Once you have a property company generating profits, the next strategic question is equally important: how do you get the money out efficiently? Paying yourself incorrectly can convert a corporation-tax saving into a personal income-tax disaster. This article sets out the 2025/26 rules and the optimal approach for property company directors.

Property Company Corporation Tax: What Comes First?

Your company must settle its HMRC corporation tax liability before distributions can be made. For periods from 1 April 2025: 19% applies to profits up to £50,000 (small profits rate); 25% applies to profits above £250,000 (main rate); and marginal relief applies between £50,001 and £250,000.

Taking a Salary from Your Property Company

A salary is the company’s deductible expense — it reduces the taxable profit and therefore the corporation tax bill. However, it attracts both employer’s (13.8%) and employee’s (8% or 2%) National Insurance Contributions.

The Optimal Salary Strategy

Many property company directors pay themselves a salary at the National Insurance Lower Earnings Limit (£6,396 for 2025/26) to retain state benefit entitlement, or at the Personal Allowance level (£12,570) to minimise total NIC cost. A salary of £12,570 avoids employee NIC while still triggering employer NIC — a specialist accountant will run the precise numbers.

Taking Dividends from a Property Company

Dividends are paid from post-corporation-tax profits. They are not subject to NICs, making them more efficient than salary for most director-shareholders. However, they do not reduce the company’s corporation tax bill.

Tax Band

Income Range (2025/26)

Dividend Tax Rate

Basic rate

Up to £50,270

8.75%

Higher rate

£50,271 – £125,140

33.75%

Additional rate

Above £125,140

39.35%

Dividend allowance

First £500 of dividends

0%

Property Company Pension Contributions

Employer pension contributions paid by the company are deductible before corporation tax — and they are not a benefit-in-kind for the director receiving them. This makes pension contributions arguably the most tax-efficient extraction method available.

Company deducts contribution: saves 19–25% corporation tax

No income tax or NICs on the contribution going in

Growth within the pension is free from income tax and CGT

Annual allowance: £60,000 per individual (2025/26), reduced under tapering for high earners

Optimising Your Extraction Mix: The Three-Layer Approach

Layer

Method

Why It Works

Layer 1

Small salary (£6,396–£12,570)

Preserves state benefit entitlement; company gets deduction

Layer 2

Pension contributions (up to £60,000)

Maximum corp tax deduction; no personal tax now

Layer 3

Dividends (remaining profit)

Lower effective rate than employment income; no NICs

Compliance Requirements

Dividends require board minutes documenting the declaration — even if you are sole director

Dividends can only be paid from distributable (post-tax) reserves — not from projected future profits

PAYE must be registered and returns filed in real time via RTI if any salary is paid

Family shareholder arrangements must not fall foul of the settlement rules (S.619 ITTOIA 2005)

Is it better to take salary or dividends from my property company?

In most cases, a combination is most efficient: a low salary (£6,396–£12,570) to preserve state benefits and create a corporation tax deduction, then dividends for the remainder. Pension contributions should be maximised before dividends are considered.

Can I pay my spouse a salary or dividends from my property company?

Yes, provided they hold shares or perform genuine work. Dividend distribution to spouse-shareholders is permissible but subject to the settlement rules if their shares do not carry genuine rights. Take professional advice before structuring family arrangements.

What are distributable reserves and why do they matter?

Distributable reserves are accumulated after-tax profits that can legally be paid as dividends. If your company has made losses or hasn’t yet produced accounts, a dividend paid without distributable reserves is unlawful and may be reclassified as a loan to the director.

How much can my company pay into my pension each year?

There is no company contribution limit per se, but total pension input (employer plus employee) must not exceed the annual allowance — £60,000 for 2025/26 — nor exceed the individual’s relevant UK earnings if claiming personal tax relief. Company employer contributions bypass the earnings cap.

What happens if I draw too much from the company?

Drawings without a corresponding salary, dividend, or loan agreement create an overdrawn director’s loan account. If this exceeds £10,000 or is not repaid within nine months of the year-end, Section 455 tax (33.75%) is charged on the outstanding balance.

Understanding the most tax-efficient way to extract profits from a property company can save thousands in tax over time. Book a consultation with Felix Accountants today.

For a property investor, claiming every allowable expense is one of the most straightforward routes to improving net returns — no new strategy required, just disciplined record-keeping and a clear understanding of HMRC rules. Yet surveys consistently show that landlords underclaim, leaving significant tax savings unclaimed each year.

The Core Rule: ‘Wholly and Exclusively’

Under HMRC’s Property Income Manual (PIM2010), an expense is deductible only if it is incurred wholly and exclusively for the purpose of letting the property. A dual-purpose cost — partly personal, partly business — is either apportioned or disallowed entirely depending on the nature of the expense.

Example: Apportionment in Practice

If your mobile phone is used 60% for property management and 40% personally, you may claim 60% of the annual contract cost. Broadband costs, home-office costs, and vehicle use can be treated similarly — but HMRC will challenge estimates that cannot be substantiated.

Allowable Expenses Every Property Investor Can Claim

Expense Category

What Is Deductible

HMRC Reference

Repairs & maintenance

Routine repairs to restore original condition (e.g. fixing boiler, repainting, replacing broken windows)

Lease renewals under 1 year, pursuing rent arrears, accountancy fees

PIM2135

Utilities paid by landlord

Gas, electricity, water, broadband, council tax if borne by landlord

PIM2110

Advertising costs

Online listings, photography, ‘to let’ boards

PIM2065

Ground rent & service charges

If leasehold property, these are deductible

PIM1070

Replacement of domestic items

Like-for-like replacement of furniture, white goods (Replacement Domestic Items Relief)

PIM3210

Section 24 Tax Rules for Property Investors

Individual landlords cannot fully deduct mortgage interest. Since 6 April 2020, the restriction has been at 100% — you receive only a 20% tax credit on finance costs. This makes holding property personally significantly less efficient for higher-rate taxpayers.

Ownership Type

Finance Cost Treatment

Example: £10,000 Interest, 40% Taxpayer

Personal ownership

20% tax credit only

Tax saved: £2,000 (not £4,000)

Limited company

Full deduction before corporation tax

Tax saved: £2,500 (at 25% CT)

Capital vs Revenue — A Critical Distinction

Not everything that costs money on a property is deductible as a revenue expense. Capital expenditure — improvements that enhance the property beyond its original state — is not deductible against rental income. It may, however, be added to the base cost of the property for CGT purposes on eventual disposal.

Revenue (Deductible) vs Capital (Not Deductible)

Replacing a broken boiler with an equivalent model = revenue (deductible)

Installing an air-source heat pump in a property that had none = capital (not deductible)

Repainting and patching walls = revenue (deductible)

Extending the kitchen = capital (add to base cost for CGT)

The £1,000 Property Income Allowance

Individuals with gross rental income below £1,000 need not report it. Where income is slightly above this, they can opt to use the allowance instead of claiming actual expenses — but not both simultaneously. For most active landlords with genuine costs, detailed expenses will produce a better result.

Property Investor Expense Checklist

Before year-end: (1) collect all invoices and receipts, (2) reconcile bank statements, (3) apportion dual-purpose costs, (4) calculate total finance costs separately, (5) identify any missed capital items for CGT records, (6) review whether any losses can be carried forward.

Expenses Property Investors Cannot Claim

Capital mortgage repayments (only the interest element qualifies for the 20% credit)

Personal insurance not connected to the letting business

Improvements and extensions to the property

Costs relating to personal occupation periods in a let property

Can I deduct my mortgage payments from rental income?

No. Capital repayments are never deductible. For individually-owned properties, you receive a 20% tax credit on the interest portion only. Limited companies can deduct the full interest before corporation tax.

Is travel to inspect my property tax-deductible?

Yes, provided the travel is wholly and exclusively for the purpose of managing or inspecting the property. Personal commuting or journeys with a dual purpose cannot be claimed. Keep a mileage log with dates and reasons.

Can I claim accountancy fees as a property expense?

Yes. Accountancy and bookkeeping fees directly related to your rental business are allowable under PIM2135. Fees for personal tax matters unrelated to the property are not.

What is Replacement Domestic Items Relief?

This relief (introduced in 2016) allows landlords to deduct the cost of replacing furnishings and domestic appliances with equivalent items. It applies to residential let properties and replaces the old Wear and Tear Allowance.

Can I carry forward a property loss?

Yes. If allowable expenses exceed rental income in a tax year, the resulting loss is carried forward against future rental income from the same property business. It cannot offset general earned income unless the activity qualifies as a trade.

Understanding allowable expenses is one of the easiest ways for a property investor to reduce their tax bill legally.

One of the most consequential decisions any UK property investor faces is deceptively simple to state: should you buy property in your personal name, through a limited company, or via a Limited Liability Partnership (LLP)? The answer will shape your tax bill, your mortgage options, your estate planning, and your long-term wealth for decades. This guide sets out the 2025/26 framework clearly so you can make the right call for your circumstances.

Key Insight

At 2025 rates, a basic-rate taxpayer might save very little by incorporating — but a higher-rate investor with four or more properties and long-term reinvestment plans could save tens of thousands in tax annually through a corporate structure.

The 2025/26 UK Property Tax Landscape

Before choosing a structure, understand the current rates that frame the decision.

Tax Type

Rate (2025/26)

Applies To

Corporation tax

19% (profits ≤£50k) — 25% (profits >£250k)

Limited companies

Income tax

20% / 40% / 45%

Individual landlords

Dividend tax

8.75% / 33.75% / 39.35% (£500 free)

Company profit extraction

Mortgage interest relief

20% tax credit only

Individual landlords

SDLT surcharge

3% on additional dwellings

All investors

Option 1: Should I Buy Property in Your Personal Name?

