This VAT and property UK guide 2025 explains when VAT applies to residential and commercial property, how VAT recovery works, and when landlords should consider opting to tax.. Many investors assume it simply doesn’t apply to residential letting — and for standard long-term lettings they are correct — but this assumption becomes expensive the moment they venture into commercial property, development projects, or short-term letting.

The Four VAT Categories for Property Transactions

VAT Category

What It Means

Property Examples

VAT Recovery on Costs?

Exempt

No VAT charged on income; no VAT recovered on costs

Standard residential letting, sale of existing residential property

No

Zero-rated (0%)

No VAT charged on income; full VAT recovered on costs

Construction/first sale of new dwellings

Yes — full recovery

Reduced rate (5%)

VAT at 5% charged; costs partially recoverable

Certain conversions of non-residential to residential

Yes — at 5% rate

Standard-rated (20%)

VAT at 20% charged; full recovery on costs

New commercial premises, opted-to-tax properties

Yes — full recovery

The Critical Distinction: Exempt vs Zero-Rated

Both categories result in zero VAT being charged to the customer — but the difference in financial outcome is enormous. Exempt = you cannot recover VAT you paid on your costs. Zero-rated = you can recover all VAT you paid on costs. For a £500,000 development project, this difference can be £80,000–£100,000.

VAT and Property UK: Residential Property Rules

The letting or sale of existing residential property is generally exempt from VAT. This means you charge no VAT on rent or sale proceeds, but you also cannot reclaim VAT incurred on repairs, maintenance, or professional fees.

However, newly built dwellings are zero-rated when first sold or let on a long lease. A developer building residential units from bare land can reclaim all VAT on construction costs and professional services — a powerful financial advantage that must be structured correctly from the outset.

VAT and Property UK: Commercial Property and the Option to Tax

Commercial property transactions are generally standard-rated at 20%. However, older commercial properties (3+ years old) are exempt by default unless the owner makes an Option to Tax election (HMRC form VAT1614A).

When to Consider Opting to Tax

You have incurred substantial VAT on refurbishment or development of commercial property

Your tenants are VAT-registered and can recover the VAT you charge them

You intend to sell the property and the buyer is VAT-registered

You want to prevent irrecoverable VAT from eroding your returns

Option to Tax Warning

An Option to Tax, once made, normally lasts 20 years and cannot easily be revoked. If you option a property and then let it to an unregistered business (a GP surgery, charity, or small retailer, for example), your VAT charge will increase their costs with no recovery possible — making your property less competitive.

VAT and Property UK: Transfer of a Going Concern (TOGC)

A TOGC applies when a property rental business is sold as a going concern, with tenants in place and the buyer continuing the same letting activity. When conditions are met, the sale is outside the scope of VAT entirely — no VAT is charged and the buyer avoids paying large amounts up front. Both parties must be VAT-registered and the seller must have opted to tax (where applicable).

Serviced Accommodation and Short-Term Lets

Short-term holiday accommodation and serviced apartments are treated as standard-rated supplies (20% VAT). Once turnover exceeds £90,000 (2025 threshold), VAT registration is mandatory. This allows recovery of VAT on cleaning, utilities, and maintenance — but requires charging 20% on income.

Do I need to register for VAT if I only let residential property?

No. Residential lettings are exempt from VAT, so rental income does not count towards the £90,000 registration threshold. You would only need to register if you have additional taxable income streams (e.g. commercial lets, serviced accommodation) that collectively exceed the threshold.

What is the option to tax and should I use it?

The option to tax converts an otherwise exempt commercial property into a standard-rated supply, allowing you to recover VAT on costs. It is beneficial when your tenants are VAT-registered and can recover the VAT, or when you have substantial development costs you want to reclaim. It is less suitable for mixed commercial/residential use or where tenants are unregistered.

Can I recover VAT on costs for a new-build residential development?

Yes. The construction and first sale of new dwellings is zero-rated, meaning you charge no VAT on the sale but can reclaim all VAT incurred on construction, professional fees, and materials. This is a significant cash-flow and cost benefit for residential developers.

What is TOGC and how does it save VAT?

Transfer of a Going Concern (TOGC) applies when a property rental business is sold with tenants in occupation and the buyer continues the same business. The sale falls outside VAT scope, meaning no VAT is charged and the buyer doesn’t pay VAT on the purchase price. Both parties must be VAT-registered for it to apply.

Does VAT apply to mixed-use development projects?

Mixed-use buildings (e.g. ground-floor commercial with flats above) require a partial exemption calculation. You can only recover the proportion of input VAT that relates to your taxable (commercial or opted-to-tax) income stream. Professional VAT advice at the planning stage is essential.

This VAT and property UK guide 2025 highlights why understanding exempt, zero-rated and standard-rated transactions is essential before making property investment or development decisions.VAT planning decisions made before the first invoice save far more than corrections made afterwards. Book your consultation with Felix Accountants.

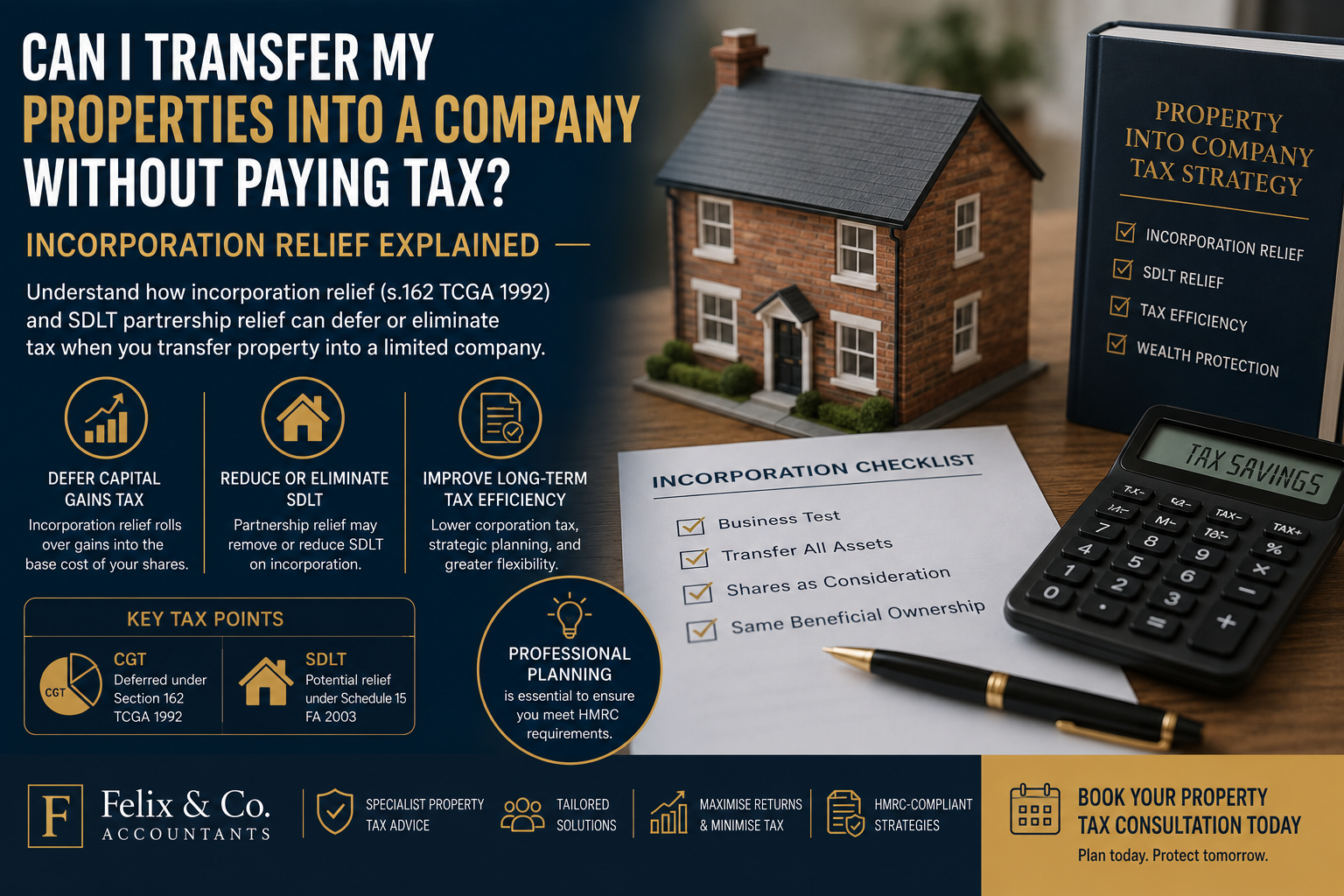

Many landlords ask whether they can transfer property into a limited company without paying tax in the UK. While incorporation can improve long-term tax efficiency, the transfer itself is treated as a disposal for tax purposes and may trigger Capital Gains Tax (CGT) and Stamp Duty Land Tax (SDLT). However, incorporation relief and SDLT partnership relief can significantly reduce or defer these charges when the correct conditions are met.

