend pays me in the UK? Yes, rental income is taxable regardless of who pays it. However, if you live in the property and share costs, it may not be classified as rental income.

What is the renters’ tax credit in the UK? There is no general renters’ tax credit in the UK, but housing benefits or Universal Credit may assist eligible tenants. Scotland has proposed a renters’ tax relief, but it is not yet law.

What expenses can you claim for rental property in the UK? Landlords can deduct expenses like:

Everyone wants to keep more of their hard-earned money, and one of the best ways to do this is by maximizing your personal tax-free allowance. Understanding how this allowance works and utilizing strategic tax planning can help reduce your taxable income, ultimately saving you money.

The personal tax-free allowance is the amount of income you can earn before you start paying income tax. The threshold can change annually, so it’s important to stay updated on the current limits. If your income exceeds this amount, only the excess is subject to tax.

Tax-Free Allowance

Use Salary Sacrifice Schemes

A salary sacrifice scheme allows you to exchange part of your salary for non-cash benefits such as pension contributions, childcare vouchers, or cycle-to-work programs. Since these benefits are often tax-free, they effectively reduce your taxable income while providing financial advantages.

Contribute to a Pension

Contributing to a pension is an excellent way to reduce your taxable income while securing your financial future. Contributions to a workplace or personal pension scheme can lower your income tax liability while growing your retirement savings.

Utilize Marriage Allowance

If you’re married or in a civil partnership and one partner earns below the personal allowance threshold, they can transfer a portion of their unused allowance to the higher-earning partner. This can reduce the tax bill for the couple as a whole.

Tax-Free Allowance

Take Advantage of ISA Accounts Tax-Free Allowance

Individual Savings Accounts (ISAs) allow you to earn interest, dividends, or capital gains tax-free. By utilizing your annual ISA allowance, you can grow your savings while avoiding unnecessary tax charges.

Claim Allowable Work and Business Expenses

If you’re self-employed or work from home, you may be eligible to deduct certain expenses from your taxable income, such as:

Office supplies and equipment

Business travel and mileage

Professional training and development

Home office expenses

Spread Income Between Family Members

If you own a business or have investments, consider distributing income among family members who have lower taxable income. This can help utilize their personal allowance while reducing the overall family tax burden.

Make Charitable Donations of Tax-Free Allowance

Donating to registered charities through Gift Aid allows you to reduce your taxable income. Higher-rate taxpayers can claim additional tax relief on donations, making charitable giving both impactful and tax-efficient.

Tax-Free Allowance

Check for Additional Tax Reliefs

There are various tax reliefs available depending on your situation, including:

Blind Person’s Allowance

Trading Allowance (for small business income)

Rent-a-Room Relief (if you rent out part of your home)

If you plan to sell investments, property, or other assets, ensure you use your Capital Gains Tax (CGT) allowance wisely. Spreading asset sales across multiple tax years can help minimize CGT liability.

FAQs of Tax-Free Allowance

What is the personal tax-free allowance?

The personal tax-free allowance is the amount of income you can earn before paying income tax. The specific amount varies each tax year, so it’s essential to check current limits.

How can I reduce my taxable income?

You can reduce your taxable income by making pension contributions, using salary sacrifice schemes, claiming allowable business expenses, and utilizing available tax reliefs such as Marriage Allowance and ISAs.

Does salary sacrifice affect my personal allowance?

Yes, salary sacrifice reduces your taxable income, meaning you may be able to keep more earnings within your personal tax-free allowance.

Can I transfer my personal allowance to my spouse?

Yes, under the Marriage Allowance scheme, a lower-earning spouse can transfer up to 10% of their personal allowance to their partner, reducing the couple’s overall tax bill.

What happens if my income exceeds the personal allowance?

Any income above the personal allowance is subject to income tax at the applicable rate based on your total earnings. Proper tax planning can help minimize your liability.

By understanding and strategically managing your personal tax-free allowance, you can legally minimize your tax liability and keep more of your earnings. Whether through pension contributions, tax-efficient savings, or work-related deductions, smart tax planning can significantly impact your financial well-being.

For personalized tax advice, consult a tax professional to ensure you’re making the most of your allowances and exemptions! click here for more

As the tax deadline approaches, small business owners must take advantage of every possible deduction to reduce their taxable income. Even in the final days before filing, there are strategic moves you can make to maximize savings. This checklist will help you identify last-minute tax saving opportunities to lower your tax bill legally and efficiently.

Business expenses that qualify as deductions can significantly reduce your taxable income. Review your records and ensure you claim all eligible expenses, including:

Office supplies and equipment

Marketing and advertising costs

Professional fees (legal, accounting, etc.)

Business travel expenses

Home office deduction (if applicable)

Last-Minute Tax Saving

Contribute to Retirement Accounts

If you haven’t maxed out contributions to a retirement plan, now is the time. Contributions to plans like a SEP IRA, Solo 401(k), or SIMPLE IRA can lower your taxable income while securing your financial future. Some plans allow contributions up to the tax filing deadline.