Advantages

No Companies House filings, statutory accounts, or director duties

Rental profits are directly accessible — no dividend procedures

Broader mortgage market with often better rates for individuals

Personal allowance (£12,570) means the first portion of profit may be tax-free

Disadvantages

Rental profits above £50,270 are taxed at 40–45% income tax

Mortgage interest relief restricted to a 20% tax credit (Section 24, Finance Act 2015)

Full property value sits in your IHT estate at 40% above the nil-rate band

Fewer mortgage lenders; rates typically 0.5–1% higher

Annual accounts, CT600, and Companies House compliance required

Option 3: Should I Buy Property Through an LLP?

An LLP blends the limited liability of a company with the tax transparency of a partnership. Profits flow directly to members and are taxed at their personal rates — but full interest deduction is available where HMRC accepts the activity as a genuine property business.

Factor

Personal Ownership

Limited Company

LLP

Tax on profits

20–45% income tax

19–25% corp tax + dividend tax on extraction

Members’ personal tax 20–45%

Interest relief

20% tax credit only

Fully deductible

Deductible if business activity proven

Reinvestment potential

Taxed first, then reinvest

Reinvest at 19–25% CT rate

Taxed on members before reinvestment

Succession planning

Complex — CGT/SDLT on transfer

Shares transferable flexibly

New members easily added

Administration

Low

Moderate to high

Moderate

Which Structure Is Right for You?

Run these five questions before deciding:

Will I live off the income now, or reinvest for portfolio growth?

Am I investing alone or with a partner, spouse, or family?

How important is limiting personal liability?

Do I intend to pass the portfolio to family?

Is this buy-to-let, serviced accommodation, or active development?

Felix’s Practical Tip

Start with the end in mind. The structure you choose today determines how easily you can borrow, grow, and eventually pass on your wealth. Once you hold multiple properties personally, restructuring is expensive — SDLT and CGT can bite hard. Choose for the future, not for today’s convenience.

Frequently Asked Questions on How to Buy Property in the UK

Is it better to buy property in my own name or through a company in 2025?

For higher-rate taxpayers planning long-term portfolio growth, a limited company typically provides superior tax efficiency through lower corporation tax rates and full mortgage interest deduction. Personal ownership is simpler and may suffice for one or two properties with low gearing.

Can I move properties from my personal name into a company?

Yes, but this is treated as a disposal at market value, potentially triggering CGT and SDLT. Incorporation Relief (s.162 TCGA 1992) can defer CGT if the activity qualifies as a business. See our dedicated guide at felixaccountants.com/transfer-property-into-company-without-paying-tax/

What is Section 24 and does it affect my decision on how to buy property?

Section 24 (Finance Act 2015) restricts individual landlords to a 20% tax credit on mortgage interest rather than a full deduction. Limited companies are unaffected. This restriction is often the primary driver for incorporation decisions.

Does an LLP pay corporation tax when they buy property?

No. An LLP is tax-transparent — profits are allocated directly to members and taxed at their personal income tax rates. This means no corporation tax at entity level, but also no benefit from the lower 19–25% corporate rates.

What SDLT surcharge applies when you buy property through a company?

Companies purchasing residential property for £500,000 or more face a flat 15% SDLT rate unless the property is held for genuine letting or development purposes. The standard 3% additional-dwelling surcharge also applies to corporate purchases below that threshold.

Ready to choose the right structure? Let Felix Accountants map out your optimal ownership model.

Maximizing legitimate tax deductions remains the most effective action an enterprise leader can take to protect corporate revenue. Pass-through business structures provide excellent operational flexibility, but they naturally expose your net profits to aggressive self-employment levies. Every dollar you fail to account for represents an unnecessary transfer of wealth directly to the federal government.

Following extensive updates codified under the One, Big, Beautiful Bill Act (OBBBA), legal avoidance requires a precise understanding of evolving depreciation rules, structural changes, and administrative frameworks. Many founders assume standard accounting applications capture every available offset, yet software only interprets the information it receives. You must actively implement structural tax reduction mechanisms to ensure your company keeps its hard-earned capital.

Optimizing your annual filing requires shifting away from basic expense logging. By adjusting your entity classifications, implementing specialized corporate reimbursement frameworks, and maximizing retirement allocations, you can structurally reduce your taxable base.

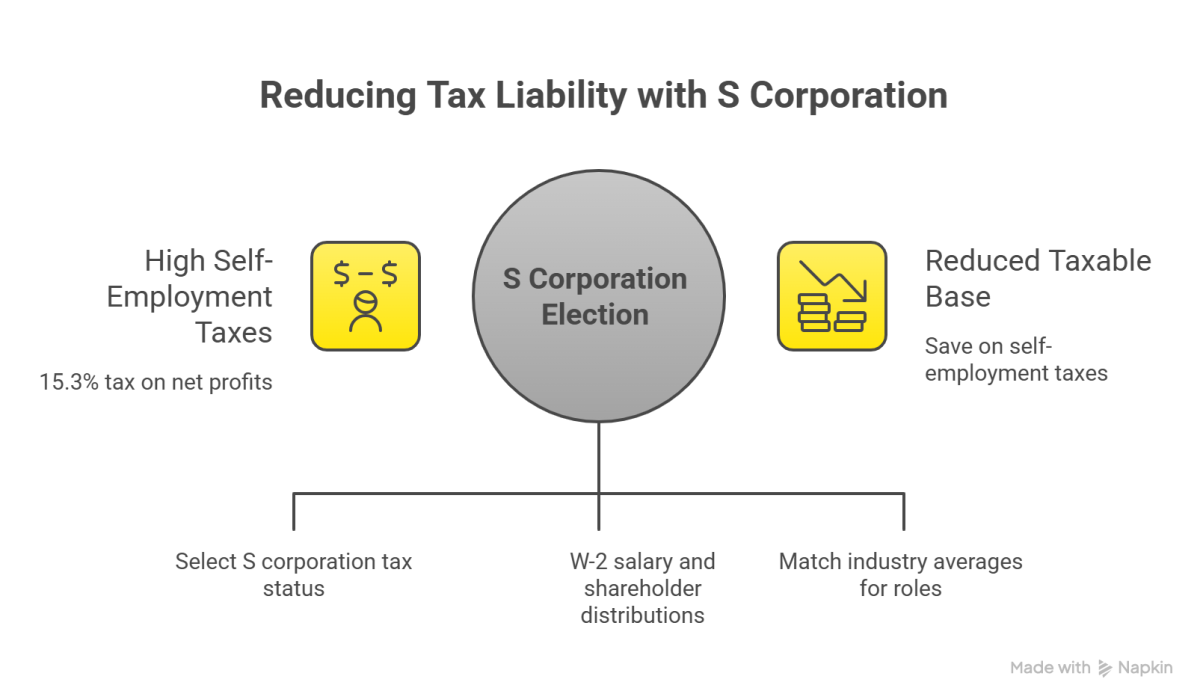

The default pass-through classification forces a single-member LLC to pay a 15.3% self-employment tax on 100% of its net operational profits. You can legally alter this financial trajectory by filing IRS Form 2553 to select an S corporation tax status. This structural optimization preserves your limited liability protections while shifting how the federal government assesses payroll taxes on your distributions.

Once the S corporation status takes effect, you divide your corporate earnings into two separate components: a W-2 salary and shareholder distributions. Your W-2 wage remains subject to standard FICA obligations, while the remaining operational profits flow to your personal return entirely free from self-employment taxes.

For example, under a standard LLC structure with a net income of $140,000, the entire amount is subject to the 15.3% self-employment tax, resulting in a total FICA tax liability of approximately $21,420. By optimizing as an S corporation, you can split that same $140,000 net income into a reasonable W-2 salary of $65,000 and a shareholder distribution of $75,000. FICA taxes only apply to the salary portion, while the distribution portion remains entirely exempt, saving you roughly $11,475 in self-employment taxes.

The Internal Revenue Service closely monitors S corporation business owners to ensure W-2 compensation matches industry averages for comparable roles. If you set an unrealistically low wage to maximize tax-exempt distributions, the government can reclassify your entire distribution pool during an audit. This strategy typically yields clear financial advantages once your company’s clean net income safely surpasses $75,000 annually.

Implementing Accountable Plans for Clear Deductions

Many managers distribute flat monthly stipends to cover team internet fees, mobile connections, or travel costs. The IRS explicitly treats undocumented monthly stipends as ordinary taxable wages, which increases your corporate payroll obligations.

To convert personal operational outlays into clean corporate tax deductions, your company must formalize a written Accountable Plan under IRS Publication 463. This administrative framework enables owners and staff to claim tax-free reimbursements for expenses incurred while advancing business operations.

An eligible reimbursement process demands absolute adherence to three core statutory requirements. First, the expense must have a clear commercial intent, meaning it is ordinary and necessary for your specific industry. Second, the claimant must provide proportional verification by submitting receipts, mileage records, or invoices within 60 days. Third, any excess funds advanced must return to the corporate account within 120 days.

By leveraging a formal accountable plan, your business can claim direct tax deductions for shared home utilities, digital tool subscriptions, and vehicle mileage without triggering employee-level income taxes.

Home Office Deductions and Boundary Management

The home office write-off offers a substantial tax benefit, yet many remote business owners avoid it out of audit anxiety. You can claim these tax deductions safely by maintaining clear physical and functional boundaries within your primary residence. The IRS demands that your workspace serve as your principal place of business and remain exclusively dedicated to commercial activity.