What Happens When You Transfer Property Into a Limited Company?

HMRC treats an incorporation as if you sold the properties to the company at market value, and the company simultaneously bought them at that same value. Two tax charges therefore arise simultaneously:

Tax Charge

Who Pays

Basis of Calculation

Capital Gains Tax (CGT)

You (the individual)

Market value minus original acquisition cost and improvements

Stamp Duty Land Tax (SDLT)

The company

Market value of the property, potentially with 3% surcharge

Incorporation Relief (Section 162 TCGA 1992)

This relief defers the capital gain that would otherwise crystallise on transfer. Instead of paying CGT immediately, the gain is ‘rolled over’ into the base cost of the shares you receive in the new company. No tax is paid now — it is deferred until you eventually sell the shares.

Four Conditions to Transfer Property Into a Limited Company Without Paying Tax

Condition

Requirement

Practical Implication for Landlords

1. A business must exist

Transferring a business, not merely an investment

Passive rent collection rarely qualifies — active management is required

2. Whole business transferred

All assets (except cash) must transfer together

All properties, leases, and contracts move to the company

3. Shares received as consideration

Transfer is wholly or partly in exchange for shares

You receive shares equal in value to net assets transferred

4. Same beneficial ownership

Proportional share allocation

Co-owners receive shares in the same ratio as their property interests

The Business Test — Ramsay v HMRC [2013]

The Upper Tribunal confirmed in Ramsay v HMRC [2013] UKUT 0226 (TCC) that ‘mere ownership and rent collection is not sufficient’ to constitute a business. HMRC expects: 4+ properties, 20+ hours per week of active management, organised systems, third-party services, and documented activity records.

How the CGT Deferral Works: A Worked Example

Step

Amount

Original portfolio purchase price

£600,000

Current market value

£1,000,000

Potential capital gain

£400,000

CGT payable without relief (at 24%)

£96,000

CGT with incorporation relief

£0 — deferred into share base cost

Base cost of shares issued

£600,000 (market value £1m minus deferred gain £400k)

SDLT Partnership Relief (Schedule 15 FA 2003)

Even where CGT is deferred, the company acquiring the property may owe SDLT. However, where the properties were held in a genuine business partnership, Schedule 15 of the Finance Act 2003 can eliminate or significantly reduce this SDLT charge.

Pre-Incorporation Ownership

SDLT on Incorporation

Sole ownership

Full SDLT on market value (including 3% surcharge)

Genuine partnership (e.g. husband and wife)

Potential SDLT relief if partnership existed as a business before incorporation

LLP converting to Ltd Co

Relief may apply depending on continuity of ownership

Critical Requirement for Partnership Relief

HMRC expects formal evidence of the partnership before incorporation: a partnership tax return (SA800), a separate bank account in the partnership name, and documented partnership accounts. Without this evidence, HMRC will deny relief and charge full SDLT on the market value.

Director’s Loan Account Benefit

Where the company assumes your outstanding mortgage, this creates a Director’s Loan Account (DLA) in your favour — equivalent to the equity you transferred. This balance can be drawn back from the company completely tax-free, providing an additional extraction route post-incorporation.

Do I pay CGT when I transfer my properties into a limited company?

Not immediately, if incorporation relief (s.162 TCGA 1992) applies. The gain is deferred into the base cost of your shares. However, the business test must be met — passive ownership does not qualify.

What CGT rate applies on eventual disposal of the shares?

Disposal of shares in a close company holding investment property will typically be subject to CGT at 20% (higher-rate taxpayers) under current rules. Business Asset Disposal Relief at 10% is unlikely to apply to purely investment portfolios.

What is the minimum number of properties needed for incorporation relief?

There is no statutory minimum, but HMRC and tribunal decisions suggest that four or more properties, combined with significant management activity (20+ hours/week), typically constitute a business for relief purposes.

Can I refinance the mortgages when I incorporate?

Existing lenders must consent to transfer their mortgages from personal to company name. Most residential buy-to-let lenders will require a full application and will charge arrangement fees. Bridging finance is sometimes used to facilitate the transition.

Is there a deadline for incorporating my portfolio?

There is no statutory deadline, but the sooner you incorporate (where it is beneficial), the sooner you benefit from lower corporation tax on profits. Additionally, the longer you wait, the larger the deferred gain that will crystallise on eventual share disposal.

Before you transfer property into a limited company, it is important to review both the CGT and SDLT implications.. Book a consultation with Felix Accountants to stress-test your position before you commit.

Once you have a property company generating profits, the next strategic question is equally important: how do you get the money out efficiently? Paying yourself incorrectly can convert a corporation-tax saving into a personal income-tax disaster. This article sets out the 2025/26 rules and the optimal approach for property company directors.

Property Company Corporation Tax: What Comes First?

Your company must settle its HMRC corporation tax liability before distributions can be made. For periods from 1 April 2025: 19% applies to profits up to £50,000 (small profits rate); 25% applies to profits above £250,000 (main rate); and marginal relief applies between £50,001 and £250,000.

Taking a Salary from Your Property Company

A salary is the company’s deductible expense — it reduces the taxable profit and therefore the corporation tax bill. However, it attracts both employer’s (13.8%) and employee’s (8% or 2%) National Insurance Contributions.

The Optimal Salary Strategy

Many property company directors pay themselves a salary at the National Insurance Lower Earnings Limit (£6,396 for 2025/26) to retain state benefit entitlement, or at the Personal Allowance level (£12,570) to minimise total NIC cost. A salary of £12,570 avoids employee NIC while still triggering employer NIC — a specialist accountant will run the precise numbers.

Taking Dividends from a Property Company

Dividends are paid from post-corporation-tax profits. They are not subject to NICs, making them more efficient than salary for most director-shareholders. However, they do not reduce the company’s corporation tax bill.

Tax Band

Income Range (2025/26)

Dividend Tax Rate

Basic rate

Up to £50,270

8.75%

Higher rate

£50,271 – £125,140

33.75%

Additional rate

Above £125,140

39.35%

Dividend allowance

First £500 of dividends

0%

Property Company Pension Contributions

Employer pension contributions paid by the company are deductible before corporation tax — and they are not a benefit-in-kind for the director receiving them. This makes pension contributions arguably the most tax-efficient extraction method available.

Company deducts contribution: saves 19–25% corporation tax

No income tax or NICs on the contribution going in

Growth within the pension is free from income tax and CGT

Annual allowance: £60,000 per individual (2025/26), reduced under tapering for high earners

Optimising Your Extraction Mix: The Three-Layer Approach

Layer

Method

Why It Works

Layer 1

Small salary (£6,396–£12,570)

Preserves state benefit entitlement; company gets deduction

Layer 2

Pension contributions (up to £60,000)

Maximum corp tax deduction; no personal tax now

Layer 3

Dividends (remaining profit)

Lower effective rate than employment income; no NICs

Compliance Requirements

Dividends require board minutes documenting the declaration — even if you are sole director

Dividends can only be paid from distributable (post-tax) reserves — not from projected future profits

PAYE must be registered and returns filed in real time via RTI if any salary is paid

Family shareholder arrangements must not fall foul of the settlement rules (S.619 ITTOIA 2005)

Is it better to take salary or dividends from my property company?