Defer Income and Accelerate Expenses

Delaying income and accelerating expenses can help shift taxable income to the next year. Consider:

Deferring invoices until after year-end (if using cash accounting)

Prepaying business expenses such as rent, insurance, or subscriptions

Purchasing necessary equipment or supplies before the deadline

Last-Minute Tax Saving

write Off Bad Debts

If you have outstanding invoices that are unlikely to be paid, consider writing them off as bad debt expenses. This reduces your taxable income and helps clean up your financial records.

Take Advantage of Section 179 and Bonus Depreciation

If you’ve purchased equipment, machinery, or software, you may be eligible for immediate deductions under Section 179 or bonus depreciation. These tax provisions allow businesses to deduct the full cost of qualifying assets rather than depreciating them over time.

Last-Minute Tax Saving

Claim Available Tax Credits

Tax credits directly reduce the amount of taxes owed, making them highly valuable. Common small business tax credits include:

R&D Tax Credit – For businesses investing in research and development

Work Opportunity Tax Credit (WOTC) – For hiring employees from certain target groups

Small Business Health Care Tax Credit – For businesses offering health insurance to employees

Review Payroll and Contractor Payments

Ensure all payroll taxes, employee wages, and contractor payments are correctly recorded. Issue 1099 forms for independent contractors and verify that payroll tax deposits are up to date to avoid penalties.

Check Your Estimated Tax Payments

If you’ve underpaid estimated taxes throughout the year, making a final estimated payment can help reduce penalties. Review your total income and adjust your last quarterly payment if needed.

Organize and Update Financial Records of last-minute tax saving

Having accurate records is crucial for tax filing and potential audits. Before submitting your tax return:

Reconcile bank and credit card statements

Categorize all income and expenses correctly

Ensure all receipts and invoices are properly stored

Last-Minute Tax Saving

Consult a Tax Professional

Tax laws change frequently, and missing out on deductions or credits can be costly. A tax professional can help identify additional savings and ensure compliance with IRS regulations.

FAQs of Last-Minute Tax Saving Checklist for Small Business Owners

How to pay less tax as a business owner in the UK?

Claim all allowable expenses – Office costs, travel expenses, utilities, insurance, and more.

Use tax-efficient business structures – Consider whether a sole trader, partnership, or limited company is best for your situation.

Pay yourself tax-efficiently – Use a combination of salary and dividends.

Take advantage of capital allowances – Claim deductions for business equipment, vehicles, and machinery.

Utilize pension contributions – Contributions to a pension scheme are tax-deductible.

Use VAT schemes – Register for VAT if beneficial, or use the Flat Rate VAT Scheme.

Employ family members – Paying family members for genuine work can reduce taxable profits.

How to avoid 40% tax as a self-employed person in the UK?

Keep your income under £50,270 to stay in the basic rate tax band (20%).

Make pension contributions to reduce taxable income.

Use tax-deductible expenses to lower profits.

Split income with a spouse (if they are in a lower tax bracket).

Consider incorporating as a limited company – You may pay yourself via dividends, which are taxed at lower rates.

How to pay the least amount of taxes as a small business owner?

Optimize expenses – Claim everything you’re entitled to.

Structure your business wisely – A limited company can be more tax-efficient than a sole trader.

Make use of allowances – Personal allowance, capital allowances, and tax-free dividends.

Hire an accountant – A professional can help you save money legally.

What is 100% tax deductible in the UK?

Office rent and utilities

Employee wages

Business insurance

Professional fees (accountants, solicitors)

Marketing and advertising

Travel expenses (business-related)

Training courses related to your business

Work equipment and IT expenses

How can I legally reduce my tax in the UK?

Use tax reliefs like the Annual Investment Allowance (AIA) for equipment.

Maximise expenses – Claim all business-related costs.

Save for retirement with a pension.

Take dividends instead of salary for lower tax rates.

What is the most tax-efficient way to pay yourself in the UK?

Take a small salary (around £12,570) to use your personal allowance.

Pay the rest in dividends, which have lower tax rates than salary.

Use pension contributions for tax efficiency.

Do I need to do a tax return if I earn under £10,000 in the UK?

Yes, if:

You’re self-employed and earn over £1,000.

You have untaxed income from property, investments, or freelancing.

Who is exempt from income tax in the UK?

People earning under £12,570 per year (Personal Allowance).

Certain state pensioners.

Some disability benefit recipients.

How to beat the tax man?

Use all available tax reliefs and deductions.

Invest in pensions and ISAs.

Plan withdrawals and income strategically to stay within lower tax bands.

Which type of business pays the least taxes?

Limited companies often pay less tax than sole traders.

Companies under the VAT threshold (£90,000) can avoid VAT.

Businesses using R&D tax relief get tax reductions.

How to reduce self-employment tax?

Claim all allowable business expenses.

Use tax-efficient pension contributions.

Keep profits below tax threshold bands.