Dual-use areas do not qualify for this treatment. If your workspace contains a guest bed or double-functions as a family entertainment zone, the entire room loses its tax-deductible status. You can compute your deduction using the simplified method or the actual expense method.

Measurement Approach

Calculation Metric

Maximum Allowance

Recordkeeping Rules

Simplified Method

Fixed $5 per square foot

Up to 300 sq. ft. ($1,500 maximum)

Basic verification of area dimensions

Actual Expense Method

Percentage of residential square footage applied to housing costs

Proportional to total expenses

Itemized records of rent, utilities, insurance

For companies leasing high-value residential property, tracking actual expenditures regularly generates far superior tax deductions. If your workspace occupies 25% of your home’s total area, you can write off 25% of your rent, electrical grid costs, and seasonal climate control bills.

Section 199A and the Pass-Through Shield

The Section 199A Qualified Business Income (QBI) deduction enables eligible pass-through owners to deduct up to 20% of their net business income before ordinary income taxes apply. For the 2026 tax year, the baseline threshold limits match inflation adjustments, sitting at $201,750 for single filers and $403,550 for married individuals filing joint returns.

When your pass-through net income exceeds these limits, complex statutory phase-outs apply based on your industry classification. If your firm operates as a Specified Service Trade or Business (SSTB)—such as a consulting agency, medical practice, law firm, or financial advisory—the deduction phases down and eventually hits zero. Under the OBBBA, the phase-in range itself has been liberalized, which gives business owners a larger cushion before the full limitation completely restricts the write-off.

For non-SSTB operations with revenues exceeding the caps, the deduction relies on a specific wage and property limitation:

Maximum Deduction =max left 50% text of corporate W-2 wages 25% text of W-2 wages + 2.5% of the property basis

If your service-based company approaches the threshold limit, you can protect your QBI deduction by intentionally reducing your personal Modified Adjusted Gross Income (MAGI). Directing corporate profits into pre-tax retirement structures lowers your personal taxable income, keeping your business beneath the phase-out boundary.

Maximizing 100% Bonus Depreciation under the OBBBA

Following the legislative implementation of the One Big Beautiful Bill Act (OBBBA), 100% bonus depreciation has been permanently restored for qualified business property placed in service during 2026. This adjustment provides an immediate cash flow benefit, completely reversing the previous phase-down timelines that threatened to phase the benefit out entirely.

When your company purchases qualifying assets like network servers, industrial machinery, field equipment, or specialized commercial software, you can write off the entire cost in the first year.

To secure this deduction, you must place the asset into active service before midnight on December 31. Purchasing equipment that remains in shipping crates until the following January postpones the entire tax write-off by a full calendar year. IRS Notice 2026-11 confirms that both the contract acquisition date and the operational placed-in-service date must comply with these timing rules to capture the full first-year value.

Frequently Asked Questions

How do LLC tax write offs work?

LLC tax write offs work by reducing your business’s net taxable income before profits flow through to your personal tax return. When you claim eligible tax deductions for ordinary and necessary business expenses, you lower the overall profit base that is subject to federal income and self-employment taxes.

How much can an LLC write off?

An LLC can write off any amount of eligible expenses, provided the costs are ordinary, necessary, and directly connected to running the business. There is no flat statutory limit on total operating tax deductions, but capital investments and startup costs must follow specific annual thresholds and depreciation schedules.

How do LLC owners avoid taxes?

LLC owners avoid taxes legally by maximizing deductions, establishing corporate accountable plans, and electing S corporation status to shield distributions from self-employment levies. They also utilize advanced asset depreciation strategies under the OBBBA framework and maximize pre-tax contributions to self-employed retirement accounts to lower their total adjusted gross income.

Can a single-member LLC write off expenses?

Yes, a single-member LLC can write off expenses directly by documenting ordinary and necessary business outlays on Schedule C of IRS Form 1040. These tax deductions lower the pass-through income figure that is ultimately subject to personal income tax and federal self-employment tax assessments.

Can you deduct LLC expenses on personal taxes?

You can deduct LLC expenses on personal taxes because default LLC structures operate as pass-through entities where all financial activities flow directly to your personal return. You report these business tax deductions on Schedule C or Schedule E, which ultimately reduces your overall personal tax obligation.

What is the difference between a deductible expense and a capital expenditure?

A deductible expense is an operational cost completely written off within the current tax year, such as office rent, marketing, or utilities. A capital expenditure represents an investment in a long-term asset that must be depreciated over its useful life, unless accelerated by Section 179 or bonus depreciation rules.

What documentation is required to support LLC write-offs?

To support LLC tax deductions, the IRS requires comprehensive documentation, including itemized receipts, corporate bank statements, canceled checks, paid invoices, and contemporaneous travel logs. These records must clearly demonstrate the exact amount, transaction date, vendor identity, and specific commercial purpose of each claimed expenditure.

What business expenses are tax deductible?

Business expenses are tax deductible if they are universally recognized as ordinary and necessary within your specific industry. Common examples include corporate software subscriptions, marketing campaigns, professional legal advice, dedicated home office facilities, employee payroll costs, and vehicle mileage accrued during commercial transport operations.

Maximizing tax deductions remains the most effective way for small business owners to shield their hard-earned revenues from unnecessary liability. Every dollar overlooked on a tax return is a dollar of pure profit surrendered to the Internal Revenue Service. Following major updates codified under the One, Big, Beautiful Bill Act (OBBBA), navigating the tax code requires careful adjustment to new thresholds, phased reductions, and updated structural frameworks.

Many entrepreneurs mistakenly assume their accountants catch every write-off. In reality, accounting systems only process the data they are given. If you fail to track specialized operational outlays, your business will miss major opportunities to lower its taxable base.

Strategic planning under the current tax code requires looking past the standard expense categories. By understanding the specific mechanisms governing asset depreciation, employee reimbursements, and structural deductions, you can dramatically shift your bottom-line profitability.