In most cases, a combination is most efficient: a low salary (£6,396–£12,570) to preserve state benefits and create a corporation tax deduction, then dividends for the remainder. Pension contributions should be maximised before dividends are considered.

Can I pay my spouse a salary or dividends from my property company?

Yes, provided they hold shares or perform genuine work. Dividend distribution to spouse-shareholders is permissible but subject to the settlement rules if their shares do not carry genuine rights. Take professional advice before structuring family arrangements.

What are distributable reserves and why do they matter?

Distributable reserves are accumulated after-tax profits that can legally be paid as dividends. If your company has made losses or hasn’t yet produced accounts, a dividend paid without distributable reserves is unlawful and may be reclassified as a loan to the director.

How much can my company pay into my pension each year?

There is no company contribution limit per se, but total pension input (employer plus employee) must not exceed the annual allowance — £60,000 for 2025/26 — nor exceed the individual’s relevant UK earnings if claiming personal tax relief. Company employer contributions bypass the earnings cap.

What happens if I draw too much from the company?

Drawings without a corresponding salary, dividend, or loan agreement create an overdrawn director’s loan account. If this exceeds £10,000 or is not repaid within nine months of the year-end, Section 455 tax (33.75%) is charged on the outstanding balance.

Understanding the most tax-efficient way to extract profits from a property company can save thousands in tax over time. Book a consultation with Felix Accountants today.

For a property investor, claiming every allowable expense is one of the most straightforward routes to improving net returns — no new strategy required, just disciplined record-keeping and a clear understanding of HMRC rules. Yet surveys consistently show that landlords underclaim, leaving significant tax savings unclaimed each year.

The Core Rule: ‘Wholly and Exclusively’

Under HMRC’s Property Income Manual (PIM2010), an expense is deductible only if it is incurred wholly and exclusively for the purpose of letting the property. A dual-purpose cost — partly personal, partly business — is either apportioned or disallowed entirely depending on the nature of the expense.

Example: Apportionment in Practice

If your mobile phone is used 60% for property management and 40% personally, you may claim 60% of the annual contract cost. Broadband costs, home-office costs, and vehicle use can be treated similarly — but HMRC will challenge estimates that cannot be substantiated.

Allowable Expenses Every Property Investor Can Claim

Expense Category

What Is Deductible

HMRC Reference

Repairs & maintenance

Routine repairs to restore original condition (e.g. fixing boiler, repainting, replacing broken windows)

Lease renewals under 1 year, pursuing rent arrears, accountancy fees

PIM2135

Utilities paid by landlord

Gas, electricity, water, broadband, council tax if borne by landlord

PIM2110

Advertising costs

Online listings, photography, ‘to let’ boards

PIM2065

Ground rent & service charges

If leasehold property, these are deductible

PIM1070

Replacement of domestic items

Like-for-like replacement of furniture, white goods (Replacement Domestic Items Relief)

PIM3210

Section 24 Tax Rules for Property Investors

Individual landlords cannot fully deduct mortgage interest. Since 6 April 2020, the restriction has been at 100% — you receive only a 20% tax credit on finance costs. This makes holding property personally significantly less efficient for higher-rate taxpayers.

Ownership Type

Finance Cost Treatment

Example: £10,000 Interest, 40% Taxpayer

Personal ownership

20% tax credit only

Tax saved: £2,000 (not £4,000)

Limited company

Full deduction before corporation tax

Tax saved: £2,500 (at 25% CT)

Capital vs Revenue — A Critical Distinction

Not everything that costs money on a property is deductible as a revenue expense. Capital expenditure — improvements that enhance the property beyond its original state — is not deductible against rental income. It may, however, be added to the base cost of the property for CGT purposes on eventual disposal.

Revenue (Deductible) vs Capital (Not Deductible)

Replacing a broken boiler with an equivalent model = revenue (deductible)

Installing an air-source heat pump in a property that had none = capital (not deductible)

Repainting and patching walls = revenue (deductible)

Extending the kitchen = capital (add to base cost for CGT)

The £1,000 Property Income Allowance

Individuals with gross rental income below £1,000 need not report it. Where income is slightly above this, they can opt to use the allowance instead of claiming actual expenses — but not both simultaneously. For most active landlords with genuine costs, detailed expenses will produce a better result.

Property Investor Expense Checklist

Before year-end: (1) collect all invoices and receipts, (2) reconcile bank statements, (3) apportion dual-purpose costs, (4) calculate total finance costs separately, (5) identify any missed capital items for CGT records, (6) review whether any losses can be carried forward.

Expenses Property Investors Cannot Claim

Capital mortgage repayments (only the interest element qualifies for the 20% credit)

Personal insurance not connected to the letting business

Improvements and extensions to the property

Costs relating to personal occupation periods in a let property

Can I deduct my mortgage payments from rental income?

No. Capital repayments are never deductible. For individually-owned properties, you receive a 20% tax credit on the interest portion only. Limited companies can deduct the full interest before corporation tax.

Is travel to inspect my property tax-deductible?

Yes, provided the travel is wholly and exclusively for the purpose of managing or inspecting the property. Personal commuting or journeys with a dual purpose cannot be claimed. Keep a mileage log with dates and reasons.

Can I claim accountancy fees as a property expense?

Yes. Accountancy and bookkeeping fees directly related to your rental business are allowable under PIM2135. Fees for personal tax matters unrelated to the property are not.

What is Replacement Domestic Items Relief?

This relief (introduced in 2016) allows landlords to deduct the cost of replacing furnishings and domestic appliances with equivalent items. It applies to residential let properties and replaces the old Wear and Tear Allowance.

Can I carry forward a property loss?

Yes. If allowable expenses exceed rental income in a tax year, the resulting loss is carried forward against future rental income from the same property business. It cannot offset general earned income unless the activity qualifies as a trade.

Understanding allowable expenses is one of the easiest ways for a property investor to reduce their tax bill legally.

One of the most consequential decisions any UK property investor faces is deceptively simple to state: should you buy property in your personal name, through a limited company, or via a Limited Liability Partnership (LLP)? The answer will shape your tax bill, your mortgage options, your estate planning, and your long-term wealth for decades. This guide sets out the 2025/26 framework clearly so you can make the right call for your circumstances.

Key Insight

At 2025 rates, a basic-rate taxpayer might save very little by incorporating — but a higher-rate investor with four or more properties and long-term reinvestment plans could save tens of thousands in tax annually through a corporate structure.

The 2025/26 UK Property Tax Landscape

Before choosing a structure, understand the current rates that frame the decision.

Tax Type

Rate (2025/26)

Applies To

Corporation tax

19% (profits ≤£50k) — 25% (profits >£250k)

Limited companies

Income tax

20% / 40% / 45%

Individual landlords

Dividend tax

8.75% / 33.75% / 39.35% (£500 free)

Company profit extraction

Mortgage interest relief

20% tax credit only

Individual landlords

SDLT surcharge

3% on additional dwellings

All investors

Option 1: Should I Buy Property in Your Personal Name?

Advantages

No Companies House filings, statutory accounts, or director duties

Rental profits are directly accessible — no dividend procedures

Broader mortgage market with often better rates for individuals

Personal allowance (£12,570) means the first portion of profit may be tax-free

Disadvantages

Rental profits above £50,270 are taxed at 40–45% income tax

Mortgage interest relief restricted to a 20% tax credit (Section 24, Finance Act 2015)

Full property value sits in your IHT estate at 40% above the nil-rate band

Fewer mortgage lenders; rates typically 0.5–1% higher

Annual accounts, CT600, and Companies House compliance required

Option 3: Should I Buy Property Through an LLP?