How do I pay the least taxes when selling my business?

Use Business Asset Disposal Relief (BADR) for 10% capital gains tax instead of 20%.

Sell in stages to manage tax liability.

Can I claim my mobile phone as a business expense in the UK?

Yes, if it’s used for business purposes. If you use it for both personal and business, you can claim the business percentage.

How much is £100,000 taxable in the UK?

First £12,570 – 0% (personal allowance)

£12,571 – £50,270 – 20% tax

£50,271 – £100,000 – 40% tax

Over £100,000 – Personal allowance reduces by £1 for every £2 earned

Can you write off a car as a business expense in the UK?

Yes, if it’s used for business. You can claim mileage allowance (45p per mile) or capital allowances for business vehicles.

How to reduce your tax bill in the UK as self-employed?

Maximise deductible expenses.

Pay into a pension.

Use VAT schemes effectively.

Plan for tax efficiency with an accountant.

How much can you earn before paying tax per month in the UK?

£12,570 per year = £1,047 per month tax-free (Personal Allowance).

For personalized tax strategies, consider consulting with an accountant before the deadline. Planning ahead will ensure a smoother tax season visit us at felixaccountants.com for more

The Annual Tax on Enveloped Dwellings (ATED) is a tax that applies to high-value residential properties owned by companies, partnerships with corporate members, or collective investment schemes in the UK. It was introduced in 2013 and mainly targets properties valued above £500,000 that are owned through a corporate structure, rather than by individuals.

A crucial part of ATED is the Valuation Rule, which determines how to assess the value of a property for tax purposes. This rule is significant because the amount of ATED tax owed depends directly on the value of the property. The following section explains the ATED valuation rules, including how property values are determined, when valuations are required, and the effect of valuations on the tax liability.

ATED: Key Considerations: Valuations

The Annual Tax on Enveloped Dwellings (ATED) tax year runs from 1 April to 31 March, and the tax return must be filed within a set period after the end of the tax year. The valuation of the property is a key factor in determining the amount of ATED annual charge payable.

The valuation rule refers to the method of determining the market value of a residential property for the purposes of ATED. The valuation is a fundamental aspect because the amount of ATED owed is based on the value of the property, and properties above a certain threshold are subject to the tax.

ATED Valuation Rules

Key Valuation Dates for ATED

The Valuation Rule is tied to specific dates that establish when and how a property should be valued for ATED purposes:

1 April 2012: This is the initial valuation date for properties that were owned on or before this date. When ATED was first introduced, the market value of these properties on 1 April 2012 determined whether the property was subject to the tax.

Acquisition Date: If the property is purchased after 1 April 2012, the valuation date becomes the date of acquisition, meaning the market value on the day the property is bought determines the ATED liability.

Five-Year Revaluation Cycle: After the initial valuation, properties must be revalued at least every five years. The most recent revaluation date was 1 April 2022, and the next revaluation date is 1 April 2027. If a property is purchased before the end of a five-year period, it must still be revalued according to the standard five-year cycle, not the remaining years. For instance, if the property is valued in 2024, the next revaluation will still occur in 2027, not 2029.

The value of the property for any chargeable period is therefore the later of:

its initial valuation date

the revaluation date

The five-year cycle ensures that the valuation reflects current market conditions and is crucial for maintaining the accuracy of tax liabilities over time.

When Revaluation Is Required

Revaluation is necessary under certain circumstances, such as:

Initial Valuation: For properties owned on 1 April 2012, or after this date, the value must be established as of the acquisition date or 1 April 2012, as applicable.

Five-Year Cycle: Properties must be revalued every five years, ensuring the tax reflects any changes in the market.

Significant Renovations or Disposals: If a property undergoes major renovations or improvements that significantly increase its value, or if a substantial portion of the property is sold or disposed of, a revaluation may be required before the five-year mark.

Major Renovations and Disposals

A substantial acquisition or disposal triggers a revaluation for ATED purposes. For example, if a property was valued at £5 million on 1 April 2012, and the owner sold part of it (like a small piece of land) for £200,000 on 30 August 2014, the revaluation would not simply be £4.8 million (the original value minus £200,000). Instead, the property would need to be revalued based on the market value of the remaining interest as of the disposal date, which could even change its value significantly.

An acquisition is considered “substantial” if the buyer pays £40,000 or more for the property or any part of it, including any linked transactions.

A disposal of part of the property (but not the whole property) is considered “substantial” if the value of the part sold is £40,000 or more.

ATED Valuation Rules

Transactions Between Connected Parties

If the transaction involves connected parties (such as family members, friends, or businesses with shared interests), special rules apply. In such cases, the market value of the property is used for ATED purposes, not just the price agreed upon between the parties. This is to prevent under-reporting of the property’s value, ensuring that the tax is based on a fair and accurate valuation.

Valuing the Property: How to Proceed

You have two options for valuing your property:

Self-Valuation: You can personally assess the value of the property, but it must reflect the market price that a willing buyer and seller would agree upon.