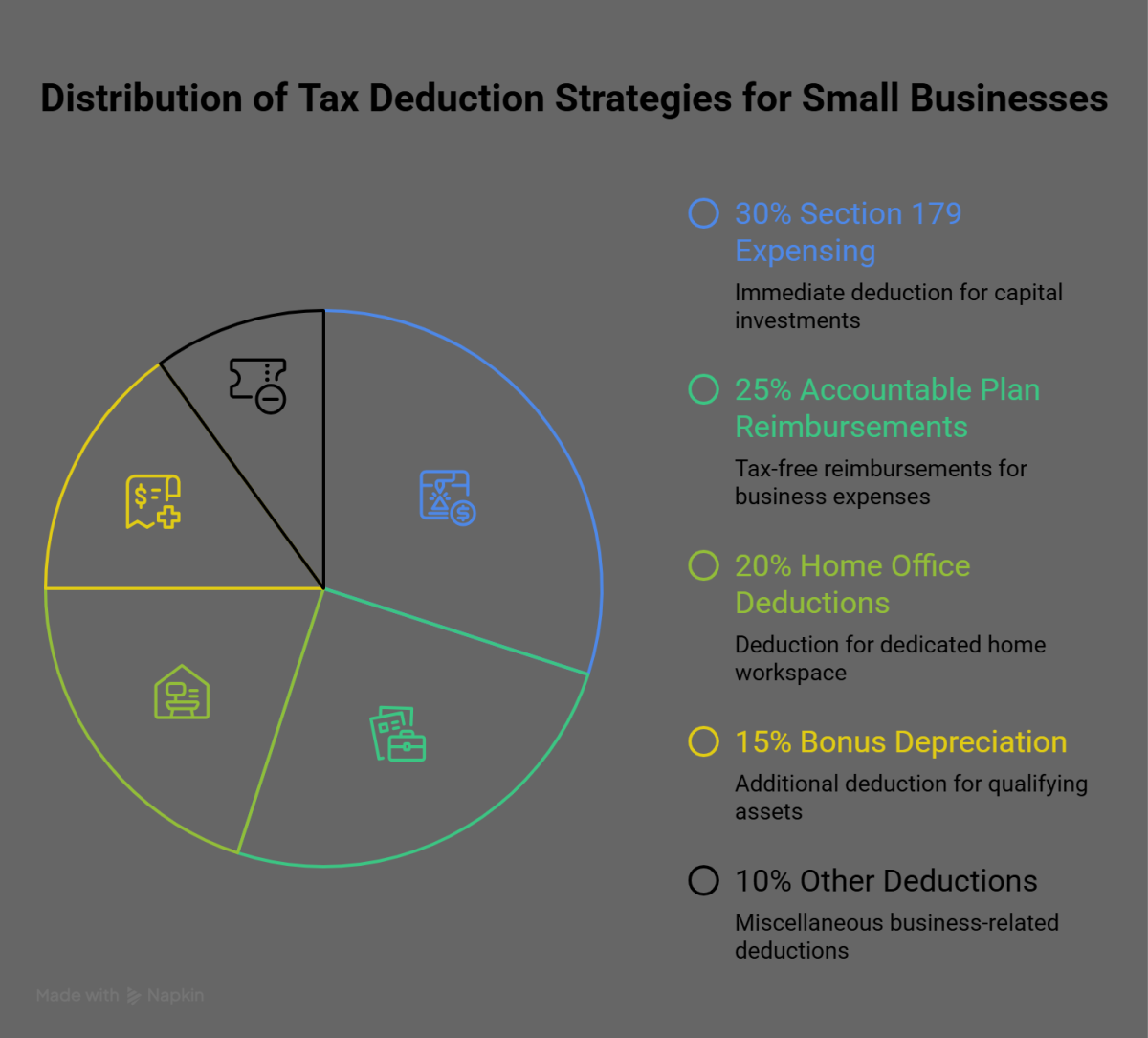

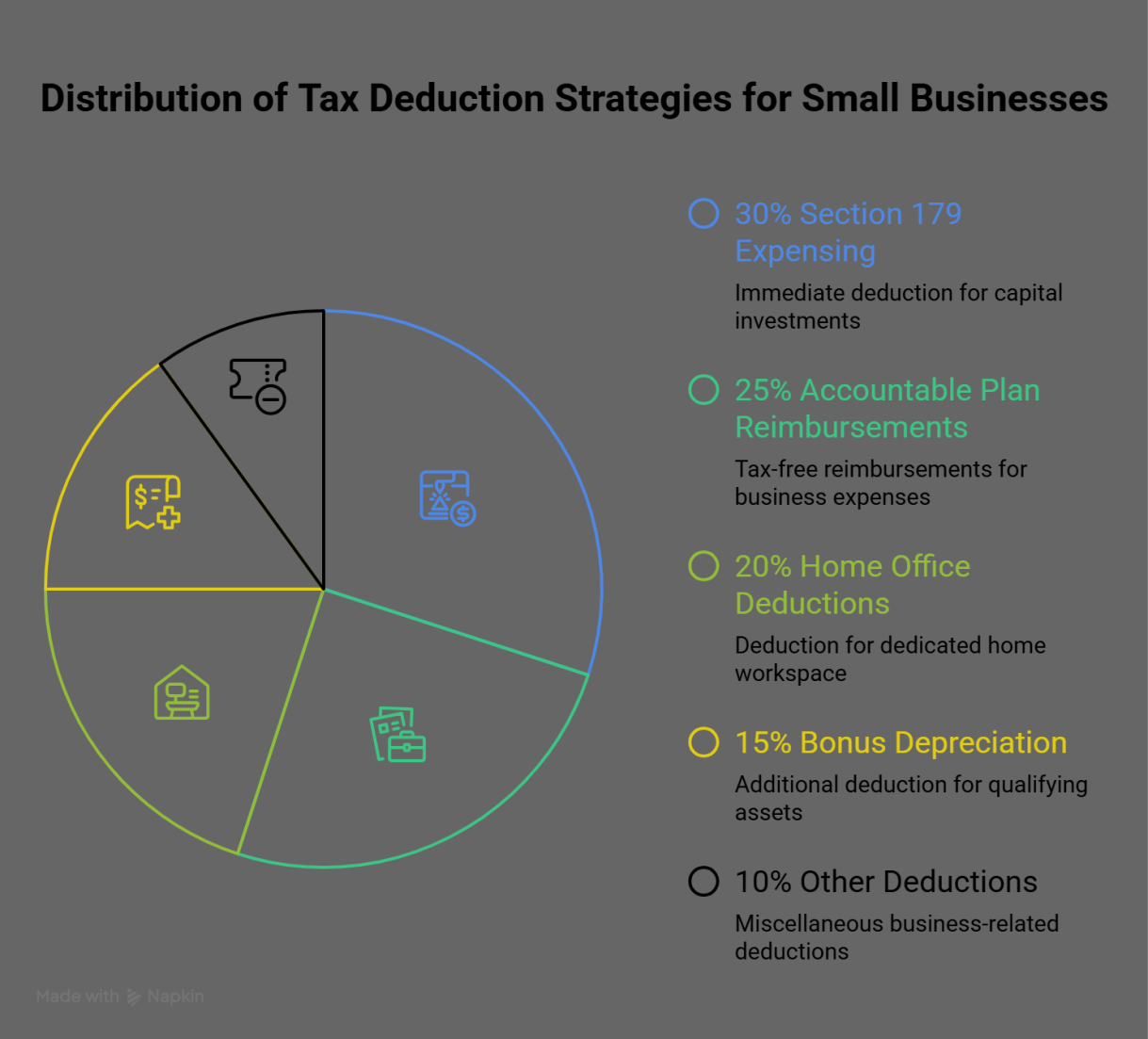

Overlooked Depreciation Strategies under Section 179

The Section 179 expensing framework provides small businesses with an immediate tool to offset capital investments. For the 2026 tax year, the maximum write-off threshold stands at $1.32 million, with the phase-out limit beginning at $3.29 million of qualifying property. This allows companies to deduct the full purchase price of qualifying equipment, machinery, and off-the-shelf software in the first year it is deployed.

The critical tactical error most owners make is focusing solely on the date of purchase. The IRS strictly mandates that an asset must be placed in service before December 31 to qualify for the deduction. If you purchase a server rack or specialized manufacturing machinery in late December, but the equipment sits in crates until January, you cannot claim the write-off for that tax year. It must be completely installed, configured, and operational.

Bonus depreciation complicates this strategy. Under current law, bonus depreciation has stepped down to 60% for property placed in service during 2026. Because Section 179 allows for a 100% upfront deduction up to the cap, business owners must sequence their asset deductions carefully. You should exhaust your Section 179 limits on assets that do not qualify for other preferential treatments before applying the 60% bonus depreciation to remaining capital expenditures.

Vehicles present another heavily restricted territory. The “SUV loophole” or Section 179 heavy vehicle deduction applies to vehicles with a Gross Vehicle W

eight Rating (GVWR) between 6,000 and 14,000 pounds. While passenger sedans face strict luxury automobile depreciation caps, heavy trucks, vans, and large SUVs used more than 50% for business can qualify for immediate expensing limits.

The Mechanics of an Accountable Plan

Many businesses reimburse workers or founders for out-of-pocket operational costs using simple, flat monthly stipends. Doing so turns tax deductions into taxable employee income. If you give a remote team member a flat $100 monthly allowance for internet and phone expenses without requiring documentation, the IRS classifies that payout as ordinary wages. This triggers payroll taxes for the company and income taxes for the recipient.

To secure tax deductions without generating tax liabilities, companies must implement a formal accountable plan under IRS Publication 463. This administrative framework relies on three rigid criteria:

Business Connection: The expense must be ordinary and necessary, incurred while performing services for the company.

Substantiation: The individual must provide documentary evidence, such as receipts, logs, or invoices, within a reasonable period (typically 60 days).

Return of Excess: Any allowance overages must be returned to the business within a reasonable period (typically 120 days).

By utilizing an accountable plan, the business deducts the exact cost of home internet, cellular plans, travel, and specialized training as a direct operating expense. The employee receives the reimbursement completely tax-free. Transitioning from flat stipends to an accountable plan shields your company from unnecessary FICA exposure.

Home Office Deductions and Shared Utilities

The home office write-off remains heavily underutilized due to lingering fears of triggering an audit. This hesitation costs remote entrepreneurs thousands in potential tax deductions. To qualify under current IRS guidelines, a home workspace must meet two uncompromising conditions: it must be your principal place of business, and it must be used exclusively and regularly for work.

Exclusive use means the space cannot serve a dual purpose. A dedicated room or a clearly partitioned area of a room satisfies the rule. A desk placed in the corner of a child’s playroom or utilizing the dining room table does not. If a single square foot of the designated zone is used for personal activities, the entire space loses its eligibility.Owners can calculate the deduction using either the simplified method or the actual expense method:

Method

Calculation

Maximum Limit

Recordkeeping Requirements

Simplified Method

Fixed rate of $5 per square foot

Up to 300 sq. ft. ($1,500 maximum)

Basic proof of square footage and business use

Actual Expense Method

Percentage of home square footage applied to total housing costs

For owners renting high-cost residential property, the actual expense method yields far greater tax deductions. If your dedicated workspace consumes 20% of your apartment’s total footprint, you can write off 20% of your rent, electricity, heating, trash collection, and renter’s insurance. Furthermore, home internet and cell phone connections should be isolated from the general home office calculation.

If you have a single internet line used for both commercial operations and family streaming, you can deduct the exact percentage dedicated to work. Maintaining a completely separate broadband connection or secondary cellular line dedicated solely to the company streamlines this process, allowing for a clean 100% deduction without complex tracking logs.

Maximizing the Qualified Business Income Deduction

The Section 199A Qualified Business Income (QBI) deduction allows eligible sole proprietors, partnerships, S corporations, and LLCs to deduct up to 20% of their qualified business income. For the 2026 tax year, the core inflation-adjusted thresholds sit at roughly $203,000 for single filers and $406,000 for married individuals filing jointly.

Once your pass-through net income crosses these specific limits, phase-out rules introduce complex restrictions based on the nature of your company. If your enterprise is classified as a Specified Service Trade or Business (SSTB)—which includes fields like law, medicine, consulting, financial services, and performing arts—the deduction begins to claw back. Above the upper phase-out limits, the QBI deduction drops to zero for SSTBs.

For non-SSTB businesses operating above the thresholds, the deduction is strictly limited to the greater of:

50% of the W-2 wages paid by the business

OR

25% of the W-2 wages + 2.5% of the unadjusted basis immediately after acquisition (UBIA) of qualified property

Pass-through owners can intentionally manage their QBI position through entity structuring and compensation design. If you operate an S corporation and your revenue is tracking well above the threshold, paying yourself too low a salary reduces the company’s total W-2 wage pool, which can inadvertently cap your overall QBI deduction.

Conversely, a sole proprietor facing an SSTB phase-out can lower their modified adjusted gross income (MAGI) by maximizing contributions to a solo 401(k) or a defined benefit plan, pulling their income back below the threshold to rescue the full 20% write-off.