An LLP blends the limited liability of a company with the tax transparency of a partnership. Profits flow directly to members and are taxed at their personal rates — but full interest deduction is available where HMRC accepts the activity as a genuine property business.

Factor

Personal Ownership

Limited Company

LLP

Tax on profits

20–45% income tax

19–25% corp tax + dividend tax on extraction

Members’ personal tax 20–45%

Interest relief

20% tax credit only

Fully deductible

Deductible if business activity proven

Reinvestment potential

Taxed first, then reinvest

Reinvest at 19–25% CT rate

Taxed on members before reinvestment

Succession planning

Complex — CGT/SDLT on transfer

Shares transferable flexibly

New members easily added

Administration

Low

Moderate to high

Moderate

Which Structure Is Right for You?

Run these five questions before deciding:

Will I live off the income now, or reinvest for portfolio growth?

Am I investing alone or with a partner, spouse, or family?

How important is limiting personal liability?

Do I intend to pass the portfolio to family?

Is this buy-to-let, serviced accommodation, or active development?

Felix’s Practical Tip

Start with the end in mind. The structure you choose today determines how easily you can borrow, grow, and eventually pass on your wealth. Once you hold multiple properties personally, restructuring is expensive — SDLT and CGT can bite hard. Choose for the future, not for today’s convenience.

Frequently Asked Questions on How to Buy Property in the UK

Is it better to buy property in my own name or through a company in 2025?

For higher-rate taxpayers planning long-term portfolio growth, a limited company typically provides superior tax efficiency through lower corporation tax rates and full mortgage interest deduction. Personal ownership is simpler and may suffice for one or two properties with low gearing.

Can I move properties from my personal name into a company?

Yes, but this is treated as a disposal at market value, potentially triggering CGT and SDLT. Incorporation Relief (s.162 TCGA 1992) can defer CGT if the activity qualifies as a business. See our dedicated guide at felixaccountants.com/transfer-property-into-company-without-paying-tax/

What is Section 24 and does it affect my decision on how to buy property?

Section 24 (Finance Act 2015) restricts individual landlords to a 20% tax credit on mortgage interest rather than a full deduction. Limited companies are unaffected. This restriction is often the primary driver for incorporation decisions.

Does an LLP pay corporation tax when they buy property?

No. An LLP is tax-transparent — profits are allocated directly to members and taxed at their personal income tax rates. This means no corporation tax at entity level, but also no benefit from the lower 19–25% corporate rates.

What SDLT surcharge applies when you buy property through a company?

Companies purchasing residential property for £500,000 or more face a flat 15% SDLT rate unless the property is held for genuine letting or development purposes. The standard 3% additional-dwelling surcharge also applies to corporate purchases below that threshold.

Ready to choose the right structure? Let Felix Accountants map out your optimal ownership model.

HMRC isn’t guessing anymore. Between the Land Registry, bank data, and even sites like Airbnb or Zoopla, the tax office has a digital map of who owns what and who’s likely collecting rent without telling them. If you own rental property in London, Slough, or the surrounding Thames Valley and haven’t fully disclosed your income, you’re sitting on a ticking financial clock and need to contact a Let Property Campaign Expert immediately. The Let Property Campaign is your one-way escape hatch, but navigating it alone is a recipe for overpaying or, worse, triggering a full-scale forensic audit.

Don’t wait for the letter to arrive. If you have undisclosed rental income in London, Slough, Windsor, Reading, or Oxford, taking the first step today is the only way to stay in control of your finances.

You’re about to learn exactly how the disclosure process works, why local market nuances in places like Windsor and Oxford matter to your tax bill, and how an expert ensures you pay the absolute legal minimum in penalties and interest.

What is a Let Property Campaign Expert?

A Let Property Campaign expert is a specialist tax advisor who manages the voluntary disclosure of undeclared rental income to HMRC. They calculate exact tax liabilities, identify all allowable property expenses to reduce the bill, and negotiate the lowest possible penalty percentages based on the landlord’s specific circumstances and “quality of disclosure.”

The Reality of HMRC Surveillance in the M4 Corridor

HMRC’s “Connect” system is an AI-driven database that cross-references billions of data points. For a landlord in Reading or London, this means HMRC knows when a property title changes, when a deposit is protected, and when a tenant claims housing benefits at your address.

The Let Property Campaign (LPC) is a specific opportunity for landlords who have failed to disclose their rental income to come forward. It’s not a “get out of jail free” card, but it is a “stay out of court” card. If you come to them before they send you a “nudge letter,” the penalties are significantly lower. If you wait until they find you, those penalties can reach 100% of the tax owed—or lead to criminal prosecution.

Why Location Matters: From Oxford Students to Slough Corporates

Your tax disclosure isn’t just about spreadsheets; it’s about the reality of your rental market. HMRC’s benchmarks for “reasonable” rental income vary wildly across the South East.

Oxford and Windsor: High-value areas with complex HMO (House in Multiple Occupation) setups or short-term holiday lets. These often involve higher management costs and maintenance fees that many landlords forget to deduct.

London and Slough: High churn rates and corporate lets. If you’ve had periods of vacancy or spent heavily on “repair vs. improvement” (a massive distinction in tax law), an expert ensures these are categorized to your advantage.

Reading: An area with high professional rental demand where landlords often move from a primary residence to a “buy-to-let” without realizing the CGT (Capital Gains Tax) implications of their future plans.

An expert understands that a £2,000 monthly rent in Slough looks different on a balance sheet than £5,000 in Kensington. They use local market data to justify your figures if HMRC questions the “commerciality” of your arrangements.

The Danger of the “DIY” in Let Property campaign Disclosure

Many landlords think the Let Property Campaign is as simple as filling out a form and cutting a check. It’s not. The biggest risk isn’t the tax itself; it’s the interest and the penalty classification.

HMRC classifies your “failure to notify” into three buckets:

Reasonable Excuse: You had a genuine reason (illness, bereavement) for not filing.

Careless: You didn’t take enough care to get it right.

Deliberate: You knew you owed tax and chose not to pay.

A DIY filer might accidentally admit to “deliberate” behavior through poor phrasing, or fail to argue for a “reasonable excuse.” An expert acts as a shield, framing your history in the most favorable light supported by evidence. They also ensure you aren’t paying tax on “capital” items that should actually be deducted from your future Capital Gains bill rather than your current Income Tax bill.

Step-by-Step: How an Expert Navigates Your Let Property campaign

Disclosure

1. The Portfolio Audit

Before speaking to HMRC, your advisor will reconstruct your financial history. This involves gathering bank statements, letting agent statements, and receipts for every tap fixed or wall painted over the last several years. They don’t just look for income; they hunt for “missing” expenses like mortgage interest (subject to Section 24 restrictions), insurance, and service charges.

2. The Notification Phase

Once the figures are ready, your expert notifies HMRC of your intent to disclose. This creates a “standstill” period of 90 days. During this time, you are protected from certain enforcement actions while the final report is prepared.

3. Technical Calculations

Calculating the tax is the easy part. The hard part is calculating the Section 24 interest relief and the tapered penalties. Since 2017, mortgage interest isn’t a direct deduction from rental income for individual landlords; it’s a 20% tax credit. Many DIY landlords still try to deduct the full interest, which is an immediate red flag for HMRC.

4. The Disclosure Submission

The final report is sent via the Official Government Gateway. This isn’t just a number; it’s a narrative. An expert includes a “disclosure letter” explaining why the omission happened, which is vital for minimizing penalties.

5. Payment and Settlement

Your expert helps arrange payment. If you can’t pay the full amount (which often happens when multiple years of back-tax are due), they negotiate a “Time to Pay” arrangement, allowing you to spread the cost without HMRC freezing your assets.