Professional Valuation: Hiring a professional property value is another option, which may offer more assurance regarding the accuracy of the valuation.

The key point here is that the valuation should be reasonable and justifiable. HMRC will usually accept self-valuations but may challenge them if they believe the valuation is incorrect.

FQSs

What are valuation rules?

Valuation rules are guidelines or methods used to determine the monetary value of an asset, business, or property. These rules vary depending on the purpose of the valuation, such as taxation, financial reporting, or investment analysis.

What is the purpose of ATED?

The Annual Tax on Enveloped Dwellings (ATED) is a UK tax designed to discourage companies from holding high-value residential properties. It ensures such properties are taxed appropriately when owned by corporate entities, partnerships with corporate members, or collective investment schemes.

How to avoid ATED?

To avoid ATED, property owners can:

De-envelope the property – Transfer ownership from a corporate entity to an individual.

Claim applicable reliefs – Available for rental businesses, property developers, or properties open to the public.

Ensure the property value is below £500,000 – ATED applies to properties above this threshold.

Since de-enveloping can have other tax implications, consulting a tax professional is recommended.

What is the meaning of ATED?

ATED stands for Annual Tax on Enveloped Dwellings, a tax on certain high-value UK residential properties owned by non-natural persons (e.g., companies or investment funds).

What is the formula for valuation?

Valuation formulas depend on the asset being valued. Common methods include:

Discounted Cash Flow (DCF) Analysis – Calculates the present value of expected future cash flows.

Comparable Company Analysis – Values a business based on similar companies.

Precedent Transactions – Uses past sales of similar assets to determine value.

In the context of UK taxation, Rule 2 of the valuation rules refers to specific guidelines for determining the market value of assets for tax purposes. The exact rule may vary based on the legislation being applied.

What is de-enveloping?

De-enveloping is the process of transferring ownership of a property from a corporate entity (the “envelope”) to an individual. This is often done to avoid taxes like ATED but may have other tax consequences, such as Stamp Duty or Capital Gains Tax.

What is NRCGT?

NRCGT stands for Non-Resident Capital Gains Tax. It applied to non-residents disposing of UK residential property between 6 April 2015 and 5 April 2019. From 6 April 2019, it was expanded to cover all UK land and property owned by non-residents.

Is “ated” a suffix?

Yes, “-ated” is a suffix used in English to form adjectives indicating a condition or state, such as “complicated” or “animated.”

What is the meaning of “coppy”?

“Coppy” is an old English term referring to a small coppice or thicket of trees. It is not commonly used today.

What is the meaning of “ture”?

“Ture” is not a standalone word in English but is a suffix found in nouns like “nature” and “structure.”

How much is NRCGT?

The Non-Resident Capital Gains Tax (NRCGT) rates are:

Individuals – 18% or 28%, depending on income level.

Companies – 20%.

These rates apply to gains from UK property disposals by non-residents.

What is the remittance basis?

The remittance basis is a UK tax treatment that allows non-domiciled residents to be taxed only on foreign income and gains brought (“remitted”) into the UK, instead of being taxed on worldwide income.

Am I still a UK resident if I live abroad?

UK tax residency depends on factors such as:

The number of days spent in the UK.

Ties to the UK (family, property, work).

The Statutory Residence Test (SRT) determines residency status. In some cases, you can still be considered a UK resident while living abroad.

What ends with “ated”?

Many English words end with “-ated,” such as:

Complicated

Animated

Dedicated

Isolated

Frustrated

This suffix often indicates a condition or state resulting from an action.

What is the full meaning of “ate”?

“Ate” is the past tense of the verb “eat,” meaning to have consumed food. It can also be a suffix in words like “dominate” or “activate.”

What does the stem “ate” mean?

The stem “ate” comes from Latin and often means “to cause” or “to make” in verbs like “educate” (to cause learning) or “animate” (to bring to life).

A personal tax account is an HMRC-initiated system to make the tax system in the UK more efficient and transparent. This system facilitates you to access all your tax-related personal information in one place. Through your tax account, you can solve your tax issues on time by yourself without writing or calling the HMRC. You are probably wondering, how do I set up my personal tax account?

If you have access to your personal tax account, it means you can save a great deal of your time and energy. You can manage and handle your tax matters in a much better way. The personal tax account system was started in 2015 and it has been a splendid success since then as it saves countless hours by dealing with everything online. Surely, it is for the best that you set up your personal tax account.

What Can I Do with My Personal Tax Account?

The list of services for the personal tax account is constantly expanding and growing. Therefore, you can avail of many useful financial services from your personal tax account that include:

Checking income tax code.

Finding the national insurance number.

Organising tax credits.

Claiming a tax refund.

Checking your income tax estimates.

Paying overdue taxes.

Updating or checking your marriage allowance.

Checking the latest updates on the value of the state pension.

Adding a family member or other trustworthy person to manage your account on your behalf.