Mileage, Travel, and S Corporation Compensation

The standard mileage rate has risen to 72.5 cents per mile, as detailed in IRS Notice 2026-10. This rate accounts for fuel, depreciation, insurance, and maintenance. Despite the higher rate, owners frequently forfeit this deduction by failing to maintain a contemporaneous mileage log. Retrospective logs reconstructed at the end of the year via calendar entries often fail to survive IRS scrutiny during an examination. A valid log must record the date, destination, exact business purpose, and starting and ending odometer readings for every trip.

For heavy vehicle usage, calculating actual expenses—including actual fuel costs, repairs, insurance, and structural depreciation—often yields greater tax deductions than the standard mileage rate. However, once you choose the actual expense method for a leased vehicle, you cannot switch to the standard mileage rate in subsequent years.

Travel expenses outside your local tax home present another area of lost opportunity. While business meals remain restricted to a 50% deduction rule, related travel costs like airfare, lodging, dry cleaning, and rideshares are 100% deductible. When combining business trips with personal vacation days, the primary purpose of the trip must be commercial.

If a trip is primarily personal, you cannot deduct the transportation costs, though you can still claim specific expenses incurred on the days dedicated purely to business activities. For S corporation owners, vehicle and travel deductions intersect directly with owner compensation audits. The IRS is actively targeting S corporations that pay owners minimal W-2 salaries to avoid payroll taxes while taking large corporate distributions.

Your salary must reflect “reasonable compensation” for your industry and role. Failing to balance this structure properly can lead the IRS to reclassify your distributions as wages, wiping out planned savings and exposing the business to back taxes, interest, and substantial penalties.

tax deductions

Frequently Asked Questions

What are the most common tax deductions small businesses miss?

Small business owners frequently miss tax deductions tied to localized operational costs, including home office internet allocations, localized vehicle mileage tracked via contemporaneous logs, and capital purchases managed via Section 179. Many also forfeit savings by using flat employee stipends instead of formalized, tax-free accountable plans, which converts clean deductions into taxable payroll liabilities.

How do I claim a deduction for a home office setup?

To claim home office tax deductions, your workspace must serve as your principal place of business and be used exclusively for commercial activities. You can calculate the deduction using the simplified method at five dollars per square foot up to 300 square feet, or the actual expense method to deduct a proportional percentage of rent, utilities, and insurance.

Are business meals fully deductible this year?

Business meals are not fully deductible; they are subject to a strict 50% limitation. To qualify for this partial write-off, the food and beverages must not be lavish or extravagant under the circumstances, and the owner or an employee must be present when the meal is provided to a client or prospect.

Can I deduct vehicle expenses using both mileage and actual costs?

You cannot combine both methods for a single vehicle within the same tax year; you must choose between the standard mileage rate or the actual expense method. If you select the standard mileage rate in the first year the car is available for use, you can switch to actual expenses later, but leasing structures lock you into your initial choice.

What software subscriptions qualify for a business write-off?

Any software subscription directly required to operate, market, or secure your company qualifies for a complete operational deduction. This includes accounting platforms, customer relationship management tools, web hosting, cybersecurity protocols, and specialized industry applications, provided they are used exclusively for your commercial operations.

How does the Section 179 deduction work for equipment purchases?

The Section 179 provision allows companies to deduct the complete purchase price of qualifying equipment and software up front, rather than depreciating the asset over several years. The equipment must be fully placed in service and functional within the business before midnight on December 31 of the filing year.

What is the difference between a tax deduction and a tax credit?

A tax deduction reduces your total taxable income, lowering the base upon which your liability is calculated based on your marginal bracket. A tax credit provides a dollar-for-dollar reduction of your final tax liability, making credits inherently more valuable than deductions when optimizing your overall financial return.

Can startup costs be deducted before the business officially opens?

The IRS allows entrepreneurs to deduct up to $5,000 of qualifying startup costs and an additional $5,000 of organizational costs in the year active operations begin. These upfront tax deductions phase out dollar-for-dollar if your total startup expenditures surpass the designated threshold, with any remaining balances amortized over a 180-month period.

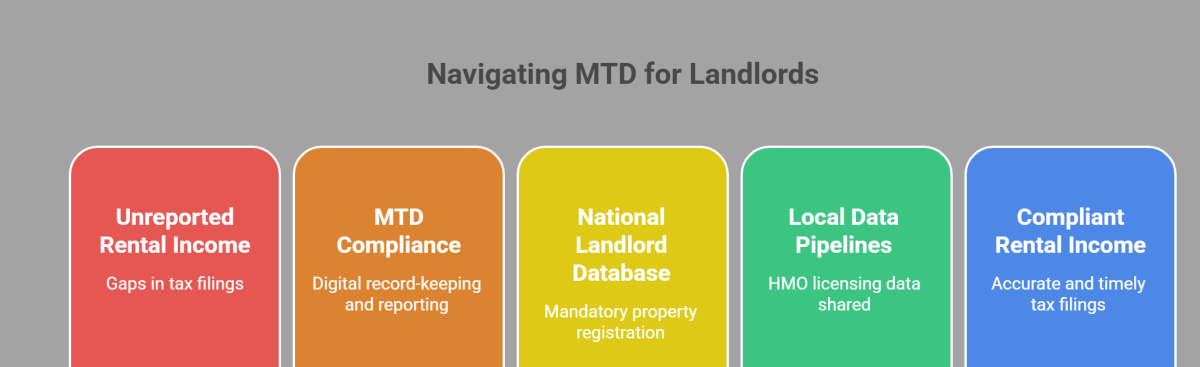

Reading Borough Council’s decision to expand its regulatory reach isn’t just about floor plans and fire doors. As of March 1, 2026, the HMO licensing Reading landscape shifted permanently with the introduction of borough-wide additional licensing. This move effectively brings 3 and 4-person shared houses into the same stringent oversight previously reserved for larger properties. While the council focuses on housing standards, the data generated by these applications provides the perfect fuel for HMRC’s “Connect” AI system.

HMRC is no longer relying on manual “nudge” letters. They’ve moved toward a digital net that cross-references local authority licensing registers with Land Registry data and Self-Assessment filings. If you’ve registered a property for HMO licensing Reading but haven’t declared a corresponding jump in rental income, the system flags the discrepancy automatically.

When you apply for a licence in Reading, you provide granular details: the number of occupants, the rent-bearing potential of each room, and the identities of all interested parties. This information is public. HMRC’s Connect system scours these public registers, pulling data from over 30 sources to build a financial profile of every landlord.

For those operating in Reading, the timing is particularly sharp. The rollout of the additional licensing scheme coincides with the first phase of Making Tax Digital (MTD) for Income Tax in April 2026. This creates a dual-pressure environment where landlords must prove physical compliance to the council while maintaining digital, quarterly records for the taxman.

Reading’s New Licensing Thresholds

Under the 2026 rules, almost any property in Reading with three or more unrelated tenants requires a licence. The council’s “Home Safe” portal requires identity documents, floor plans, and safety certificates.

Requirement

Mandatory Licensing (5+ persons)

Additional Licensing (3-4 persons)

Occupancy

5 or more people

3 to 4 people

Area Coverage

National / All of Reading

Borough-wide (from March 2026)

Application Fee

Two-stage (Part A & Part B)

Two-stage (Part A & Part B)

HMRC Visibility

High

High (via Public Register)

The trap for many is the assumption that “small” HMOs fly under the radar. In reality, the additional licensing register is often more scrutinized by tax authorities precisely because it captures landlords who historically operated in a “grey area” of tax reporting.

Why MTD for Income Tax Changes the Game

From April 6, 2026, landlords with a qualifying income over £50,000 must transition to MTD. This means no more annual scrambles to find receipts in January. You’ll need HMRC-compatible software to submit quarterly updates. This digital trail makes it nearly impossible to reconcile a licensed 5-bedroom HMO with a tax return that only shows income for a single-family let.

The council’s interest is your tenants’ safety; HMRC’s interest is your turnover. By securing a licence for HMO licensing Reading, you are effectively notifying the government that your property is generating higher-than-average yields. If your reported expenses or income figures don’t align with the market rates for a licensed HMO in the RG1 or RG2 postcodes, an inquiry is likely.

Avoiding the Compliance Squeeze

To survive this “digital net,” you need to treat your Reading HMO as a business, not a hobby. This starts with a “fit and proper person” assessment and ends with rigorous digital bookkeeping.

Audit your floor plans. Ensure your room sizes meet the 6.51 $m^2$ minimum for single adults.

Sync your data. Your licence application figures should match your MTD software entries exactly.

Prepare for the Part B fee. Reading’s fee structure is split; failing to pay the second part on time can invalidate your licence and alert the council’s enforcement team.

The goal is to remain invisible to HMRC’s AI by being perfectly visible and compliant on the council’s register. Discrepancies, not high income, trigger investigations.

FAQs: Your Guide to HMO Licensing Reading

Does a 3 bed house need an HMO licence in Reading?

Yes, as of March 1, 2026, a 3-bed house occupied by three or more unrelated people requires a licence under the additional HMO licensing Reading scheme. Previously, only larger properties with five or more occupants were mandated, but the new borough-wide designation has removed the “small HMO” exemption that many landlords relied on for years.

What are the HMO rules in Reading?

The rules for HMO licensing Reading require properties to meet strict safety and amenity standards. This includes minimum bedroom sizes (6.51 $m^2$ for one adult), annual gas safety checks, and five-yearly electrical inspections (EICR). Landlords must also ensure adequate kitchen and bathroom facilities relative to the number of tenants, alongside providing valid fire safety certifications.