Comparison: Expert Disclosure vs. HMRC Discovery

Feature

Expert-Led Disclosure

HMRC Discovery (Audit)

Penalty Rate

Often 0% – 20%

35% – 100%+

Look-back Period

Limited by “reasonable care”

Up to 20 years

Control

You lead the narrative

HMRC dictates the investigation

Stress Level

Managed by professionals

High (legal/criminal threats)

Cost

Fixed fee + lower tax

Higher tax + compound interest + huge penalties

The “Repair vs. Improvement” Trap

This is where most London and Windsor landlords lose money. If you replace a broken wooden window with a double-glazed uPVC window, HMRC usually views that as a “repair” (deductible from income tax). If you build an extension or install a high-end designer kitchen where a basic one existed, that’s an “improvement” (deductible from Capital Gains Tax when you sell).

Without an HMRC Let Property Campaign expert in Slough or London, you might try to claim an extension against your rental income. HMRC will reject it, charge you a penalty for a “careless” error, and you’ll still owe the tax. An expert knows how to categorize these costs to maximize your current cash flow while protecting your future tax position.

Is it too late if I already received a Let Property campaign letter?

If you’ve received a “nudge letter” from HMRC mentioning the Let Property Campaign, the window for a “voluntary” disclosure is closing, but it isn’t shut. You can still use the campaign, but your penalty will likely be higher than if you had come forward unprompted. However, responding with a professional report from a London tax specialist shows HMRC that you are now taking your obligations seriously. This often prevents them from digging into other areas of your finances, like your primary business or offshore investments.

Strategy Framework: The Felix Approach to Let Property campaign

We don’t just crunch numbers. We look at the “Three Pillars of Protection”:

Documentation: Creating a “bulletproof” trail of expenses to offset income.

Mitigation: Arguing for the lowest possible penalty tier based on your life circumstances.

Future-Proofing: Setting up your digital records to comply with Making Tax Digital (MTD) for landlords, so you never end up in this position again.

Whether you’re a landlord with one flat in Reading or a portfolio in Oxford, the goal is the same: total compliance with minimum financial damage.

Further Reading on Let Property campaign

To better understand your specific situation, explore our dedicated regional guides:

How many years does the Let Property Campaign go back?

HMRC can go back up to 20 years if they believe the failure to pay was deliberate. If it was a “careless” mistake, they usually look back 6 years. If you took “reasonable care” but still got it wrong, the limit is typically 4 years. An expert helps determine which limit applies to you.

What are the penalties for the Let Property Campaign?

Penalties range from 0% to 100% of the tax owed. For voluntary disclosures where the landlord was “careless” but helpful, penalties are often between 0% and 15%. If HMRC finds you first, those rates jump significantly.

Can I include mortgage interest in my Let Property campaign disclosure?

Yes, but only according to the current rules. Since April 2020, you cannot deduct mortgage interest from your rental income to calculate profit. Instead, you receive a 20% tax credit. Failing to apply this correctly in a disclosure is a common reason HMRC rejects DIY submissions.

Do I have to pay the Let Property campaign full amount immediately?

Not necessarily. While HMRC prefers immediate payment, a Let Property Campaign expert can often negotiate a payment plan (Time to Pay arrangement) if you can demonstrate that a lump sum payment would cause “undue hardship.”

Does the Let Property campaign apply to holiday lets or Airbnb?

Yes. The Let Property Campaign covers all residential property, including specialized lets like Airbnb, student housing, and holiday rentals in areas like Oxford or Windsor. It does not cover commercial property (shops or offices).

What expenses can I claim to reduce my tax bill?

You can claim letting agent fees, property insurance, maintenance and repairs (not improvements), utility bills you paid, council tax during void periods, and professional fees like accountancy or legal costs related to the tenancies.

If you’ve been renting out property in the UK without declaring all of your rental income to HMRC, you are not alone — and you may still have the opportunity to put things right before the taxman comes to you. The HMRC Let Property Campaign is a government-backed voluntary disclosure scheme specifically designed for residential landlords with undeclared rental income. Understanding it — and acting on it quickly — could save you thousands of pounds in penalties and protect you from serious legal consequences.

In this guide, we explain exactly what the Let Property Campaign is, how it works, what penalties you could face, and how working with an experienced Let Property Campaign accountant can make the whole process as straightforward as possible.

What is the Let Property Campaign? (Featured Snippet)

The Let Property Campaign is an HMRC voluntary disclosure scheme for UK landlords who have undeclared rental income. It allows landlords to come forward, declare outstanding tax liabilities, pay what they owe (including interest), and typically receive lower penalties than if HMRC investigates first. The campaign has been open since 2013 and remains active.

What Is the HMRC Let Property Campaign?

The Let Property Campaign (LPC) was launched by HMRC in September 2013 as a targeted initiative to bring UK residential landlords who owe tax on rental income back into compliance. Unlike a full HMRC investigation — which can be costly, stressful, and result in heavy penalties — the LPC offers a structured, more forgiving route for landlords to disclose unpaid tax themselves.

It applies to landlords who rent out one or more residential properties in the UK and have not correctly declared their income to HMRC. This includes landlords who have filed no tax return at all, those who have understated their income, and those who have claimed ineligible expenses. You can find HMRC’s official guidance on the scheme at gov.uk.

The campaign is not a tax amnesty — you will still pay the tax you owe, plus interest. But landlords who come forward voluntarily under the LPC benefit from reduced penalty rates compared to those who wait for HMRC to come to them.

Who Does the Let Property Campaign Apply To?

The campaign is open to any UK individual landlord letting out residential property. This includes:

Landlords who have never registered for self-assessment

Landlords who filed returns but omitted or understated rental income

Landlords who inherited property and have since rented it out

Landlords with overseas rental income not declared in the UK

Landlords who rent out a room in their main residence beyond the Rent-a-Room allowance

The LPC does not cover commercial property, partnerships, or companies — for those cases, HMRC has separate disclosure routes.

How Far Back Does the Let Property Campaign Go?

One of the most common questions we receive at Felix Accountants is: “How far back does the Let Property Campaign go?” The answer depends on the nature of the non-disclosure.

HMRC applies a tiered look-back period based on the perceived intent of the landlord:

Innocent error (careless): 4 years back from the current tax year

Careless or negligent behaviour: 6 years back

Deliberate non-disclosure: 20 years back

For most landlords who simply didn’t realise they needed to declare rental income, the look-back period is typically 4 to 6 years. However, if HMRC decides the failure was deliberate, they can go back up to 20 years, which can result in a very significant tax bill.

Important:

Coming forward under the Let Property Campaign proactively — before HMRC contacts you — is classified as ‘unprompted’. This gives you the most favourable penalty treatment and signals to HMRC that you are acting in good faith.

Let Property Campaign Penalties: What Will You Actually Pay?

Many landlords delay disclosing undeclared rental income because they worry about the financial hit. But the penalty structure under the Let Property Campaign is designed to reward early, voluntary disclosure — meaning the sooner you act, the less you pay.

Penalty Rates at a Glance

Here is how the penalty rates break down depending on your disclosure type:

Disclosure Type

Penalty Range

Typical Scenario

Unprompted

0% – 30%

Landlord comes forward voluntarily

Prompted

15% – 30%

HMRC contacts landlord first

Prompted (deliberate)

30% – 70%

Deliberate non-disclosure

Offshore/concealment

Up to 200%

Offshore assets or deliberate concealment

In addition to penalties, HMRC charges interest on unpaid tax from the date the tax was due. This is currently calculated at the Bank of England base rate plus 2.5%, which means the longer you leave it, the more the interest builds up. A qualified Let Property Campaign accountant can use HMRC’s online tools to calculate the exact interest and penalty figures before you make a formal disclosure.

Prompted vs Unprompted Disclosure

These two terms matter enormously when it comes to your penalties. An unprompted disclosure means you contact HMRC before they contact you. A prompted disclosure means you only come forward after receiving a nudge letter, a compliance check, or direct contact from HMRC.

The difference can be dramatic: unprompted disclosures for non-deliberate errors attract penalties starting at 0%, while prompted disclosures for the same error can attract 15% or more. If you have received an HMRC nudge letter, do not delay — act immediately.