Viewing your self-assessment tax calculation, which might be helpful in applying for credit.

If there is any error or miscalculation in anything like details or anything else, you can change it by yourself. This guide will help you comprehend how do I set up my personal tax account.

What are the Benefits of setting up a Personal Tax Account?

The personal tax account system is an attempt by the HMRC to make the taxation system more transparent and efficient. With the use of this taxation system, it becomes easier for you to update the HMRC about the changes to your circumstances, like getting married, having a baby, and changing your address. It enables you to change your child’s benefits circumstances, such as if the child joins or leaves education or training. If you are a parent, then you can keep track of child track credits. you can check or update the benefits you get from your work such as car insurance, or company car details.

The major benefit of the personal tax account is that everything relating to your tax affairs will be online in one place. Hence, you will not have to spend time finding out different papers to get the details of your taxes.

Also, creating your personal tax account enables you to monitor your tax-related affairs to make sure that your records are accurate and up to date.

It is less time-consuming, more transparent, less difficult, more immediate, and entirely paperless. This process does not require lengthy letters but easy texting messages or emails- so you will be doing good for the environment too. Thus, it is an ideal situation.

Certainly, it is human nature to envisage every new thing as difficult until becoming familiar with it. But setting up your personal tax account with HMRC is like something easier done than said.

Setting up a personal tax account is not time-taking or technicalities involving the job at all. According to HMRC, it should only take 5-10 minutes.

Personal Tax Account

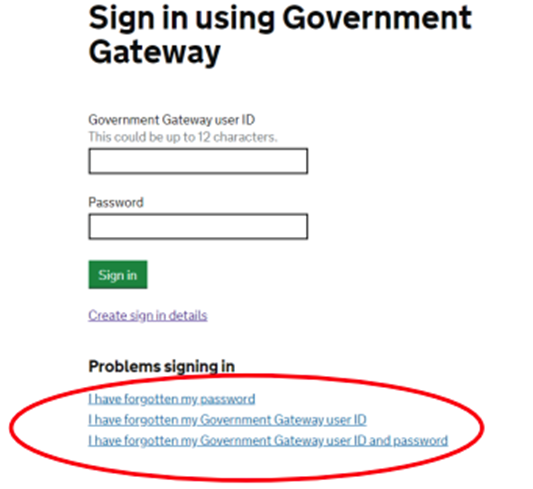

To start with, you must log in to your government gateway account.

The form online available is itself much easier to follow as it simply involves inputting your information and setting up security protocol. At this stage, the time factor entirely depends on the organization of the paperwork you start with. The more your paperwork is organized, the less time will it takes. Let’s discuss the paperwork you require to understand how I set up my personal tax account.

What do you need to Apply for the Paperwork?

National insurance number.

Recent pay slip.

UK passport (must be on date) or most recent P60.

Landline number or your mobile number, as part of the two-step security.

Choose the email address you want to attach to the account.

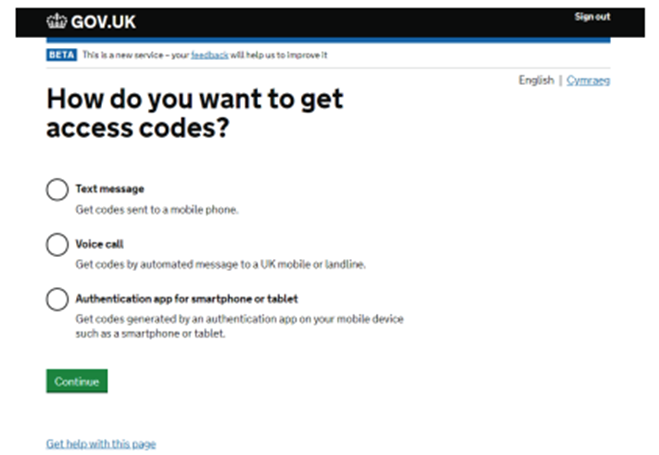

Now, you have acquired all the needed information to set up your personal account. Just go to the government gateway, and select either individual, (if you represent your own business) or agent (if you represent other people in financial matters to the government) to start the registration process.

How can I create my personal tax account?

There are a few steps to set up your personal tax account. We share those steps one by one in a largely simplified way.

1. Registration

You will need to register online by using this link on the official websiteof the HMRC to access the personal tax account.

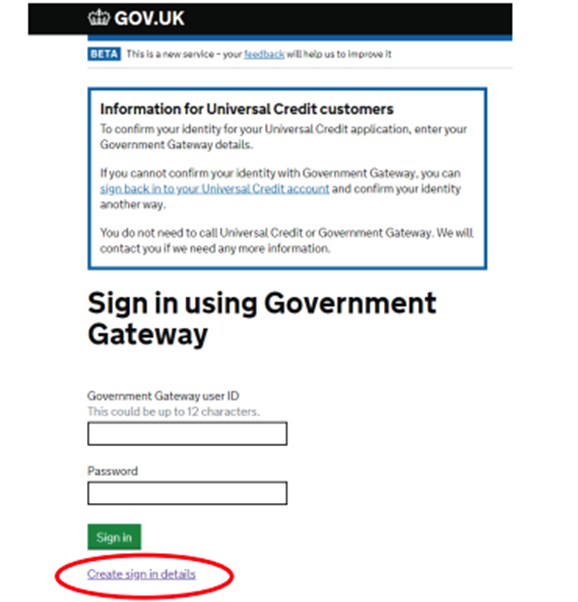

Click the ‘create sign-in details’ link given below the sign-in button to begin the registration process.