What is the minimum room size for an HMO in Reading?

For HMO licensing Reading compliance, a room used for sleeping by one person aged 10 or over must have a floor area of at least 6.51 $m^2$. If two people over 10 share a room, the minimum increases to 10.22 $m^2$. Any floor area where the ceiling height is below 1.5 metres is excluded from these calculations.

Is Reading an Article 4 area for HMO?

Yes, large parts of Reading are subject to Article 4 Directions. This means you must obtain planning permission to convert a C3 (family home) into a C4 (small HMO), even before you apply for HMO licensing Reading. The licensing scheme and planning permissions are separate; having a licence does not mean you have the required planning consent.

How much is an HMO licence in Reading?

The cost for HMO licensing Reading varies based on the scheme and property size, typically ranging from £500 to over £1,500. Reading operates a two-stage fee system: Part A is paid upon application to cover processing, and Part B is due once the council intends to grant the licence, covering the ongoing management costs.

What happens if you don’t have an HMO licence in Reading?

Operating an unlicensed property subject to HMO licensing Reading is a criminal offence. Penalties include unlimited fines from the courts or civil penalties of up to £30,000 (£40,000 from May 2026). Furthermore, tenants can apply for a Rent Repayment Order (RRO) to reclaim up to 12 months of rent paid during the unlicensed period.

How many people can live in an HMO in Reading?

The maximum number of occupants is determined by the specific conditions of your HMO licensing Reading agreement. The council assesses the property’s size, room dimensions, and the number of available bathrooms and kitchens. You cannot exceed the number of “permitted persons” stated on the face of your issued licence without risking significant legal penalties.

How long does an HMO licence last in Reading?

A licence granted under the HMO licensing Reading framework typically lasts for up to five years. However, the council may grant a shorter licence if there are concerns about the management of the property or if the landlord has a history of non-compliance. You must apply for a renewal before the current licence expires to remain legal.

The landscape of UK buy-to-let has reached a “Big Bang” moment. With the Section 21 abolition officially taking effect as part of the Renters’ Rights Act 2025, the days of “no-fault” evictions are over. For landlords, this isn’t just a shift in tenancy management; it is a fundamental shift in tax compliance.

As the Let Property Campaign, I am here to guide you through this transition. The new legislation links your right to regain possession of your property directly to your status on the National Landlord Database, which functions as a direct data pipeline to HMRC. If you have undisclosed rental income, the window to “come clean” under favorable terms is closing fast.

The Death of Section 21 and the Rise of the Periodic Tenancy

On 1 May 2026, the Renters’ Rights Act 2025 fully takes effect, mandating the total abolition of Section 21 “no-fault” evictions. Furthermore, all tenancies are being converted into “periodic” or rolling agreements.

The National Landlord Database “Trap”

To serve a valid possession notice under these new rules—even for legitimate reasons like selling the property or moving back in—landlords must be registered on the new National Landlord Database.

The Data Link: This database is not just an administrative list; it is a direct data feed to HMRC.

The End of Ghost Landlording: It is now virtually impossible to legally manage a property or evict a tenant without your details being cross-referenced against HMRC’s “Connect” system.

Bridging the Gap: The Let Property Campaign

If the Section 21 abolition has made you realize that your tax affairs aren’t quite in order, the Let Property Campaign is your best route to compliance.

What is the Let Property Campaign?

It is a specific opportunity for individual landlords to disclose unpaid taxes on residential properties. By coming forward voluntarily, you secure more favorable terms—including lower penalties—than if HMRC finds you first through their new digital data pipelines.

Eligibility Criteria

You can use this campaign if you are an individual landlord (not a company or trust) renting out:

Single or multiple residential properties.

A room in your main home that exceeds the Rent a Room Scheme threshold.

Holiday lets or inherited properties.

UK property while living abroad.

The 3-Step Disclosure Roadmap

Step

Action

Key Deadline

1. Notify

Tell HMRC you intend to make a disclosure.

Immediately upon realizing the error.

2. Calculate

Work out tax, interest, and penalties for the relevant years.

90 days from notification.

3. Pay

Make a formal offer and pay the full amount electronically.

90 days from notification.

How Far Back Do You Need to Go?

The number of years you must disclose depends on why the tax wasn’t paid:

Reasonable Care: Maximum of 4 years.

Careless (Not taking reasonable care): Maximum of 6 years.

Deliberate: Up to 20 years.

2026: The Year of Digital Enforcement

The Section 21 abolition is just one piece of a larger enforcement puzzle.

Making Tax Digital (MTD)

Since 6 April 2026, MTD for Income Tax has been mandatory for landlords earning over £50,000. This requires quarterly digital reporting, meaning HMRC sees your financial data every three months rather than once a year.

Local Council Data Pipelines

Regional enforcement is also tightening. For example, Reading Borough Council now shares HMO licensing data directly with HMRC’s “Connect” system. Automated pipelines verify landlord identities and property details, leaving no room for “accidental” omissions.

Why Voluntary Disclosure is Non-Negotiable

If HMRC discovers your undisclosed income before you notify them, the consequences are severe:

Higher Penalties: Up to 100% for UK income or 200% for offshore income.

Criminal Risk: Potential for criminal prosecution and being named on the “deliberate defaulters” list.

By contrast, voluntary disclosure through specialists like Marslands Accountants can significantly reduce the burden. Marslands report helping landlords save an average of £7,000 on their final tax bill through the expert application of allowable expenses.

Frequently Asked Questions Section 21 abolition

1. What is the impact of the Section 21 abolition on current landlords?

The Section 21 abolition means you can no longer use “no-fault” notices to end tenancies. To gain possession, you must use specific grounds (like selling or moving in) and be registered on the National Landlord Database. This registration acts as a trigger for HMRC to verify your tax compliance and rental income history.

2. Can I still evict a tenant after the Section 21 abolition?

Yes, but the process is now more rigorous. You must provide a valid reason under the revised grounds for possession. Crucially, your legal standing to evict is tied to your transparency; if you aren’t registered on the National Landlord Database—which feeds into HMRC—your possession notices will likely be deemed invalid by the courts.

3. How does the National Landlord Database link to my taxes?

The database is a digital pipeline that shares your property and identity details directly with HMRC’s Connect system. Once you register to comply with the Section 21 abolition requirements, HMRC can automatically cross-reference your property holdings against your self-assessment filings to identify any gaps in reported rental income or capital gains.

4. What should I do if I haven’t declared rental income before 2026?

You should immediately notify HMRC via the Let Property Campaign. With the Section 21 abolition making “ghost landlording” impossible, a voluntary disclosure is the only way to avoid the maximum 100–200% penalties. Starting the process now allows you to settle unpaid taxes under the campaign’s more lenient voluntary terms.

5. How many years of back-tax will HMRC look at?

If you have been “careless,” HMRC typically goes back 6 years. However, if they deem the omission “deliberate”—which is easier to prove now with the Section 21 abolition and MTD providing digital trails—they can go back 20 years. Voluntary disclosure often helps limit the scope and penalty percentage compared to an HMRC-led inquiry.

6. What expenses are allowable in a Let Property Campaign disclosure?

You can deduct “wholly and exclusively” incurred costs such as repairs, insurance, and management fees. Expert accountants, like Marslands, often help landlords save an average of £7,000 by identifying overlooked allowable expenses. Ensuring these are calculated correctly is vital now that MTD requires quarterly digital transparency for many landlords.

7. Is the Let Property Campaign available for limited companies?

No, the campaign is strictly for individual landlords. If you operate your properties through a limited company and have undisclosed income, you cannot use these specific terms. However, with the Section 21 abolition affecting all residential tenancies, companies must also ensure their digital records match the National Landlord Database to remain compliant.

8. What happens if I ignore the new tax transparency rules?

Ignoring the rules while the Section 21 abolition is in effect is highly risky. HMRC’s “Connect” system now receives data from local councils, the National Landlord Database, and MTD. Failure to disclose can lead to penalties of up to 100%, public naming as a defaulter, and the loss of your legal right to manage or regain your property.

The April 2026 MTD deadline has arrived, marking the most significant shift in property taxation in a generation. For landlords in Reading and across the UK, the transition from annual Self Assessment to quarterly digital reporting is no longer a future concept—it is a mandatory legal requirement for those with qualifying income over £50,000.

As the Let Property Campaign, I am here to ensure you navigate this “Big Bang” moment without falling into the digital traps set by automated enforcement. If the sudden transparency of Making Tax Digital (MTD) has highlighted gaps in your previous filings, the Let Property Campaign remains your primary safety net for voluntary disclosure.

The 2026 Enforcement Trifecta

The April 2026 MTD rollout does not exist in a vacuum. It is part of a three-pronged enforcement strategy designed to eliminate “ghost landlording.”

MTD for Income Tax (Active 6 April 2026): Mandatory digital record-keeping and quarterly updates for landlords earning over £50,000.

National Landlord Database (Active 1 May 2026): Under the Renters’ Rights Act 2025, registration is mandatory to legally manage properties or serve possession notices.

Local Data Pipelines (Reading): Since 1 March 2026, Reading Borough Council has extended licensing to small HMOs (3-4 occupants), sharing this data directly with HMRC’s “Connect” system.

Understanding Qualifying Income for the April 2026 MTD Deadline

A common misconception is that the £50,000 threshold applies to profit. It does not. The April 2026 MTD rules apply to your gross qualifying income—the total rent received before any expenses are deducted.

Income Type

Included in Threshold?