Step-by-Step: How to Make a Let Property Campaign Disclosure

The process has four main stages. Getting each one right is critical to minimising your tax bill and avoiding further investigation.

Step 1 – Notify HMRC

Before you can make a formal disclosure, you must notify HMRC of your intention to disclose. You do this online at gov.uk. HMRC will then issue you with a unique disclosure reference number.

Step 2 – Gather All Relevant Records

This is where most landlords need professional help. You will need records of all rental income received, any eligible expenses you wish to claim, bank statements and tenancy agreements, and records of any mortgage interest (though the rules here changed significantly from 2017 onwards).

Step 3 – Calculate the Tax, Interest, and Penalties Owed

Using HMRC’s disclosure calculator — or more accurately, working with an experienced Let Property Campaign specialist — you will calculate the precise amount owed for each tax year in the look-back period. This includes income tax on net rental profit, National Insurance if applicable, interest on the unpaid tax, and any penalties applied at the appropriate rate.

Step 4 – Submit the Disclosure and Pay

Once the figures are agreed and your disclosure reference number is in hand, you submit the full disclosure to HMRC online and make payment. HMRC gives you 90 days from your initial notification to complete the process.

Pro tip from Felix Accountants:

Do not attempt a Let Property Campaign disclosure without professional guidance. Errors in your disclosure — overstating income, missing eligible deductions, or misclassifying expenses — can result in a higher tax bill than necessary, or flag your case for further investigation.

Why You Need a Let Property Campaign Accountant

The LPC process appears straightforward on paper. In practice, calculating the correct figures, understanding which expenses are allowable, navigating post-2017 mortgage interest relief restrictions, and presenting your disclosure in the most favourable light requires genuine expertise. The wrong approach can cost you significantly more than the accountant’s fees.

At Felix Accountants, our Let Property Campaign specialists have helped landlords across London, Windsor, Slough, Reading, and Oxford navigate the process smoothly and cost-effectively. We advise on:

Which tax years need to be included in your disclosure

How to calculate your allowable expenses correctly, including repairs, letting agent fees, and insurance

How mortgage interest restrictions apply to your specific situation

Whether any wear and tear allowances or capital allowances apply

How to present your disclosure to minimise your penalty exposure

How to respond if HMRC asks further questions after your disclosure

Whether you are based in London or use our specialist services in Windsor, Oxford, Reading, or Slough, our team provides clear, fixed-fee guidance so you know exactly what you will pay before we begin.

Let Property Campaign: Reasonable Excuse — Can You Avoid Penalties Entirely?

HMRC does recognise the concept of a “reasonable excuse” — a genuine reason why you failed to declare your rental income. If accepted, it can reduce or even eliminate your penalties entirely. However, HMRC applies the standard strictly.

What HMRC may accept as a reasonable excuse:

Bereavement of a close family member around the time returns were due

Serious or life-threatening illness preventing you from managing your affairs

A fire, flood, or theft that destroyed your financial records

Genuine uncertainty about whether income was taxable (in limited circumstances)

What HMRC will typically not accept:

Not knowing you had to register for self-assessment

Relying on someone else who failed to act on your behalf

Forgetting to file or pay

Lack of funds to pay

If you believe you have a reasonable excuse, document it thoroughly. Our team at Felix Accountants can advise on whether your circumstances are likely to be accepted and how to present your case effectively.

Is the Let Property Campaign Still Running in 2026?

Yes. As of 2026, the HMRC Let Property Campaign is still open and active. There is currently no announced end date for the scheme. However, HMRC has significantly increased its data-matching capabilities in recent years — using information from letting agents, Land Registry records, deposit protection schemes, and overseas disclosures — which means it is becoming increasingly likely that undeclared landlords will be identified proactively.

The window of opportunity to benefit from the most favourable penalty treatment is narrowing. If you are a landlord with any undeclared rental income, now is the time to act — not when an HMRC letter arrives on your doormat.

Pros and Cons of Using the Let Property Campaign

Advantages of Making a Voluntary Disclosure

Lower penalties — potentially 0% for unprompted non-deliberate disclosures

Avoidance of a full HMRC investigation, which can be far more intrusive and costly

Peace of mind and removal of a significant source of financial and legal stress

Ability to correct the record and move forward with a clean compliance history

More control over the process compared to being investigated by HMRC

Potential Drawbacks to Be Aware Of

You will pay all the tax owed plus interest — there is no reduction in the underlying liability

If HMRC finds errors in your disclosure, it can prompt further scrutiny

The 90-day window to complete disclosure after notifying HMRC can feel tight

Without professional help, it is easy to overclaim or underclaim expenses

Property Campaign Windsor

A Real-World Example: What a Let Property Campaign Disclosure Looks Like

Case Study (anonymised):

A landlord in Windsor came to Felix Accountants after letting out two buy-to-let properties for six years without filing self-assessment returns. Combined rental income over the period was approximately £78,000. After allowable expenses, the taxable profit was significantly lower. We prepared a full 6-year look-back disclosure, correctly applied mortgage interest restrictions, and filed an unprompted disclosure with HMRC. The final settlement included back taxes and interest — but zero penalties, saving the client over £4,500 compared to a prompted disclosure at standard penalty rates.

Related Articles You May Find Useful

If you found this guide helpful, you may also want to read our detailed resources on the Let Property Campaign on the Felix Accountants website:

Frequently Asked Questions About the Let Property Campaign

1. How far back can HMRC go under the Let Property Campaign?

HMRC can typically look back 4 years for innocent errors, 6 years for careless non-disclosure, and up to 20 years for deliberate evasion. Most landlords fall into the 4–6 year category, but your specific situation should be assessed by a qualified accountant before you notify HMRC.

2. What are the penalties for not declaring rental income?

Penalties range from 0% for unprompted voluntary disclosures of innocent errors up to 200% for deliberate offshore concealment. In addition to penalties, HMRC charges interest on all unpaid tax from the date it was originally due. Acting voluntarily before HMRC contacts you will always produce the lowest penalty outcome.

3. Can I use the Let Property Campaign if HMRC has already contacted me?

Yes, but your disclosure will be classified as ‘prompted’, which means higher minimum penalty rates apply. Even so, making a full and accurate disclosure remains far better than ignoring HMRC’s contact. If you have received a nudge letter or compliance check notice, contact a Let Property Campaign specialist immediately.

4. How much does it cost to use a Let Property Campaign accountant?

Fees vary depending on the number of years involved, the complexity of your property portfolio, and the work required to reconstruct records. At Felix Accountants, we offer transparent, fixed-fee packages for Let Property Campaign disclosures. A free initial consultation will give you a clear quote before any work begins.

5. What happens after I submit my Let Property Campaign disclosure?

HMRC will review your disclosure and, in most cases, accept it and issue a statement of account for payment. In some cases, they may ask clarifying questions. If your disclosure is accurate and complete, the process typically concludes smoothly. You should retain all supporting records for at least 5 years in case HMRC follows up.

6. Is the Let Property Campaign the same as a tax amnesty?

No. The Let Property Campaign is not an amnesty — you will still pay all the tax you owe plus statutory interest. The benefit is in the reduced penalties compared to what HMRC would impose following a formal investigation. It is best understood as a structured, lenient route back into compliance rather than a debt write-off.

7. Can overseas rental income be disclosed under the Let Property Campaign?

Yes, but it is more complex. Overseas rental income may also be subject to double taxation agreement provisions, foreign tax credits, and additional HMRC reporting requirements. Felix Accountants has specific experience with overseas property disclosures under the LPC — contact us if you have international rental income to declare.

Get Expert Help With Your Let Property Campaign Disclosure Today

Whether you are a landlord in London, Windsor, Slough, Reading, or Oxford — or anywhere else in the UK — Felix Accountants offers specialist Let Property Campaign advice and full disclosure management. Our team combines deep HMRC compliance knowledge with a practical, client-first approach.

Visit us at felixaccountants.com or call our team directly. We make the Let Property Campaign process simple, transparent, and as cost-effective as possible for every landlord we work with.