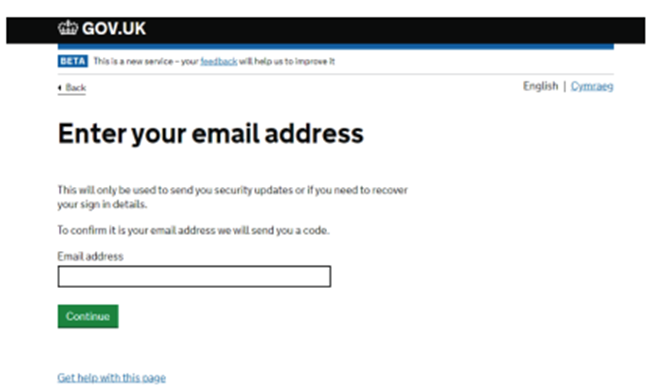

Then you will have to enter your email address. After doing so, select Continue.

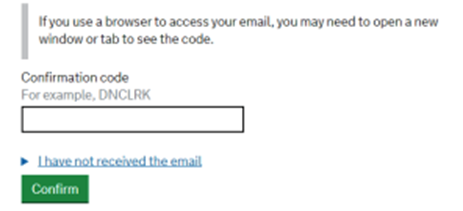

You will receive a code of 6 characters from HMRC at this email address.

Once you have entered the details in the given box, HMRC will prompt you to enter your full name and create a password. Then you will see your Government Gateway ID number.

2. Setting up your account

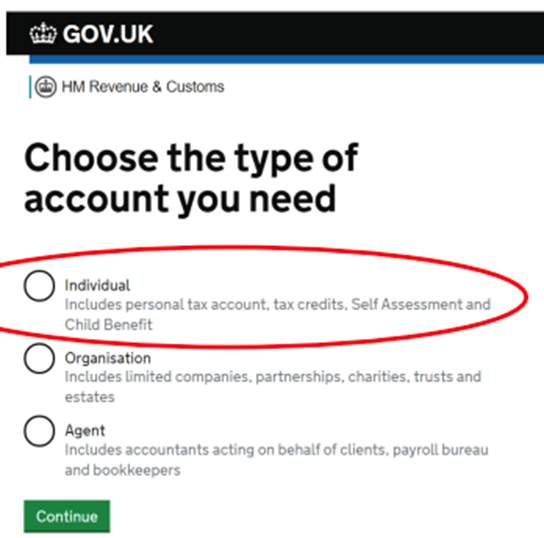

Here the HMRC will ask you to select the type of account you need. Please select “individual” and then click the green button of “continue”.

Now the HMRC will ask you to set up a method to receive an access code. It is important to know that select a method you are quite comfortable with because HMRC will use this method to send you an access code, every time you sign by using your Government Gateway user ID.

After selecting the method, you are most convenient with, click on the green button of “continue”.

Then HMRC will ask you to enter the 6 digits access code it has provided you with.

Kindly, enter the code and then click the green button “continue”.

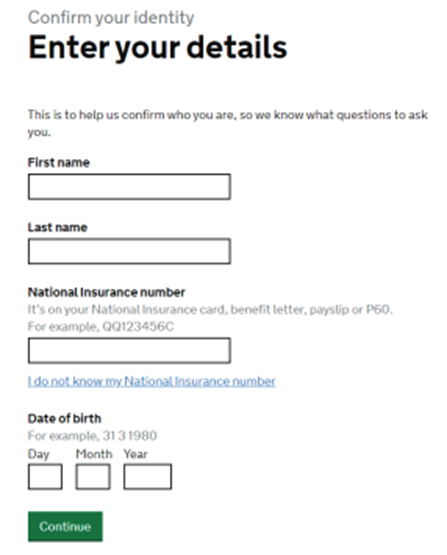

Now HMRC will ask you to confirm your identity, please provide the details where asked and then click the green button of “continue”.