Gross Rental Income (UK & Overseas)

Yes

Self-Employment Income

Yes

Furnished Holiday Lets

Yes

Jointly Owned Property Share

Individual Share Only

The Reading “Trap”: Additional Licensing Meets HMRC Connect

Landlords in Reading face a unique challenge. On 1 March 2026, the council’s Additional HMO Licensing scheme became active for properties with 3 or 4 occupants.

This is more than a safety check. This licensing data serves as a direct feed to HMRC. If you apply for a license in Reading but have not declared that rental income for previous years, the April 2026 MTD digital trail will likely trigger an automated tax enquiry.

Voluntary Disclosure via the Let Property Campaign

If the new digital landscape has made you realize your past filings were “careless” or incomplete, the Let Property Campaign allows you to “come clean” under favorable terms.

Reasonable Care: HMRC may only look back 4 years.

Careless: HMRC can investigate the last 6 years.

Deliberate: Up to 20 years of back-tax, interest, and penalties.

By notifying HMRC voluntarily, you avoid the maximum 100-200% penalties associated with prompted enquiries. Specialists like Marslands Accountants report saving landlords an average of £7,000 on their final bill by identifying valid allowable expenses that landlords often overlook.

Frequently Asked Questions

1. What is the impact of the Section 21 abolition on current landlords?

The Section 21 abolition, effective 1 May 2026, removes the ability to end tenancies without a specific reason. To regain possession, landlords must use new grounds and be registered on the National Landlord Database. This registration links directly to the April 2026 MTD framework, ensuring total tax transparency before any legal possession can be granted by the courts.

2. Can I still evict a tenant after the Section 21 abolition?

Yes, but you must use Section 8 grounds, such as the new Ground 1A for selling the property. However, your legal standing is now tied to compliance. If you are not registered on the National Landlord Database—which feeds into the April 2026 MTD data net—your eviction notices will likely be ruled invalid.

3. How does the National Landlord Database link to my taxes?

The database acts as a digital pipeline to HMRC’s “Connect” system. When you register to comply with the Renters’ Rights Act, HMRC cross-references your identity against your April 2026 MTD submissions. Any discrepancy between the properties you claim to manage and the income you report will trigger an immediate compliance check.

4. What should I do if I haven’t declared rental income before 2026?

You should immediately notify HMRC through the Let Property Campaign. With the April 2026 MTD deadline now active, “ghost landlording” is no longer viable. Making a voluntary disclosure before HMRC’s automated systems flag your Reading licensing data can significantly reduce your penalties and the risk of criminal prosecution.

5. How many years of back-tax will HMRC look at?

The look-back period depends on your behavior. If you were “careless,” HMRC typically reviews 6 years. If they deem the omission “deliberate”—a conclusion easier to reach given the April 2026 MTD digital requirements—they can go back 20 years. Voluntary disclosure is the best way to limit this window and secure lower penalty rates.

6. What expenses are allowable in a Let Property Campaign disclosure?

You can deduct “wholly and exclusively” incurred costs, such as property repairs, insurance, and management fees. In the context of the April 2026 MTD shift, keeping digital receipts for these expenses is vital. Specialists like Marslands often help landlords identify overlooked deductions, saving an average of £7,000 on their final settlement.

7. Is the Let Property Campaign available for limited companies?

No, the campaign is strictly for individual landlords. While companies are not eligible for these specific voluntary terms, they are still subject to the transparency brought by the April 2026 MTD era and the National Landlord Database. Companies with undisclosed income should seek professional advice to rectify their position outside of this specific campaign.

8. What happens if I ignore the new tax transparency rules?

Ignoring the April 2026 MTD and licensing rules is high-risk. HMRC’s “Connect” system now synthesizes data from MTD, the National Landlord Database, and Reading’s HMO licensing. Failure to comply can result in penalties up to 100% of the tax due, being named a “deliberate defaulter,” and losing the legal right to manage or evict tenants.

Note: For more information on making a disclosure, visit the official GOV.UK guide or contact felixaccountants for specialist support.

HMRC isn’t guessing anymore. Between the Land Registry, bank data, and even sites like Airbnb or Zoopla, the tax office has a digital map of who owns what and who’s likely collecting rent without telling them. If you own rental property in London, Slough, or the surrounding Thames Valley and haven’t fully disclosed your income, you’re sitting on a ticking financial clock and need to contact a Let Property Campaign Expert immediately. The Let Property Campaign is your one-way escape hatch, but navigating it alone is a recipe for overpaying or, worse, triggering a full-scale forensic audit.

Don’t wait for the letter to arrive. If you have undisclosed rental income in London, Slough, Windsor, Reading, or Oxford, taking the first step today is the only way to stay in control of your finances.

You’re about to learn exactly how the disclosure process works, why local market nuances in places like Windsor and Oxford matter to your tax bill, and how an expert ensures you pay the absolute legal minimum in penalties and interest.

What is a Let Property Campaign Expert?

A Let Property Campaign expert is a specialist tax advisor who manages the voluntary disclosure of undeclared rental income to HMRC. They calculate exact tax liabilities, identify all allowable property expenses to reduce the bill, and negotiate the lowest possible penalty percentages based on the landlord’s specific circumstances and “quality of disclosure.”

The Reality of HMRC Surveillance in the M4 Corridor

HMRC’s “Connect” system is an AI-driven database that cross-references billions of data points. For a landlord in Reading or London, this means HMRC knows when a property title changes, when a deposit is protected, and when a tenant claims housing benefits at your address.

The Let Property Campaign (LPC) is a specific opportunity for landlords who have failed to disclose their rental income to come forward. It’s not a “get out of jail free” card, but it is a “stay out of court” card. If you come to them before they send you a “nudge letter,” the penalties are significantly lower. If you wait until they find you, those penalties can reach 100% of the tax owed—or lead to criminal prosecution.

Why Location Matters: From Oxford Students to Slough Corporates

Your tax disclosure isn’t just about spreadsheets; it’s about the reality of your rental market. HMRC’s benchmarks for “reasonable” rental income vary wildly across the South East.

Oxford and Windsor: High-value areas with complex HMO (House in Multiple Occupation) setups or short-term holiday lets. These often involve higher management costs and maintenance fees that many landlords forget to deduct.

London and Slough: High churn rates and corporate lets. If you’ve had periods of vacancy or spent heavily on “repair vs. improvement” (a massive distinction in tax law), an expert ensures these are categorized to your advantage.

Reading: An area with high professional rental demand where landlords often move from a primary residence to a “buy-to-let” without realizing the CGT (Capital Gains Tax) implications of their future plans.

An expert understands that a £2,000 monthly rent in Slough looks different on a balance sheet than £5,000 in Kensington. They use local market data to justify your figures if HMRC questions the “commerciality” of your arrangements.

The Danger of the “DIY” in Let Property campaign Disclosure

Many landlords think the Let Property Campaign is as simple as filling out a form and cutting a check. It’s not. The biggest risk isn’t the tax itself; it’s the interest and the penalty classification.

HMRC classifies your “failure to notify” into three buckets:

Reasonable Excuse: You had a genuine reason (illness, bereavement) for not filing.

Careless: You didn’t take enough care to get it right.

Deliberate: You knew you owed tax and chose not to pay.

A DIY filer might accidentally admit to “deliberate” behavior through poor phrasing, or fail to argue for a “reasonable excuse.” An expert acts as a shield, framing your history in the most favorable light supported by evidence. They also ensure you aren’t paying tax on “capital” items that should actually be deducted from your future Capital Gains bill rather than your current Income Tax bill.

Step-by-Step: How an Expert Navigates Your Let Property campaign

Disclosure

1. The Portfolio Audit

Before speaking to HMRC, your advisor will reconstruct your financial history. This involves gathering bank statements, letting agent statements, and receipts for every tap fixed or wall painted over the last several years. They don’t just look for income; they hunt for “missing” expenses like mortgage interest (subject to Section 24 restrictions), insurance, and service charges.

2. The Notification Phase

Once the figures are ready, your expert notifies HMRC of your intent to disclose. This creates a “standstill” period of 90 days. During this time, you are protected from certain enforcement actions while the final report is prepared.

3. Technical Calculations

Calculating the tax is the easy part. The hard part is calculating the Section 24 interest relief and the tapered penalties. Since 2017, mortgage interest isn’t a direct deduction from rental income for individual landlords; it’s a 20% tax credit. Many DIY landlords still try to deduct the full interest, which is an immediate red flag for HMRC.

4. The Disclosure Submission

The final report is sent via the Official Government Gateway. This isn’t just a number; it’s a narrative. An expert includes a “disclosure letter” explaining why the omission happened, which is vital for minimizing penalties.

5. Payment and Settlement

Your expert helps arrange payment. If you can’t pay the full amount (which often happens when multiple years of back-tax are due), they negotiate a “Time to Pay” arrangement, allowing you to spread the cost without HMRC freezing your assets.

Comparison: Expert Disclosure vs. HMRC Discovery

Feature

Expert-Led Disclosure

HMRC Discovery (Audit)

Penalty Rate

Often 0% – 20%

35% – 100%+

Look-back Period

Limited by “reasonable care”

Up to 20 years

Control

You lead the narrative

HMRC dictates the investigation

Stress Level

Managed by professionals

High (legal/criminal threats)

Cost

Fixed fee + lower tax

Higher tax + compound interest + huge penalties

The “Repair vs. Improvement” Trap

This is where most London and Windsor landlords lose money. If you replace a broken wooden window with a double-glazed uPVC window, HMRC usually views that as a “repair” (deductible from income tax). If you build an extension or install a high-end designer kitchen where a basic one existed, that’s an “improvement” (deductible from Capital Gains Tax when you sell).