Felix Accountants are specialist Let Property Campaign accountants serving landlords across London, Windsor, Slough, Reading and Oxford. This article is for general guidance only and does not constitute formal tax or legal advice. Always consult a qualified professional before making a disclosure to HMRC.

Published by Felix Accountants | Let Property Campaign Specialists across London, Windsor, Slough, Reading & Oxford

Once you notify HMRC of your intent to join the Let Property Campaign (LPC), the countdown begins. You are issued a unique Disclosure Reference Number (DRN) and a Payment Reference Number (PRN), and you have exactly 90 days to calculate your figures, submit your disclosure, and pay the balance.

At Felix Accountants, we call this the “Execution Phase.” The 90-day window sounds generous, but when you are dealing with years of missing bank statements and complex tax rules, time disappears quickly. Here is your roadmap to a successful submission.

1. The Timeline: Notification to Settlement

The LPC is a structured process. Missing the 90-day deadline can result in HMRC rejecting your disclosure and opening a formal (and much more expensive) enquiry.

Day 1: Formal Notification via the Digital Disclosure Service (DDS).

Day 2–60: The “Deep Dive.” This is when we reconstruct your rental accounts.

Day 60–80: We calculate the “Tax Gap,” statutory interest, and the behavior-based penalty.

Day 80–90: Formal submission of the disclosure and payment of the total amount.

2. Essential Documentation Checklist

To make an accurate disclosure, we need to move beyond “estimates” wherever possible. You should begin gathering:

Income Records: Tenancy agreements, letting agent annual statements, or bank statements showing rent deposits.

Expense Evidence: Invoices for repairs, insurance certificates, management fee statements, and utility bills for void periods.

Mortgage Data: Annual mortgage interest certificates (usually provided by your lender every January).

Other Income Info: Your P60 or P11D (if employed) or self-employed accounts. Your rental tax is determined by your total income, so we need the full picture to apply the correct tax bands.

3. Dealing with Missing Records

What if you don’t have bank statements from six years ago?

Bank Requests: Most banks can provide historic statements for a small fee, though this can take 2–3 weeks (hence the urgency).

Reasonable Estimates: If records are truly lost, HMRC allows for “Best Estimates.” We can use local rental market data and average maintenance costs for your property type to build a defensible set of figures.

The Narrative: We must include a note in your disclosure explaining why records are missing and how we reached our estimates.

4. Calculating the “Add-Ons”: Interest and Penalties

Your disclosure isn’t just about the tax. HMRC expects you to “Self-Assess” two other figures:

Statutory Interest

This is not a penalty; it is compensation to the government for not having the money on time. Interest rates for late tax have risen significantly in 2025 and 2026. We use specialized software to calculate interest from the date the tax should have been paid to the current date.

The Penalty Offer

You must make a “Formal Offer” of a penalty. As discussed in previous articles, this is based on your behavior:

Reasonable Care: 0%

Careless (Unprompted): 0% – 30%

Deliberate (Unprompted): 20% – 70%

5. Making the “Formal Offer”

A unique feature of the LPC is that it is a Contractual Disclosure. When we submit the form, we are making a “Formal Offer” to pay a specific amount. If HMRC accepts this offer, it becomes a legally binding contract that prevents them from re-opening those specific years in the future (provided your disclosure was honest).

6. What If You Can’t Pay Everything on Day 90?

If the final bill is larger than expected, do not wait until Day 90 to tell HMRC. * We can negotiate a “Time to Pay” (TTP) arrangement.

HMRC is generally more open to payment plans (spreading the cost over 6–12 months) if the request is made as part of a voluntary disclosure.

Frequently Asked Questions (FAQs)

Can I submit the disclosure before the LPC 90 days are up?

Yes. You can submit as soon as your figures are ready. In fact, submitting early reduces the amount of statutory interest you have to pay.

What happens if I miss the LPC 90-day deadline?

HMRC may remove you from the campaign. This means you lose the “favourable terms” and lower penalties. They may then open a formal enquiry into your affairs.

HMRC “reviews” every submission. If your figures look sensible and match their “Connect” data, they usually issue an acceptance letter within 30–60 days. If the figures look suspiciously low, they will ask for evidence.

Do I need to send my LPC receipts to HMRC with the disclosure?

No. You don’t send the receipts with the form, but you must keep them for 6 years after the disclosure. HMRC can ask to see your “working papers” at any time during that period.

Can Felix Accountants handle the LPC payment for me?

You usually pay HMRC directly using your PRN (Payment Reference Number). However, we ensure you have the exact bank details and references to ensure your payment is allocated correctly to your disclosure.

Beat the LPC Clock with Felix Accountants

The LPC 90-day window is the final hurdle to tax peace of mind. Let Felix Accountants take the lead on the calculations and the paperwork, so you can focus on the future of your property investment.

[Button: Start My 90-Day Disclosure Process][Button: Get a Quote for LPC Management]

If you have recently opened your mail to find a letter from HM Revenue & Customs (HMRC) regarding your property income, you are likely feeling a mix of confusion and anxiety. You aren’t alone. In 2026, HMRC has significantly ramped up its “one-to-many” mailing campaign, often referred to targeting residential landlords across the UK.

At Felix Accountants, we specialize in helping landlords navigate these letters through Let Property Campaign (LPC). This guide will walk you through exactly what these letters mean, the risks of ignoring them, and how you can resolve your tax position while minimizing penalties.

1. What Exactly is an HMRC Nudge Letter?

A nudge letter is not a formal tax enquiry or a notification of a criminal investigation. Instead, it is a “soft” prompt from HMRC’s data-driven system.

HMRC uses a sophisticated AI software called Connect. This system cross-references data from the Land Registry, letting agents, mortgage applications, and even sites like Airbnb or Booking.com. If the system identifies a person who owns multiple properties or has a buy-to-let mortgage but no corresponding rental income on their tax return, a nudge letter is triggered.

The letter essentially says: “We have information that suggests you may have rental income. Please check your records and let us know if you need to pay tax.”

2. Why Have I Received This Letter Now?

HMRC’s “Connect” system is more powerful than ever. Common triggers for receiving a nudge letter in 2026 include:

Land Registry Updates: You purchased a second property or changed the title deeds.

Tenancy Deposit Schemes: Your tenant’s deposit was registered, creating a digital paper trail.

Stamp Duty Records: Historical data from when you purchased the property.

Third-Party Reporting: Letting agents are now legally required to provide HMRC with lists of landlords they represent.

3. The “Certificate of Tax Position”: The Hidden Trap

Most nudge letters include a document called a Certificate of Tax Position. HMRC asks you to sign and return this within 30 days.

Warning: This certificate is not a statutory requirement. You are not legally obligated to sign it.

Why you should be cautious:

The certificate asks you to declare one of the following:

My tax affairs are up to date.

I have some additional tax to disclose.

I have not been a landlord during the period.

If you sign the certificate stating your affairs are up to date, and HMRC later finds an error, you could face criminal prosecution for “Dishonest Disclosure” or “Perjury.” It is almost always better to have an accountant respond with a formal letter on your behalf rather than signing this specific HMRC document.

4. The Let Property Campaign (LPC): Your “Amnesty”

If you realize you do owe tax, the best route for resolution is the Let Property Campaign. This is a specific disclosure facility for individual landlords renting out UK residential property.

The Benefits of the LPC:

Lower Penalties: By coming forward via the LPC (an “unprompted disclosure”), your penalties can be as low as 0% to 20%. If you wait for HMRC to start a formal investigation (a “prompted disclosure”), penalties can soar to 100% or even 200% for offshore income.

Fixed Timeline: Once you notify HMRC, you have a clear 90-day window to calculate and pay.

Manageability: It allows you to wrap up multiple years of tax into one single settlement rather than filing dozens of individual backdated tax returns.

5. Step-by-Step: How to Respond to Your Nudge Letter

Step 1: Review Your Records

Don’t rely on memory. Gather your bank statements, letting agent statements, and mortgage interest certificates for the last several years. You need to calculate your actual profit, not just your total rent.