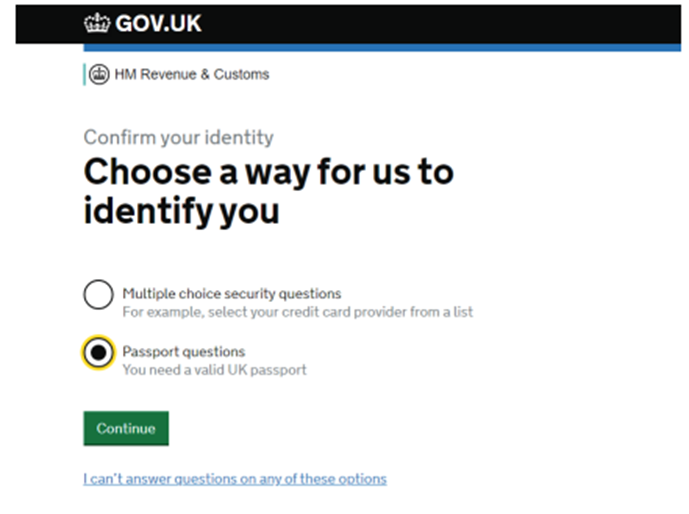

Now HMRC will ask you the way you want your identity o be confirmed by the HMRC. If you are a UK passport holder, you are recommended to use this option.

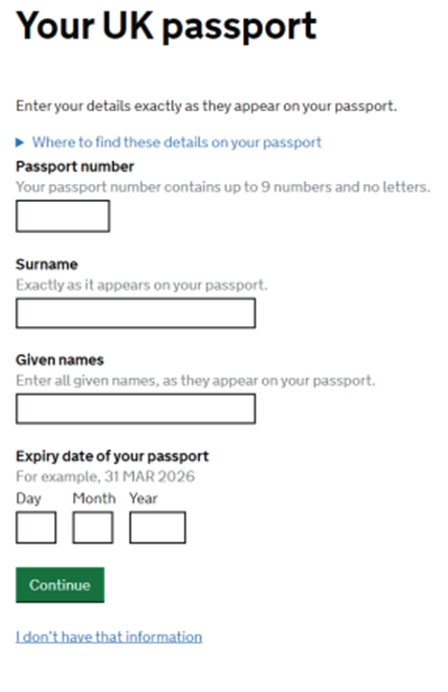

HMRC will ask you to share the same detail you have on your passport. Please enter the required details and then click the green button of “continue”.

Now HMRC will confirm whether the details you entered are correct and whether the personal tax account has been successfully set up. After its confirmation, you will be asked whether you would like to receive your correspondence regarding your tax affairs electronically or post via your Personal Tax Account. please select the option which is most suitable to you and select the green “continue” button. Now you will be taken to the Personal Tax Account home page.

3. Recovering Login Details

If you have previously used the online services of the government Gateway or HMRC to submit your tax returns electronically via the website of HMRC. You must log in by using those account details. But if you have forgotten the details of those accounts then please select one of the links given at the bottom of the sign-in page depending on the details you need to recover.

Now HMRC will take you, according to its process to recover your Government Gateway user ID or password.

If you face any difficulty with the process, you can easily contact HMRC for help.

Safety and security with your Personal Tax Account

After completing the registration procedure, you are the only person to have access to your personal tax account with your user ID and password.

Therefore, that answers your question, how do I set up my personal tax account?

Can my Personal Tax Account Help Review my National Insurance Record?

When it comes to reviewing your National Insurance record, your personal tax account can be particularly helpful. You can easily review your national insurance record that covers your entire working history by accessing your personal tax account. Reviewing your National Insurance record helps you ensure that your entire record is accurate and up to date. It also identifies any gaps in your contributions that might need to be addressed.

After that, when you reach the pension age, you can ensure that you have the correct credits to receive a full pension. If you find any discrepancies and gaps, the best option is to contact HMRC for investigation.

Can my Personal Tax Account Help Review my Employment Records?

Yes, your personal tax account gives you the additional benefit of reviewing your employment records.

It’s another benefit is that if you cannot obtain a copy of your P60 from your employer, you get it from your personal tax account. Once you understand how I set up my personal tax account, you can move forward with these steps.

Can Personal Tax Accounts Provide Information on PAYE codes?

Another useful feature of a personal tax account is that it enables you to view the PAYE codes use applied to your employment.

Moreover, you also have the option to modify your PAYE code directly from your personal tax account.

Is your Personal Information Secure?

When it comes to security, HMRC takes it seriously and uses firewall protection for all its systems. This is like a bulwark to provide maximum protection for your information because its detective capacity is strong enough to detect any unauthorized entry. All the data that you share with HMRC is encrypted and nobody can see your data except yourself.

Furthermore, you also must be conscious and vigilant of your online safety. Avoid sharing your user ID or password with anybody. If you cannot remember it and want to note it down, then ensure to keep it in a discrete place. Surely, you now have a clear idea of how I set up my personal tax account.

How Can I Ensure Nobody Accessed My Account?

One of the easiest ways, you must know whether someone accessed your account or not is the security measure of the system that shows you the time and date you logged into your personal tax account. Check this list frequently, if see any such thing that does not look right, immediately contact HMRC through their website.

Another safety measure built into the system is automatic logging out of your account if it is not active after 15 minutes. If you are forgetful, don’t worry, the system will secure your account.

Does HMRC Ask for Personal and Financial Detail?