Without an HMRC Let Property Campaign expert in Slough or London, you might try to claim an extension against your rental income. HMRC will reject it, charge you a penalty for a “careless” error, and you’ll still owe the tax. An expert knows how to categorize these costs to maximize your current cash flow while protecting your future tax position.

Is it too late if I already received a Let Property campaign letter?

If you’ve received a “nudge letter” from HMRC mentioning the Let Property Campaign, the window for a “voluntary” disclosure is closing, but it isn’t shut. You can still use the campaign, but your penalty will likely be higher than if you had come forward unprompted. However, responding with a professional report from a London tax specialist shows HMRC that you are now taking your obligations seriously. This often prevents them from digging into other areas of your finances, like your primary business or offshore investments.

Strategy Framework: The Felix Approach to Let Property campaign

We don’t just crunch numbers. We look at the “Three Pillars of Protection”:

Documentation: Creating a “bulletproof” trail of expenses to offset income.

Mitigation: Arguing for the lowest possible penalty tier based on your life circumstances.

Future-Proofing: Setting up your digital records to comply with Making Tax Digital (MTD) for landlords, so you never end up in this position again.

Whether you’re a landlord with one flat in Reading or a portfolio in Oxford, the goal is the same: total compliance with minimum financial damage.

Further Reading on Let Property campaign

To better understand your specific situation, explore our dedicated regional guides:

How many years does the Let Property Campaign go back?

HMRC can go back up to 20 years if they believe the failure to pay was deliberate. If it was a “careless” mistake, they usually look back 6 years. If you took “reasonable care” but still got it wrong, the limit is typically 4 years. An expert helps determine which limit applies to you.

What are the penalties for the Let Property Campaign?

Penalties range from 0% to 100% of the tax owed. For voluntary disclosures where the landlord was “careless” but helpful, penalties are often between 0% and 15%. If HMRC finds you first, those rates jump significantly.

Can I include mortgage interest in my Let Property campaign disclosure?

Yes, but only according to the current rules. Since April 2020, you cannot deduct mortgage interest from your rental income to calculate profit. Instead, you receive a 20% tax credit. Failing to apply this correctly in a disclosure is a common reason HMRC rejects DIY submissions.

Do I have to pay the Let Property campaign full amount immediately?

Not necessarily. While HMRC prefers immediate payment, a Let Property Campaign expert can often negotiate a payment plan (Time to Pay arrangement) if you can demonstrate that a lump sum payment would cause “undue hardship.”

Does the Let Property campaign apply to holiday lets or Airbnb?

Yes. The Let Property Campaign covers all residential property, including specialized lets like Airbnb, student housing, and holiday rentals in areas like Oxford or Windsor. It does not cover commercial property (shops or offices).

What expenses can I claim to reduce my tax bill?

You can claim letting agent fees, property insurance, maintenance and repairs (not improvements), utility bills you paid, council tax during void periods, and professional fees like accountancy or legal costs related to the tenancies.

If you have undisclosed rental income, the sheer weight of “not knowing” is often worse than the tax bill itself. You might be wondering: How much do I actually owe? How far back will they go? Is there a way to estimate the damage before I talk to HMRC? This is where understanding the Let Property Campaign penalty calculator methodology becomes your most powerful tool. By learning how to calculate these figures, you move from a place of panic to a place of strategy.

In this guide, we will walk you through the exact process of using the Let Property Campaign framework to estimate your liabilities. We’ll cover the difference between tax, interest, and penalties, and provide a step-by-step roadmap to ensure you don’t pay a penny more than is legally required. Whether you are a landlord in Windsor, Oxford, or London, this manual is designed to give you total clarity.

Featured Snippet: What is the Let Property Campaign penalty calculator?

The Let Property Campaign penalty calculator is a framework used to estimate the total cost of disclosing unpaid rental tax. It combines the total tax owed per year, statutory interest (calculated from the date the tax was due), and a percentage-based penalty (0%–100%) determined by the taxpayer’s behavior and the timing of the disclosure.

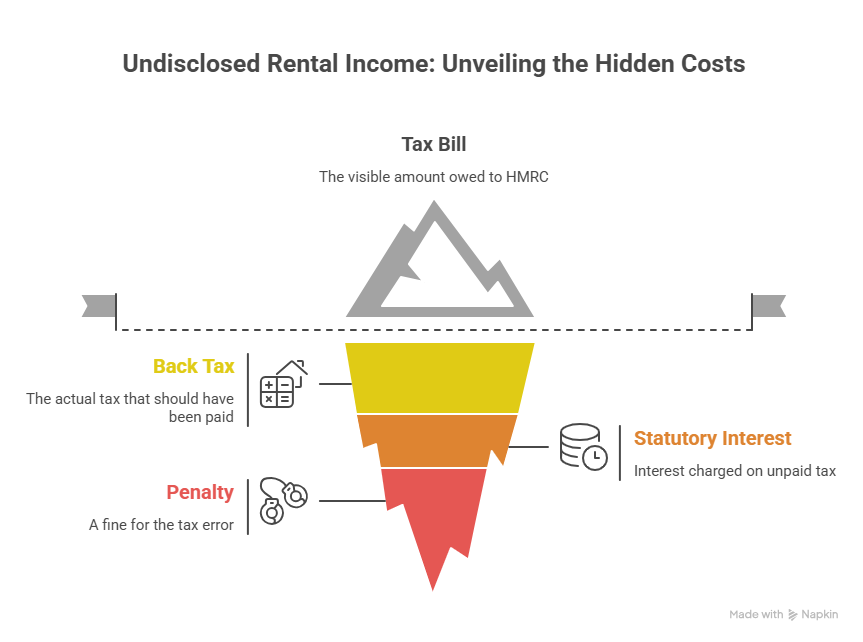

Understanding the “Cost” Pillars of a Disclosure

Before you start plugging numbers into a spreadsheet, you must understand that your final bill to HMRC isn’t just one number. It is built on three distinct pillars. If you miss one, your estimate will be dangerously low.

Pillar 1: The Back Tax (The Principal)

This is the actual amount of tax you should have paid on your rental profits. To find this, you must take your gross rental income and subtract “allowable expenses” (like repairs, insurance, and management fees). If you are a higher-rate taxpayer, you also need to account for the mortgage interest tax credit restrictions (Section 24).

Pillar 2: Statutory Interest

HMRC views unpaid tax as an interest-free loan you took from the government. To rectify this, they charge interest from the date the tax should have been paid until the date you actually pay it. With interest rates currently at decade-highs, this can add 20% or more to an old tax debt.

Pillar 3: The Penalty

This is the “fine” for the error. The percentage is applied to the tax amount (not the interest). This is the area where a specialist accountant provides the most value, as we can often argue for lower categories based on your circumstances.

Step-by-Step: How to Use the Penalty Calculator Framework

Since HMRC does not provide a single “one-click” calculator that handles every nuance, you must follow this structured framework to get an accurate estimate.

Step 1: Determine the Relevant Tax Years

How far back are you going?

4 Years: If you took “Reasonable Care” but made an honest mistake.

Note: Do not subtract the full mortgage payment. You can only deduct the interest element (and for individuals, this is now a 20% tax credit rather than a direct deduction from income).

Step 3: Determine Your Tax Band

Your rental profit is added to your other income (Salary, Dividends, etc.). If your total income crosses the £50,270 threshold (for 2025/26), you will owe 40% tax on the portion of rental profit sitting in the higher-rate band.

Step 4: Apply the Penalty Percentage

Use the table below to decide which percentage to apply to your tax total.

Behavior

Unprompted (You told them)

Prompted (They found you)

Reasonable Care

0%

0% – 30%

Careless

0% – 30%

15% – 30%

Deliberate

20% – 70%

35% – 70%

Step 5: Calculate Interest

You must apply the HMRC late payment interest rate to each year’s tax. Because rates change, it is best to use a specialized interest calculator or ask your HMRC Let Property Campaign expert in Slough to run the professional software.

Strategy Framework: Minimizing the “Penalty” Variable

The penalty is the only part of the equation that is negotiable. To minimize this, you must demonstrate the “Quality of Disclosure.”

Telling: Did you tell HMRC everything, or did you wait for them to ask?

Helping: Did you provide your spreadsheets and receipts quickly?

Giving Access: Did you allow HMRC to check your records?

Landlords in Reading and London who provide a “Full and Unprompted” disclosure can often see their penalties for carelessness reduced to 0%.

Real-World Example: The “Careless” Disclosure

Imagine a landlord in Oxford who didn’t declare £10,000 in rental profit per year for the last 4 years. They are a basic-rate (20%) taxpayer.

Tax Owed: £2,000 per year x 4 years = £8,000

Interest: (Estimate) £1,200

Penalty (Unprompted/Careless): Let’s say 10% = £800

Total Bill:£10,000

If this same landlord had waited for a “nudge letter,” the penalty could easily double or triple, and HMRC might insist on looking back 6 or 20 years instead of 4.

Pros and Cons of DIY Calculation vs. Professional Assistance

DIY Calculation

Pros: Free; gives a rough “ballpark” figure immediately.

Cons: High risk of missing tax credits; often results in overpaying tax or underestimating penalties; no protection if HMRC challenges the figures.

Professional Specialist (Felix & Co.)

Pros: Access to professional-grade Let Property Campaign penalty calculator software; expert negotiation of penalty categories; identifying obscure allowable expenses (e.g., specific proportions of home office/travel).

Cons: Upfront accountant fee. However, the tax savings usually far exceed the fee.

Why Location Matters: High-Value Service Areas