Step 2: Seek Professional Advice

Before replying to HMRC, speak to a specialist like Felix Accountants. We can perform a “Pre-Disclosure Check” to see exactly how much you owe and whether you have a “Reasonable Excuse” for the delay (which can further reduce penalties).

Step 3: Notify HMRC of Intent

We will register you for the Let Property Campaign. This “stops the clock” on further HMRC action and gives us 90 days to prepare the figures.

Calculating the Section 24 Tax Credit for mortgage interest.

Adding statutory interest and the correct penalty percentage.

Step 5: Submission and Payment

Once the disclosure is submitted and the tax is paid, HMRC usually issues an acceptance letter within a few weeks, bringing the matter to a permanent close.

6. What If I Don’t Owe Any Tax?

Sometimes, HMRC gets it wrong. You might have received a letter even if:

Your rental income is below the £1,000 Property Allowance.

You are letting a room in your own home under the Rent-a-Room Scheme (below £7,500).

The property is owned by a Limited Company, and you’ve already paid Corporation Tax.

Even if you owe nothing, do not ignore the letter. You must still respond to explain why no tax is due. Ignoring the “nudge” will almost certainly lead to a formal, much more intrusive tax enquiry.

7. How Far Back Will HMRC Look?

One of the most common questions we hear is: “How many years do I need to pay for?” The answer depends on your “behaviour”:

Behaviour

Look-back Period

Reasonable Care (You tried to get it right but failed)

4 Years

Careless (You didn’t pay enough attention to your tax)

6 Years

Deliberate (You knew you should pay but chose not to)

20 Years

At Felix Accountants, our job is to argue for the lowest possible category based on your specific circumstances.

8. Summary: The Cost of Delay

The difference between acting now and waiting for a formal investigation can be tens of thousands of pounds.

Scenario A (Proactive): You use the LPC. You pay the tax + interest + 10% penalty.

Scenario B (Reactive): HMRC opens an enquiry. You pay the tax + interest + 70% penalty + potential “Naming and Shaming” on the HMRC website. Frequently Asked Questions (FAQs)

Q1: Can I just start filing my next tax return correctly and forget about the past?

No. HMRC’s systems look backward. Filing a correct return now might actually “flag” the fact that you owned the property in previous years, triggering an enquiry into your history.

Q2: What if I don’t have receipts from 5 years ago?

We can use “Reasonable Estimates.” HMRC allows for the reconstruction of records using bank statements and average costs for the period, provided the figures are sensible and defensible.

Q3: I live abroad; does the Let Property Campaign apply to me?

Yes. If you own property in the UK, you are liable for UK tax regardless of where you live. There is also a “Non-Resident Landlord Scheme” you should be aware of.

Q4: Will I go to prison for undeclared rent?

Criminal prosecution is extremely rare for landlords who come forward voluntarily via the Let Property Campaign. HMRC’s primary goal is to collect the tax, not to fill prison cells. However, ignoring letters increases your risk significantly.

Q5: How much does it cost to have Felix Accountants handle this?

We offer a transparent, fixed-fee service for LPC disclosures. Most clients find that the tax and penalties we save them far outweigh our fees.

Take Control of Your Tax Position Today

If you’ve received a nudge letter, the clock is already ticking. Don’t let a simple mistake turn into a legal nightmare.

Contact Felix Accountants for a confidential consultation. We will review your letter, assess your records, and handle HMRC so you don’t have to.

With UK housing valued at over £10 trillion, and most of that being pure equity (unmortgaged), the conversation around property tax hikes is heating up. As the government hunts for new revenue sources, property wealth stands out as low-hanging fruit. But would increasing property tax actually work? And how might it affect property investors, landlords, and homeowners?

How Property Taxes Work in the UK

What is Property Tax in the UK?

In the UK, property tax comes in several forms:

Stamp Duty Land Tax (SDLT): Paid when buying property

Council Tax: Annual tax paid by occupants

Capital Gains Tax (CGT): Paid on profit from property sales (not main residences)

Rental Income Tax: Income tax on profits from letting property

Together, these taxes raised over £10 billion in 2023/24 alone. SDLT especially targets higher-value and second-home purchases, making it feel more like a wealth tax than a transactional levy.

Inflation pushing up property values and taxable thresholds

Increased reliance on wealth-based taxation to fund public services

How Much Do Property Owners Pay?

How Much Tax Do You Pay for Owning a House in the UK?

There is no annual tax for owning a property in England, but you’ll pay:

Council Tax: £1,200–£3,000+ depending on location

Stamp Duty when purchasing

CGT if selling an investment property

How Much Property Income is Tax-Free in the UK?

You can earn up to £1,000 tax-free per year through the property income allowance, or claim allowable expenses. Higher earners pay up to 45% tax on net rental profits.

Rules You Need to Know

What is the 36-Month Rule?

If you’ve moved out of your main residence, the last 36 months of ownership still qualify for CGT relief. This protects sellers during transitions.

What is the 2-Out-of-5 Rule?

You must have lived in a property for 2 out of the last 5 years to qualify for private residence relief when selling, protecting you from most CGT charges.

What is the August Rule?

Though not a formal tax term, “August Rule” often refers to CGT timing strategies—like selling just before a new tax year. It’s commonly used in tax planning to manage thresholds or changes.

Selling, Moving & Overseas Property

Do You Pay Tax When You Sell Your House in the UK?

Not if it’s your main residence. The main residence relief makes owner-occupier home sales exempt from CGT. But investment properties and second homes do incur CGT.

Can I Sell My House and Still Live in It in the UK?

Only under sale-and-leaseback arrangements or if you transfer ownership (e.g., to family). Be aware this can affect tax liability and eligibility for CGT relief.

Do I Have to Pay Tax in the UK if I Sell My House Abroad?

Yes — UK residents must declare overseas property sales. You may owe UK CGT, but can often claim foreign tax credits to avoid double taxation.

Global Context: Property Tax Abroad

What Countries Have No Property Tax?

Countries with no annual property tax include:

Monaco

UAE

Malta

But many still charge high acquisition fees or stamp duty.

What States Have No Property Tax or Income Tax?

In the U.S.:

States with no income tax: Florida, Texas, Nevada

No state has zero property tax, but rates vary—Hawaii and Alabama have some of the lowest.

Investor FAQs & Wealth Management

What is the Most Tax Efficient Way to Buy Property in the UK?

Using a limited company structure (for buy-to-let)

Maximizing spouse exemptions and CGT allowances

Investing in areas with lower SDLT bands

Using pension funds (SIPP/SSAS) for commercial property

Is Buying Property in the UK a Good Investment?

Despite tax changes, UK property remains strong due to:

Long-term capital growth

High rental demand

Stable legal framework

But the net yield is narrowing, especially in areas hit hardest by stamp duty and reduced mortgage relief.

System Criticism & Proposed Reforms

Why Are My Property Taxes So High Compared to My Neighbors?

Possible reasons include:

Different council tax bands

Area-specific levies

Property size and valuation discrepancies

Who Raises Property Taxes?

National government: Stamp Duty, CGT

Local councils: Council Tax and specific regional levies

Does Inflation Cause Property Taxes to Go Up?

Yes. Inflation increases property valuations, leading to:

Higher SDLT upon purchase

Increased council tax banding

Greater capital gains upon sale

Future Tax Changes: What Could Happen?

Will Reliefs Be Scrapped?

The most at-risk relief is CGT allowance, which has already dropped from £12,000 to £3,000. A lifetime CGT cap on the main residence is also being discussed—though politically risky.

Is a Wealth Tax on Homes Coming?

Not officially. But stamp duty and CGT are already functioning as de facto wealth taxes, especially for:

Second homes

Foreign buyers

Properties over £1M

What Should Investors Do Now?

Model your CGT exposure across multiple properties

Consider corporate ownership for high-yield portfolios

Watch for any Autumn Budget updates on SDLT or CGT

Plan sales to maximize existing reliefs while they last