It is important to know, and HMRC often emphasizes to be mindful of the procedure of HMRC that it does not ask for any personal or financial details by email, phone, or text. Always be on watch to protect yourself from the scammer, if notice any such thing as suspicious, report it to the HMRC, even if you have not lost anything. Undoubtedly, it is in your best interest to do so.

Shortly speaking, setting up a personal tax account offers a wide range of benefits by saving you a great deal of energy and time that you can utilize in something more productive and creative. You can easily check state pensions, national insurance contributions, and many other tax affairs online without standing in long queues on helplines or doing related paperwork. It keeps you updated and informed about your tax status. And through it, you can also keep HMRC timely updated and informed about your circumstances. Most importantly, your financial information is safe and secure.

FAQs

How do I activate my UTR number?

If your UTR (Unique Taxpayer Reference) is inactive, you can reactivate it by:

Contacting HMRC – Call the Self Assessment helpline and request reactivation.

Providing Personal Details – You may need to confirm your full name, address, National Insurance number, and date of birth.

Waiting for Confirmation – HMRC will confirm reactivation, usually via letter or phone.

How to check income tax?

You can check your income tax by:

Logging into your HMRC Personal Tax Account – View your tax payments, liabilities, and tax code.

Using the HMRC App – Check your tax status on the go.

Contacting HMRC – If you have queries about your tax records, call them for assistance.

How to file income tax?

To file your income tax return:

Register for Self Assessment if you haven’t already.

Gather Necessary Documents – Income records, expenses, and other tax-related details.

Complete Your Tax Return – Log in to your HMRC account and fill out the SA100 form.

Submit Before the Deadline – The deadline for online submissions is usually 31 January.

How do I create a UTR account?

To get a UTR number:

Register for Self Assessment with HMRC.

Provide Personal Information – Full name, address, date of birth, and National Insurance number.

Wait for UTR to Arrive – It is usually sent by post within 10 working days in the UK.

How do I check if my UTR is active?

You can check if your UTR is active by:

Logging into your HMRC account to view your Self Assessment status.

Calling HMRC – Provide your UTR and ask if it is active.

How to set up self-employed?

Register with HMRC for Self Assessment.

Keep Records of your income and business expenses.

Submit Your Tax Returns Annually to pay the correct amount of tax and National Insurance.

How do I check my UTR online?

You can find your UTR number by:

Logging into your HMRC account – Your UTR is listed in your tax documents.

Checking Previous HMRC Letters – It appears on tax returns and payment reminders.

How do I check my active tax status?

Use Your HMRC Personal Tax Account – Check your tax payments and liabilities.

Contact HMRC – If you’re unsure about your status, they can confirm it.

How long does it take to get a UTR?

HMRC usually issues a UTR within 10 working days if you’re in the UK or 21 days if you’re abroad.

How much money do you have to make as a self-employed person?

If you earn over £1,000 per tax year from self-employment, you must register with HMRC and file a tax return.

How do self-employed get money?

Self-employed individuals earn money by:

Charging clients/customers directly for services.

Selling products online or in-store.

Receiving payments through invoices, bank transfers, or platforms like PayPal.

How can I make money from home self-employed?

Options for making money from home include:

Freelancing – Writing, graphic design, programming, etc.

E-commerce – Selling on platforms like eBay, Etsy, or Amazon.

Affiliate Marketing – Promoting products for commissions.

Online Courses – Teaching skills through platforms like Udemy or Teachable.

How to earn $1,000 per day from home?

Earning $1,000 per day requires high-income skills or scalable businesses:

Dropshipping or E-commerce – Selling trending products online.

Stock Trading or Cryptocurrency – Requires experience and risk management.

Freelance Consulting – High-ticket services like business coaching.

Online Courses & Digital Products – Selling valuable knowledge at scale.

What is the fastest way to become self-employed?

Identify a skill or service you can offer immediately.

Register as self-employed with HMRC.

Find clients through online platforms like Fiverr, Upwork, or LinkedIn.

Start small and reinvest earnings to grow your business.

How to earn money from Google at home?

Google offers multiple ways to make money:

Google AdSense – Earn from ads on a blog or YouTube channel.

Google Play Store – Develop and sell apps.

Google Opinion Rewards – Get paid for surveys.

YouTube Partner Program – Monetize videos through ads and memberships.

In the dynamic world of UK property investment, understanding and adhering to HM Revenue & Customs (HMRC) regulations is crucial. HMRC compliance assistance isn’t just about ticking boxes—it’s about safeguarding your investments, avoiding hefty fines, and maintaining a reputable standing in the industry. This comprehensive guide will help landlords and property investors navigate the complex terrain of tax compliance for landlords, ensuring smooth sailing in your property ventures.

Imagine driving a car without understanding the rules of the road. Sooner or later, you’re bound to run into trouble. Similarly, without proper knowledge of property tax compliance UK, landlords and investors risk facing penalties, legal issues, and financial losses.

Why Compliance Matters